Mar 16, 2025

Can 100-Year-Old Jewellery Mine New-Age Diamonds?

Retail

Last month, jewellery startups continued to pick up pace as lab grown diamonds became even more attractive, and 200 Cr of funding went into the category.

Golden Bird

In India, the art of adornment is as old as civilisation.

The country’s romance with jewelry stretches back over 5,000 years, weaving a tapestry of opulence, cultural significance and evolving economic landscapes.

From the alluvial rivers of ancient India to modern-day labs, the story, much like the diamonds, seems to last forever.

India remained the only supplier of precious gems to the world for centuries. Ancient Sanskrit texts, like the Arthashastra (circa 3rd century BC) describe diamonds as symbols of divine energy, used for religious ceremonies in addition to adornment. For example, yellow diamonds were believed to bring prosperity, while clear diamonds were thought to enhance wisdom and purity.

India’s diamond deposits were primarily found in the Krishna, Godavari and Penner riverbeds in present-day Andhra Pradesh and Telangana. The Golconda region became famous for producing the Koh-i-Noor, or the Hope diamond.

Indian miners used basic tools to extract gemstones from these regions and supplied them to traders who transported them across the Silk Road to markets in the Middle East and Europe. It was only in the medieval period (5th to 15th centuries) that Indian artisans perfected diamond cutting and polishing techniques, making them more desirable among the ruling elite.

The period from 16th to 18th century marked a golden age for Indian jewelry under the patronage of Mughal emperors. They commissioned elaborate pieces incorporating diamonds, rubies, and emeralds, leading to the evolution of intricate jewelry-making techniques that live on to this day.

One such technique, originating in the royal courts of Rajasthan and Gujarat, was Kundan - setting gemstones with gold foil between the stones and their mount. Another art form introduced to India by Persian craftsmen was Meenakari, which is the process of enameling metal surfaces with vibrant colours to form detailed designs.

The Mughal period also popularised Polki, using uncut, rustic diamonds in jewelry. They were often combined with Kundan and Meenakari work, resulting in some of the most unique pieces of the time.

By the 17th century, Indian diamonds were highly sought after in European courts, adorning French monarchs like Louis X1V, who owned the famed Tavernier Blue diamond.

India’s historical moniker ‘Sone ki chidiya’ symbolises the historical affluence, prosperity and cultural richness during this time. Its abundant natural resources in gold, diamonds and gemstones were sought after in global markets.

Unfortunately, with the turn of the century and the beginning of British colonial rule, India’s diamond trade began to wane. The East India Company imposed heavy taxes and regulations on local artisans, limiting their ability to export to the west.

Despite the economic setbacks, the demand for Indian diamond jewelry remained strong among the aristocracy. The Indian elite continued to commission elaborate jewelry, keeping the traditional craftsmen alive.

At the same time, massive new diamond deposits in Brazil and South Africa were being discovered, overshadowing India’s depleting alluvial mines. India transitioned from being a primary diamond producer to a hub for cutting and polishing diamonds sourced from other parts.

Towards the end of the colonial era, the legacy of India’s ancient diamond trade and centuries of artistry, positioned it well for resurgence as a powerhouse in the global gem and jewelry markets.

Infusing Purity & Trust

In the years post-independence, the diamond and jewelry industry underwent a slow but consequential change.

It faced multiple challenges in a new economic and regulatory environment and changing consumer preferences, but the stresses allowed it to shine even brighter.

Traditional jewelry purchases were based on trust, with little formal verification of the diamond quality or gold content. This lack of standardisation led to the risk of adulteration, with jewelers misrepresenting diamond clarity and weight and sometimes mixing gold with impurities.

Much of the jewelry industry was run by small, family-owned businesses that remained fragmented and unorganised. Unlike in Western countries, where large brands emerged, Indian consumers mainly relied on independent local jewelers.

This lack of uniformity made comparing products or ensuring fair pricing across geographies difficult. Buyers depended on impeccable family reputations instead of quality control or fair trade practices regulated by a central body.

Policymakers and industry stakeholders began establishing a formal hallmarking and certification system in 1947 with the formation of the Indian Standards Institution (ISI), which would later become the Bureau of Indian Standards (BIS). Consumers gradually became more aware of purity concerns, marking a slow shift toward transparent sourcing and pricing.

While talks about standardising the trade began to emerge, it would be several decades before an organised structure would develop.

Urbanisation and lifestyle changes in the 20th century also led to a shift in consumer preferences for jewelry. While traditional heavy gold and diamond ornaments remained a cultural staple for occasions such as weddings, sleek, lightweight designs became common for work and modern social gatherings.

Women looked to balance elegance with functionality. Delicate necklaces, bangles, and stud earrings started to be preferred over heavy Kundan sets.

Jewelers began to experiment with minimalist designs and new materials. They started incorporating smaller, precision-cut diamonds instead of large Polki diamonds into geometric designs.

They also began using 14 and 18-karat gold to allow for more affordable jewelry than traditional 22-karat gold. Designs that set diamonds in minimal embellishments started gaining acceptance among the younger, affluent population.

By the 1960s, while the industry was still largely unorganised, specific structural changes began taking shape. Established family businesses continued to flourish, but demand for certification grew, laying the foundation for quality standards.

Surat, in Gujarat, was emerging as a leading diamond-cutting and processing hub thanks to its tradition of craftsmanship and availability of low-cost skilled labour. Moreover, the city’s proximity to Mumbai allowed easy import of rough diamonds and export of finished ones.

The city’s family-run businesses invested heavily in the diamond trade by setting up advanced laser-cutting technology and networks abroad to funnel business back to India.

Surat’s artisans were setting the stage for the country’s rise as a leader in diamond processing in the coming decades.

Unshackling Jewelry

As newly independent India approached the second half of the 20th century, prominent family jewelers operated in Mumbai, Delhi, Chennai, and Kolkata.

Around the 1960s and 1970s, businesses such as Tribhovandas Bhimji Zaveri, P.C. Chandra and GRT Jewellers built reputations for quality and trust based on decades of relationship and experience.

While the industry remained primarily unorganised and unregulated, these jewelers gradually set informal industry benchmarks for purity, pricing and customer service. They set up multiple outlets in major urban centers, expanding beyond single stores.

One of the challenges businesses faced was the heavy regulation of gold and diamond imports. The government restricted individual gold holdings to control the outflow of foreign exchange reserves. It limited the trade of gold bars and coins through policies like the Gold Control Act of 1968.

This, however, did not deter the demand for diamond and gold jewelry, and the industry thrived despite restrictions. Indian families continued to invest in jewelry for weddings and ceremonies and to preserve wealth. The restrictions led consumers to seek gold through unofficial channels.

A black market for gold emerged with some estimates suggesting that approximately 80 tonnes entered the country in a single year, like 1988, with customs being able to seize only a fraction of that amount. Consequently, this fostered criminal networks and deprived the state of revenue.

Recognising the challenges, the government eventually repealed the Gold Control Act in 1990, as part of broader liberalisation of the economy. This move marked a critical moment for the jewelry industry, paving the way for modernisation and integration into the global economy.

The industry began to see rapid expansion and formalisation, thanks to the reduced dependency on smuggling networks and improved access to raw materials. Branded jewelry retailers emerged.

Tanishq, a subsidiary of the Tata Group, was launched in 1994, revolutionizing the market with a focus on quality assurance, transparency, and improved retail experience. They introduced certified diamonds and lightweight, contemporary designs that appealed to India’s growing working professionals. To further build transparency and address adulteration concerns, Tanishq introduced ‘karat meters’ in its stores, allowing customers to verify gold purity on the spot.

Almost in parallel, the Bureau of Indian Standards (BIS) finally introduced the BIS hallmarking system in the late 1990s, setting uniform standards for gold purity and ensuring that buyers could trust their purchase. Many jewelers adopted these certification practices, improving transparency in the market.

At the turn of the 21st century, India’s jewelry industry looked more structured and reliable.

Improved regulation and a growing middle class, combined with the rise of branded players, laid the proper foundation for sustained growth in jewelry retail and diamond processing.

Formalizing a Golden Run

Family-run jewellers dominated India’s jewellery market for decades, thriving on craftsmanship, trust, and generational loyalty.

Jewellery purchases were deeply tied to weddings, religious traditions, and wealth preservation, making personalised service and flexible home offerings essential to their success.

Customers valued customised designs, familiarity with preferences, and negotiable pricing, reinforcing relationships in an era without mandatory hallmarking or certification.

Regional expertise further shaped consumer choices—South Indian jewellers specialised in temple jewellery, while North Indian jewellers mastered Kundan, Polki, and Meenakari designs. These artisans worked with skilled local craftsmen, ensuring unique, handcrafted jewellery.

Many also offered credit and installment options, making purchases more accessible. Leading names like Tribhovandas Bhimji Zaveri, PN Gadgil, and C. Krishniah Chetty & Sons set industry benchmarks in quality and trust.

Organised retail chains emerged as urbanisation, globalisation, and regulatory changes reshaped consumer preferences. The introduction of BIS hallmarking (2000) and certified diamonds (GIA, IGI) pushed buyers toward standardised pricing, assured quality, and modern showroom experiences. Tanishq led the way, introducing fixed pricing and structured retail experiences, forcing traditional jewellers to modernise.

Retail chains expanded aggressively, moving beyond regional strongholds into Tier-1 and Tier-2 cities, enhancing visibility through mall outlets and flagship showrooms.

Brands like Kalyan Jewellers and Malabar Gold even entered international markets like the Middle East, the USA, and Southeast Asia, positioning Indian jewellery globally.

Marketing played a crucial role in shaping jewellery as a modern lifestyle purchase, with brands leveraging celebrity endorsements, festive campaigns, and influencer-driven promotions. Amitabh Bachchan (Kalyan), Deepika Padukone (Tanishq), and Kareena Kapoor (Malabar) became key faces of this transformation.

Organized retailers also introduced gold savings plans, EMI options, and loyalty programs, attracting middle-class buyers who previously relied on informal credit. In 2008, the global financial crisis drove gold prices up by 40%, reinforcing its role as a wealth preserver.

As India’s economy surged—with GDP growing at 7.2% annually between 2000 and 2010—disposable incomes increased, and more consumers prioritised certified jewellery and structured pricing. The 2008 financial crisis further drove gold demand, pushing prices up by 40%, reinforcing its role as a safe-haven investment.

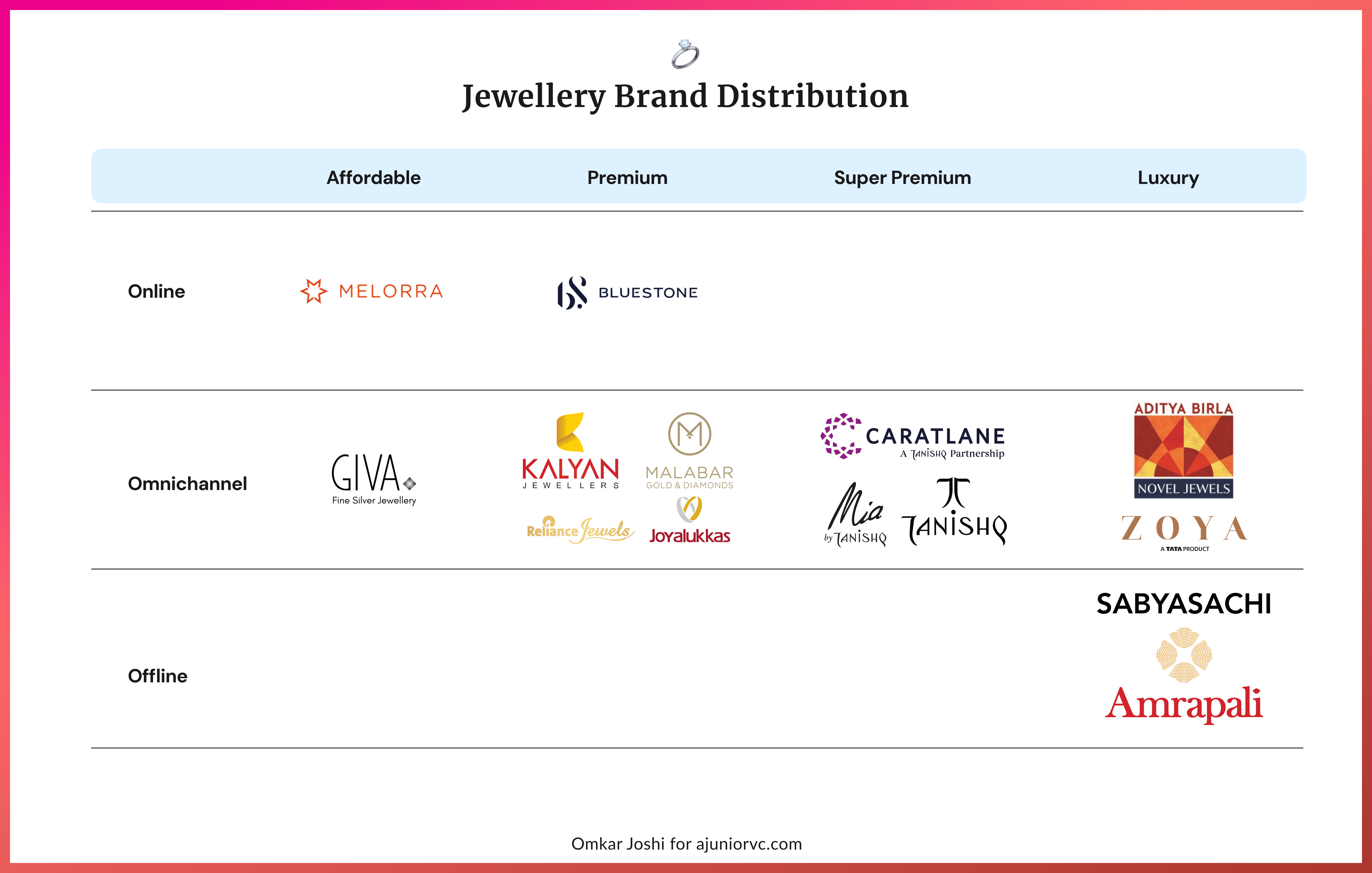

The early 2010s ushered in a new wave of change, with e-commerce and D2C jewellery brands like CaratLane and BlueStone pioneering online shopping. Younger buyers, seeking convenience, affordability, and transparency, gravitated toward virtual try-ons, and try-at-home models.

Organized retailers adapted, with Tanishq, Malabar Gold, and Kalyan Jewellers investing in e-commerce, click-and-collect services, and virtual consultations, blending digital convenience with in-store trust.

Strong Omni Channel

The Indian jewelry industry underwent a significant shift in the 2000s.

Until then, it was fragmented and dominated by family-run businesses. Consumers relied on trust, but there was little standardisation. That changed with the rise of organised retail.

As jewellery purchasing evolved, so did gold investments. Beyond adornment, Indians sought secure, liquid alternatives, leading to the rise of digital and paper-based gold assets. Gold Exchange-Traded Funds (ETFs), introduced in 2007, allowed investors to own gold without physical storage.

To further formalise gold investment, the Indian government launched Sovereign Gold Bonds (SGBs) in 2015, offering annual interest and capital appreciation as an alternative to physical gold. With benefits like tax exemptions and no storage costs, SGBs became a preferred option for urban investors.

While digital gold, ETFs, and SGBs continued to gain traction, gold jewellery remained deeply ingrained in Indian culture, especially for weddings and festivals.

By 2016, digital gold platforms powered by MMTC-PAMP were started on Paytm, PhonePe, Google Pay. They gained momentum, enabling users to buy and sell small fractions of gold online.

The Tata Group’s Tanishq led the transformation into a more organised play. It introduced fixed pricing, hallmark certification, and a modern shopping experience. Consumers who were used to negotiating over gold prices now saw a transparent model.

This shift forced traditional players to adapt. Around the same time, brands like Malabar Gold, Kalyan Jewellers, and Joyalukkas expanded aggressively. They built national brands, moving beyond their regional roots. Jewelry shopping, once an informal affair, was becoming structured.

Economic growth and urbanisation significantly increased disposable incomes and shifted consumer preferences toward branded jewelry. This drove organized players to expand aggressively to meet demand. The next inflection point came in mid 2016 with the rise of e-commerce.

Is 20,000Cr CaratLane India's Biggest Startup Turnaround?

CaratLane and Bluestone were key in expanding online jewelry retail, making certified jewelry more accessible and reshaping consumer trust in the digital-first model.

Jewelry was a high-trust purchase, and buying gold or diamonds without seeing them felt risky. These platforms tackled the problem by offering home trials, easy returns, and certification-backed products.

Titan, which owned Tanishq, saw the potential early and acquired a 62% stake in CaratLane in 2016 for INR 357 Cr. The move integrated online convenience with offline assurance, setting the stage for omnichannel retail.

Then came the pandemic in 2020. Lockdowns forced jewelers to go digital. Virtual try-ons, WhatsApp catalogs, and video consultations became standard.

As uncertainty loomed, gold demand hit record highs, with prices touching INR 55K per 10 grams in August 2020, up 34% year-over-year. Consumers turned to trusted brands, and the shift toward organised retail accelerated.

The post-pandemic world saw omnichannel emerge as the dominant model. Digital discovery led to offline fulfillment, blending the strengths of both formats.

But as India’s appetite for jewelry continued to rise, competition also heated up.

Deeper Markets

As India entered the early 2020s, the jewelry market had become a battleground.

The rising incomes and wealth, along with offline lockdowns, were both fueled by the pandemic. Legacy brands like Tribhovandas Bhimji Zaveri, Joyalukkas, and Senco Gold continued to command deep customer loyalty. They thrived on reputation and community trust.

Organized chains like Tanishq, Malabar Gold, and Kalyan Jewellers built nationwide networks, offering standardised quality and transparent pricing. New entrants like Reliance Jewels, with ~150 standalone showrooms and 200+ shop-in-shop outlets, leveraged scale and aggressive expansion to capture market share.

Digital-first brands like CaratLane, Bluestone, and Melorra pushed affordability and convenience, appealing to younger buyers. Luxury designers like Amrapali, Sabyasachi, and Hazoorilal catered to the high-end segment, focusing on craftsmanship and exclusivity.

The investment-driven gold segment, led by MMTC-PAMP, Augmont, Safegold, Jar and Paytm Gold, tapped into the shift toward digital gold and gold-backed assets, with India’s digital gold market expected to reach 30,000 Crore by 2030.

The competition was fierce, but the right to win depended on multiple factors.

Trust was non-negotiable. Jewelry was a high-value purchase, often linked to significant life events. Consumers prioritised authenticity, making brand credibility a key differentiator.

Pricing strategy mattered. Traditional retailers enjoyed 25-30% gross margins but faced the challenge of scaling efficiently. Digital players operated with lower overheads but struggled with thinner margins, typically 10-15%.

The market structure was also evolving. Wedding jewelry, once the dominant segment, was now competing with daily-wear demand. Younger buyers preferred lightweight, contemporary designs over heavy, traditional pieces.

The share of studded jewelry in overall sales grew from 10% in 2015 to 25% in 2023. Gold as an investment was seeing a shift.

With rising financial literacy, more consumers opted for sovereign gold bonds and digital gold instead of physical jewelry. Sovereign gold bond issuances crossed INR 45K Cr by 2022-23 since their inception in 2015.

Technology is playing a crucial role in shaping the future. Augmented reality is enabling virtual try-ons. AI is helping brands personalise recommendations. 3D printing was reducing design-to-market timelines.

Consumer preferences change rapidly. Brands that can anticipate and adapt will lead to the next growth phase.

As the industry stands today, no single model dominates. Traditional players are modernising. E-commerce brands are adding offline touchpoints.

Large conglomerates were entering the space with distinct positioning, such as Aditya Birla’s Novel Jewels, which plans to invest INR 5,000 crore in the jewelry market, and Tata’s Zoya, a super-premium brand catering to the ultra-luxury segment.

As the Indian market deepened, a sliver became more attractive. Each demographic needed their variant, like young urban consumers or older rural consumers. Each occasion, everyday wear or wedding wear, needed its own.

By 2022, this shift opened up many opportunities, including an entirely new form of jewellery.

Man Made Shift

With the influx of money and change in jewellery buying sentiment, India’s jewellery market transformed.

Lab-grown diamonds (LGDs) quickly became a key part of this change. LGDs, unlike their real counterparts, were manufactured. Due to the ease with which they were produced, costs were much lower than the natural type.

In 2023, the overall jewellery market was valued at about 6 lakh crores and was expected to grow steadily, reaching nearly 10 lakh crores by 2030 with a CAGR of 5.7% between 2024 and 2030. This impressive growth would be driven by higher disposable incomes, rapid urbanisation, the digital revolution, and evolving consumer tastes that favor innovative and ethically sourced products.

India’s long history of precious metals was reflected in the country's contribution of roughly 24% to the global jewellery market in 2023. This statistic highlighted India’s deep cultural connection to luxury and tradition.

At the same time, consumer attitudes were shifting. More and more buyers are now open to alternative options that deliver the same sparkle and beauty at a more attractive price point. The jewellery industry's organised sector capitalised on these shifts, such as lab grown diamonds.

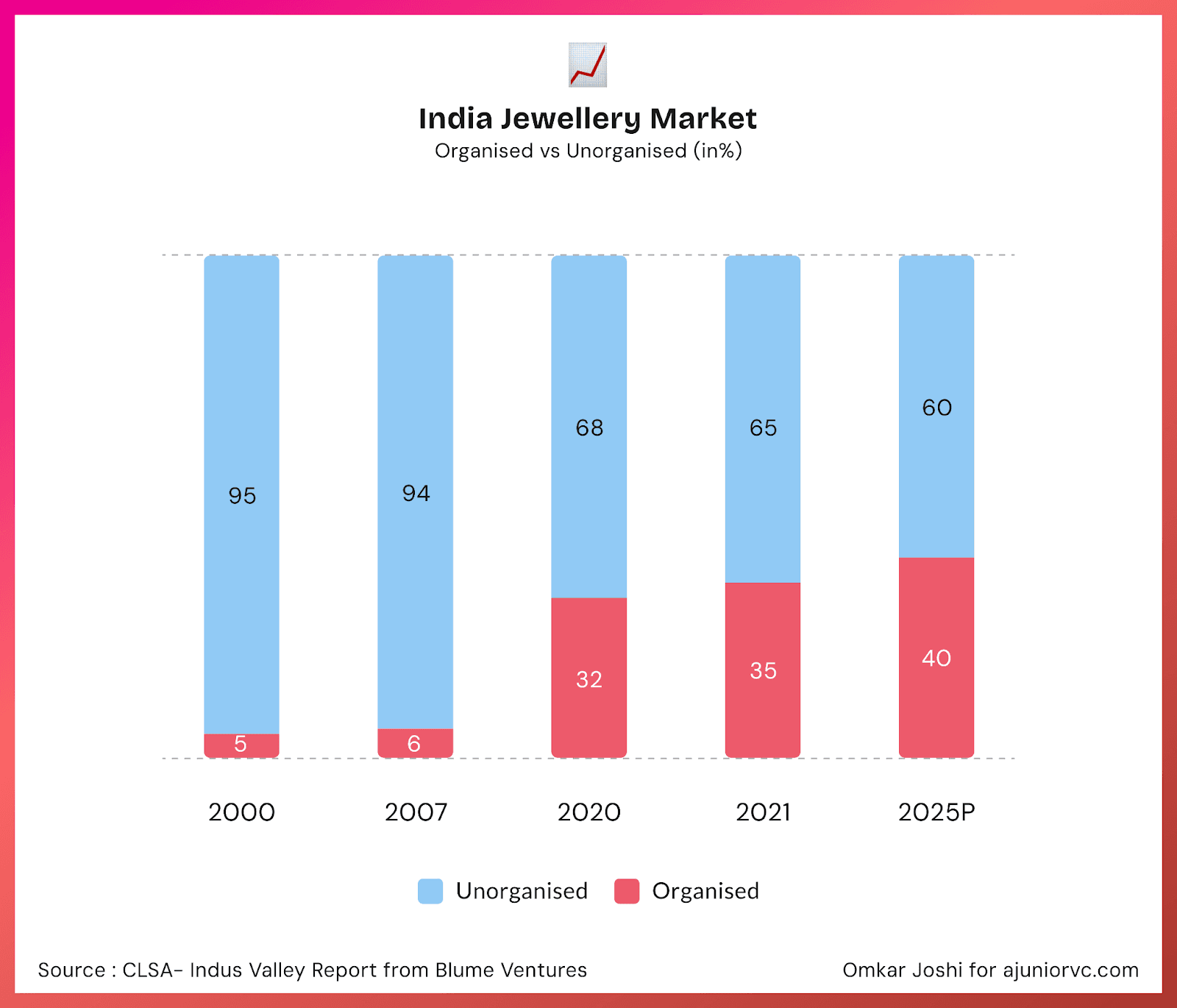

Organized retailers comprised about 35-40% of the market, and this share is expected to grow to 50% by 2030. This trend will likely improve quality, increase transparency, and bring more innovation. The organized retail sector is supported by a increasingly large processing chain.

India, specifically Surat, is a significant hub for diamond processing. India imports rough diamonds for cutting and polishing. However, imports of rough diamonds decreased by 22% recently due to weak demand from key markets like the U.S. and China. Exports have also declined by 8.3%.

The decline in both signals towards one massive opportunity - innovation in the industry, which is a category creation segment instead of expecting more demand in the existing space. Technological advancements have considerably shifted most sectors, including diamonds.

The quality of lab-grown diamonds is nearly indistinguishable from naturally mined ones. This evolution is especially popular among younger consumers who value ethical sourcing, sustainability, and cost-effectiveness. As production methods become more efficient, the price gap between mined and lab-grown diamonds is expected to narrow further, widening their appeal.

Though lab-grown diamonds look like they are going to win, the purpose of buying diamonds is also to indicate an “investment”. If LGDs become too cheap or accessible, their utility as a signal starts to diminish. The race to the bottom in LGDs could also likely kill margins and make the sector less attractive.

New players were thus staring at a large yet fast-evolving market.

Opportunities for New Diamonds

The key driver for India’s jewellery industry has been the gigantic Indian wedding industry.

Gold occupied the lion’s share for spend. For every one percent increase in per capita income, gold demand rises by 0.9%. Gold remains the preferred metal, with the five southern states accounting for ~40% of India’s gold jewelry sales. Its dominance stems from its cultural significance in weddings and its strong perception as a store of value and hedge against inflation.

Gold demand is also linked to agricultural cycles, peaking during Kharif and Rabi harvests. Farmers often use gold as collateral for sowing or working capital needs. Wedding purchases remain high value, with total jewelry spending per wedding ranging from INR 5-15 lakh, representing a significant share of household savings.

However, repeat purchases are low, and margins remain moderate due to intense competition and a focus on purity over design.

Most jewellery was initially made for this occasion, as it used to be expensive and inaccessible. Organisation, technology and the internet are helping the market evolve beyond wedding-driven demand, with shifting consumer preferences, new categories, and investment trends shaping its future.

As gold prices rose, and diamonds became inaccessible, people shifted to more options. The demand for non-wedding jewelry is rising, with daily-wear jewelry expected to match wedding jewelry sales by the decade’s end. Younger, urban consumers are moving away from traditional heavy gold pieces, opting for lightweight, contemporary designs that align with their lifestyles.

A key driver of this shift is the growing accessibility of niche and specific jewelry styles that were once hard to find. Design technology and manufacturing advances have made it easier to create and distribute intricate, customized, and trend-driven pieces.

A new wave of daily-wear jewelry buyers is emerging, preferring lightweight, contemporary pieces over heavy traditional designs. This shift has fueled demand for digitally-driven brands which leverage data analytics, personalisation, and online-first strategies to attract young, urban consumers.

Consumers now have access to various metals, including steel, gold, and silver, expanding their choices beyond conventional high-value gold ornaments.

Rising gold prices have also nudged buyers toward alternative materials and more affordable yet stylish options. Brands like Giva, Jewelbox, Aukera, and Palmonas are capitalising on this shift, offering modern designs that blend aesthetics with affordability.

New age brands like Yinara, Trisu and Pippa Bella also started to scale. Digital-first retailers and established players are expanding their collections to cater to this evolving demand.

With innovation in materials and design, India’s jewelry landscape is no longer limited to traditional, occasion-based purchases.

Instead, it is becoming a diverse market where personal expression and everyday wear are beginning to take center stage.

India’s Bright Sparkle

Beyond domestic consumption, India is capitalizing on global trade shifts.

With China+1 strategies driving supply chain diversification, India is emerging as the preferred global hub for jewelry exports. 80% of the world's diamonds pass through India for cutting and polishing, reinforcing its role as a critical link in the international supply chain.

At the ultra-luxury end, brands target India's wealthiest consumers, often referred to as India1 Alpha—the highest disposable income segment, catering to elite buyers seeking exclusivity, craftsmanship, and heritage-rich designs.

India’s jewelry industry, built on centuries of craftsmanship, trust, and deep cultural significance, is now evolving into a global force. While traditional players continue to dominate high-value purchases, shifting consumer preferences, new luxury entrants, and international supply chain dynamics are shaping the next growth phase.

Despite rapid e-commerce growth, offline stores remain crucial, offering touch-and-feel assurance, customer service, and grievance resolution.

By 2024, India’s new-age brands in jewellery had also cemented themselves as here to stay. CaratLane had a blockbuster acquisition worth 17,000 Cr, a journey almost 17 years in the making. BlueStone filed to go public. The duo started with very diverging paths, and CaratLane ended up winning. But the two have succeeded in their ways, making the market attractive.

There is an opportunity for not just two but probably 10 new age brands that could build huge companies. Jewelry brands can differentiate themselves based on events (e.g., wedding vs. casual vs. workwear), metals (gold, silver, steel, platinum), or usage frequency (daily wear, occasional, investment-grade).

Each sub-category represents a massive, underpenetrated market, with revenue potential in the hundreds or thousands of crores. As India’s jewelry industry enters this new phase, the convergence of heritage craftsmanship, global demand, digital transformation, and rising consumer aspirations is creating unprecedented growth.

The market is ripe for new players who bring fresh design language, innovative materials, and modern consumer experiences to India’s evolving jewelry landscape.

Whether through omnichannel retail, LGD disruption, or export expansion, India is positioning itself as the world's largest jewelry market and a global powerhouse in design, innovation, and supply chain leadership.

The next decade will define how India cements its place at the pinnacle of the global jewelry industry.

Writing: Keshav, Anisha, Nikhil, Rajiv, Ritika, Shreyas and Aviral Design: Omkar