Oct 3, 2021

Inside BillDesk's 20 Year Build for the Next Innings

Profile

Payments

Finance

Aggregator

B2B

Series E-G

Last fortnight, Billdesk was acquired by Prosus’ PayU for $4.7Bn, making the combined provider the largest online player, and the acquisition the largest after Flipkart.

Enter Sandman into a Niche

It was the year 1999

An IIM A student, Srinivasu M.N had now spent close to a decade working at the Indian conglomerate ITC. He decided to switch his career path to get into consulting and joined the coveted American firm, Arthur Andersen LLP.

Little did he know that Arthur Andersen would connect him to colleagues with whom he’d end up spending the next two decades of his life. Srinivasu would end up meeting his eventual co-founders Ajay Kaushal and Karthik Ganapathy, both also from the IIMs.

The three would gain deep insight from consulting in the financial services sector.

Srinivasu and his colleagues soon decided to bid adieu to their jobs at Arthur Andersen coincidentally right before the firm self-combusted in the wake of the Enron Scandal.

The three wanted to build something in finance. They were crystal clear about not wanting to get into the red ocean of online share trading and lending because the competition in the space was strife.

Banking in India was undergoing a major paradigm shift. Banks were investing in core banking platforms and moving away from brick-and-mortar branches.

To add to it, India’s internet user base stood at about 50,000 at the time, but people were still standing in long queues to pay any bills, be it phone bills or electricity bills.

The trio realised that there is a business opportunity in building a layer of services to assist banks in going digital.

With tenets of simplicity and convenience strongly ingrained into their thinking, the three of them decided to build a convenient payment platform that would enable them to be partners to banks.

IndiaIdeas.com a.k.a BillDesk was born, becoming the earliest harbinger of the Indian fintech ecosystem.

Nothing Else Matters But E-Bills

At the time, neither banks nor billers had devised any form of electronic bill payments by then.

BillDesk saw an opening and quickly onboarded banks and merchants onto its platform to integrate their payment technology. This allowed them to connect banks with any merchants or utilities who had to accept payments from customers.

This meant that, at one end, the firm’s technology pipe gathered billing data from utilities like power and water suppliers and phone companies. On the other, it collected paper mandates from banks’ customers to debit the payments to these utilities from their accounts.

The two-sided matchmaker turned out to be a robust system.

The way the model was structured meant that there was no end-consumer acquisition for BillDesk. The company would only take a cut from one of the transacting parties for every transaction it facilitates.

This digital solution would end up being a win-win for all the players.

Customers no longer needed to line up to pay bills. Utility players didn’t have to spend millions of man-hours reconciling bank transactions. Banks didn’t have to deal with physical payments where customers clogged up their branches.

In 2000, BillDesk had successfully tapped a niche market, because it was online.

However, the payments solution always maintained the ethos of staying in the background, steering clear of the limelight and allowing banks to brand and operate their solution.

The company decided to keep their heads down and focus on building demo solutions for showing how it all worked, to convince banks and merchants to try it out

Staying in the background, steering clear of the grow-big-at-any-cost fintech model and performing product demos turned out to be a good strategy for the firm as they ended up forging relationships with multiple banks across the country.

BillDesk was now ready to fly, but it needed money to do so.

Sweet Dreams Are Not Made of VC

In 2001, there was no venture capital ecosystem to speak of.

BillDesk raised its first funding of $500K from a nationalised bank and a fund run by a regulatory body.

It’s interesting to note that both of these backers were government-owned and the antithesis of today’s high-profile, global venture capital companies.

In the years that followed, the company managed to build a roster of clients and was offering its gateway to multitudes of customers making payments in India.

For BillDesk, slow and steady growth was the way.

They ended up building a payments processing network with 25 of India’s largest banks including the likes of SBI, Citibank, HDFC and leading companies such as LIC, BSNL, Hutchison-Essar, Franklin Templeton, etc.

BillDesk had built a leading position in the electronic payments services market in a very short period of time and Investors were vying to support their rapid growth to help them further dominate the market.

By now, the company had reached a fair amount of maturity in their business model and was looking to expand into tier-I and tier-II cities as well as launching new products in the market.

In 2006, more money followed as a US-based venture capital firm along with India’s largest public sector bank decided to invest $7.5M into BillDesk.

With no incumbents or competition in the fintech space, BillDesk was steadily chugging ahead like a steamboat.

The steamboat wasn’t leaking, it was gathering steam along the way.

A Profitable Rainmaker

In a market without access to capital, BillDesk had to perform with good economics and steady growth.

By 2007, the game was in understanding which elements of the payment chain to target. While a plethora of new players on the block targeted the consumer, BillDesk’s founders had other plans.

Going directly to consumers meant operating with a heavy cash burn model.

When Billdesk started operations, India wasn’t ready with the consumer and internet digital base. Founders knew very well that they were early in the day for a payments tech play and hedged this risk by adopting a pure B2B route.

BillDesk understood unit economics like age-old business. Provide quality services, create real value, and take a cut home.

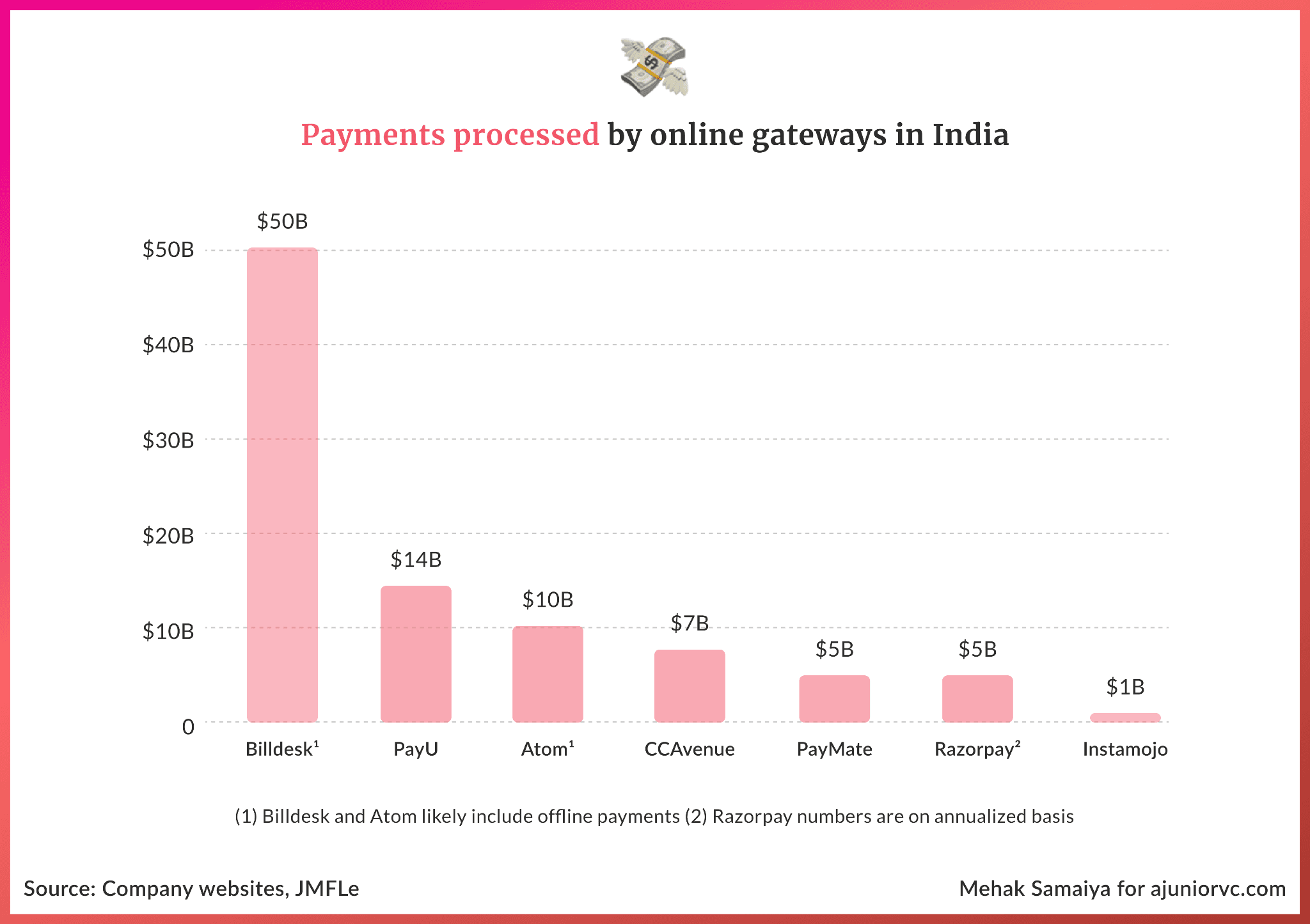

Because of the early head start, BillDesk turned profitable in 2008 and grew quickly without a lot of competition barring CCAvenue, which started its shop in 2001.

Market tailwinds like an increasing internet consumer base, solidifying infrastructure and demonetization, gave a powerful push to BillDesk’s topline – further strengthening its position as a market-leading platform for online bill payments.

Essentially a payment gateway, it made its revenue from a cut of Merchant Discount Rate (MDR).

MDR is a fee levied to Merchants for accepting online payments in exchange of services provided by the payment gateways and networks like Visa/ Mastercard and banking entities.

MDR is made up of Payment Gateway Fee, Payment Network Fee, Acquiring bank Fee, and Interchange fee to Issuer Bank.

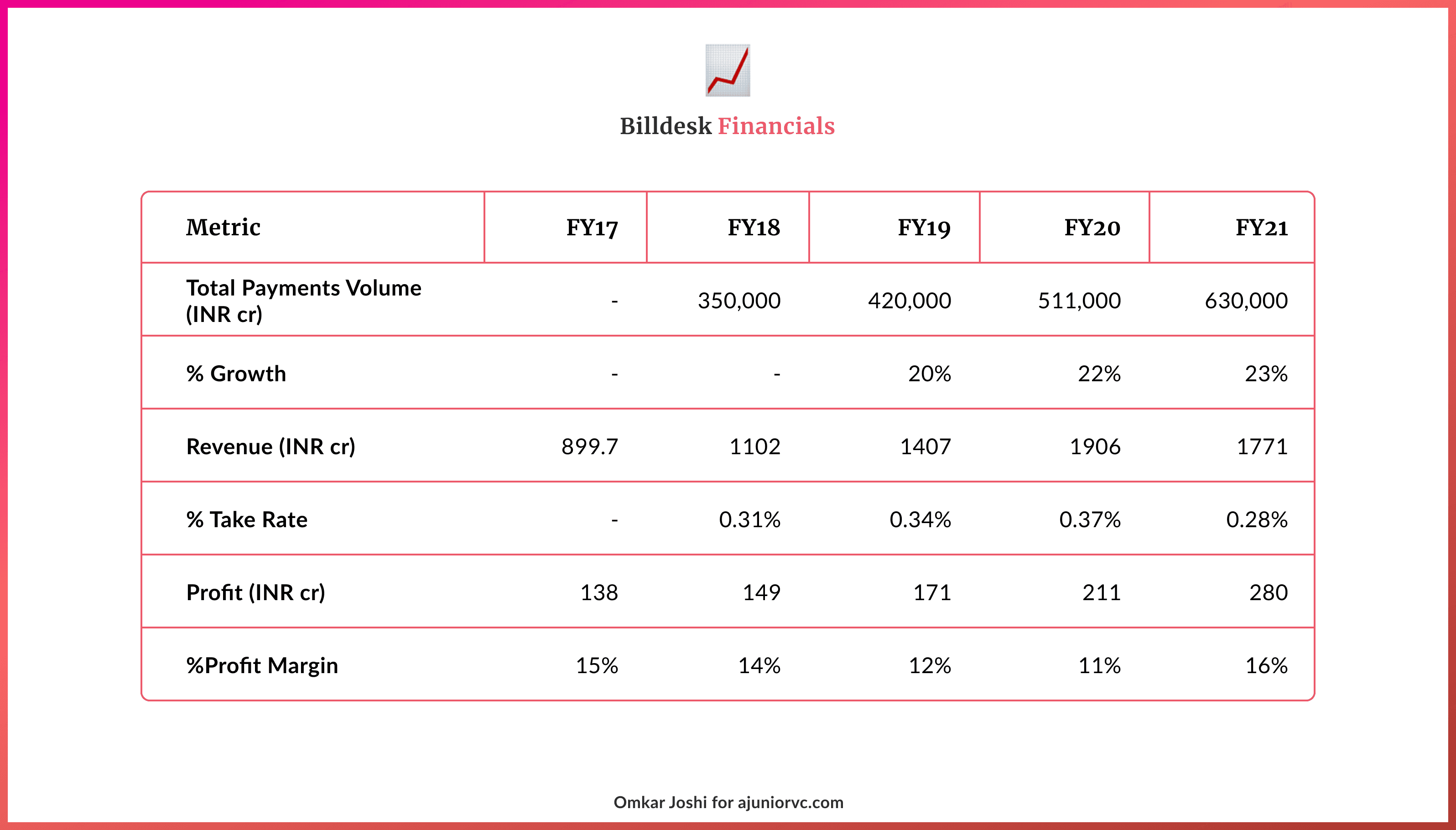

BillDesk’s Take Rate was ~0.3% of the total Transaction Payments Volume (TPV) going through its platform.

With very healthy profit margins, and a constantly rising TPV which was ~20% YoY growth, in alignment with the market numbers for digital payments on an upswing.

BillDesk was showcasing sheer dominance.

Lead The Lightning Fast Digital Processing

BillDesk’s timing was unique. When no player existed, they made a market for themselves.

The markets rewarded them well for starting early. With little to no competition, BillDesk would turn out to be the winner in the race.

From the start, it held the majority market share. It would turn out to be the market leader in online bill payments with tie-ups spreading across 100 billers in the country.

These marquee metrics would be a result of BillDesk’s vision early in the day; the founders built for a system, decades in advance.

Parallelly, Bharat was building its India Stack, which would be the much-needed fuel to the engine.

As it entered the 2010 decade, India was transforming and Billdesk was helping with online payments.

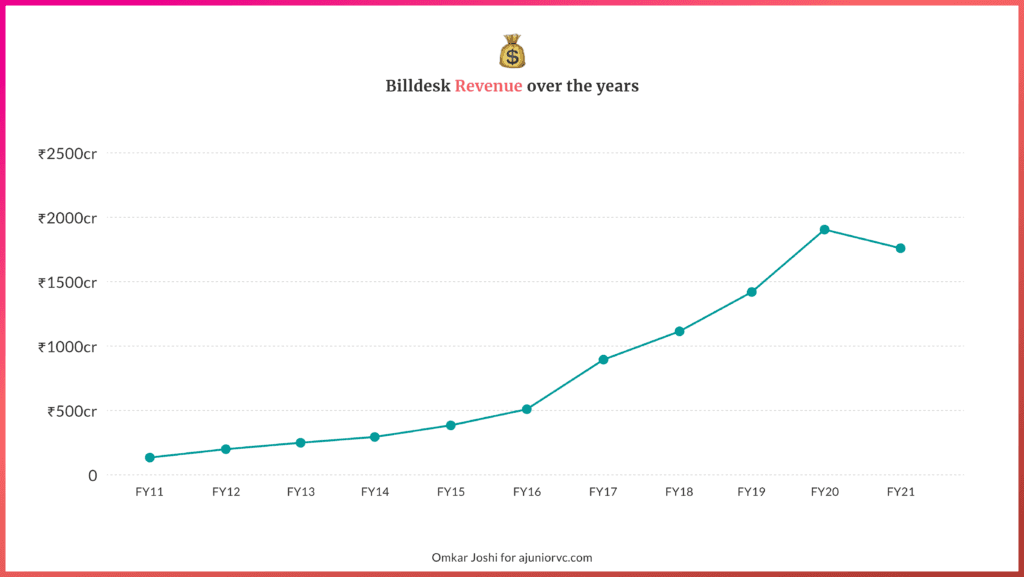

While India’s digital payments was a work in progress, BillDesk was ready for the sprint. Their revenues from over 3x from ~150 Crs to ~500 Crs over the next five years from 2011 to 2016.

As countries like China by then already had solid mobile payments systems, Indian companies knew that even the Indian market would be disrupted soon or later. This was the time when BillDesk was building to integrate India’s digital payments stack in silence.

Come 2016, news about UPI flooded the market. Fintech companies went berserk, while the public awaited the most flawless payments system in the world.

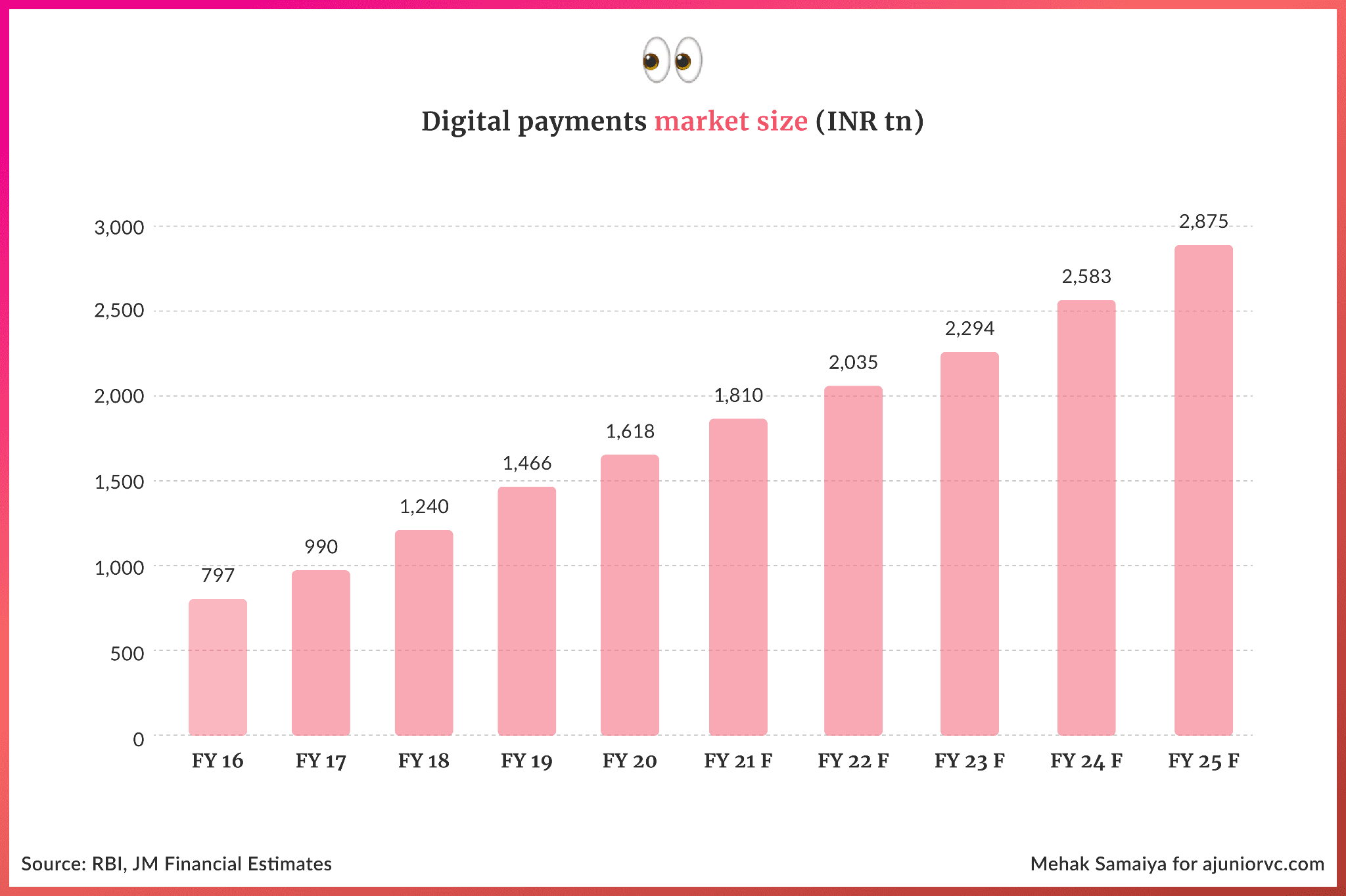

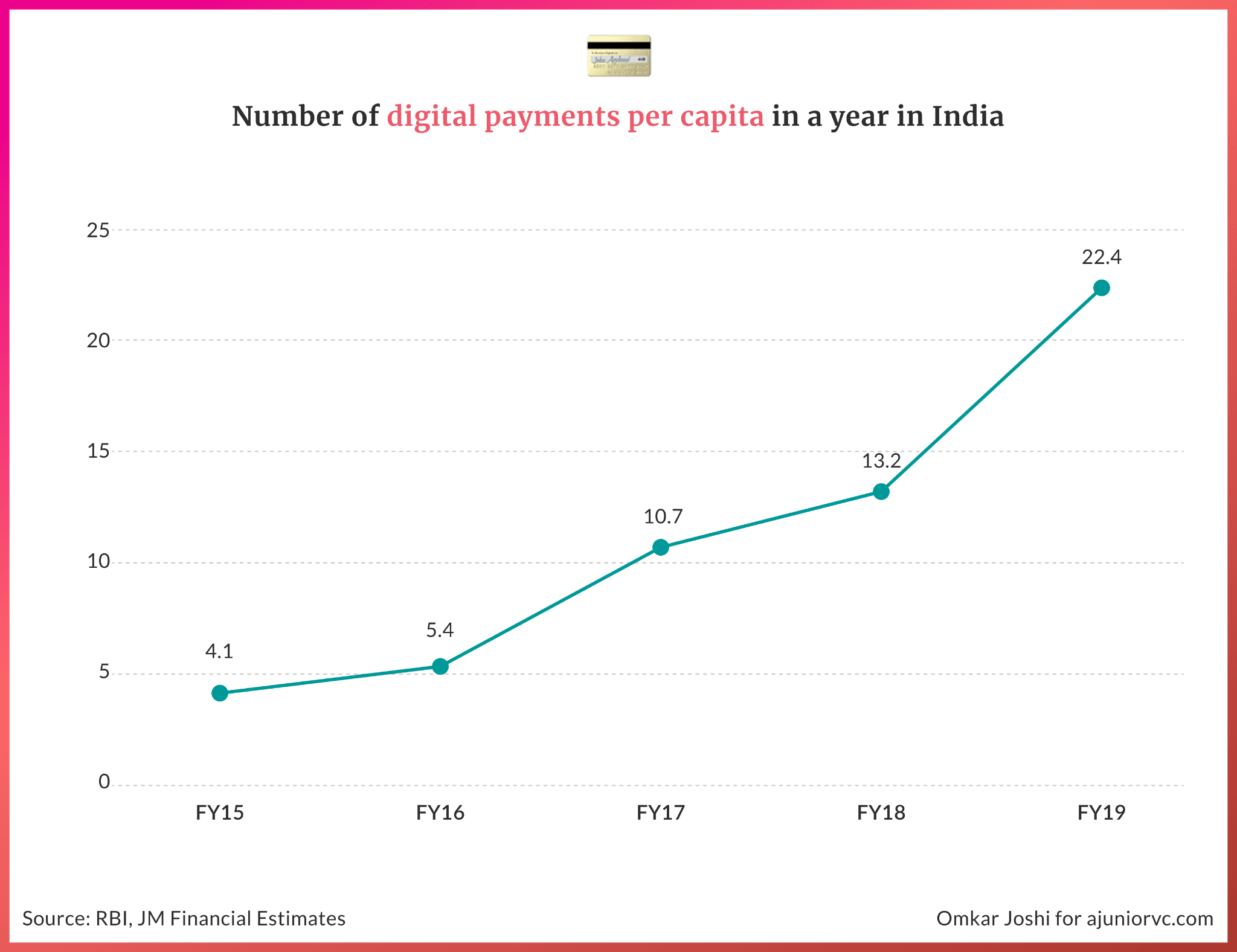

Digital payments in India went for a home run with a per capita growth of 4x over the next three years.

Challenging the Champion In The Ring of Gateways

By 2017, BillDesk’s run was no less than a gold rush.

It had been profitable for more than a decade – unheard of in the startup ecosystem. But ever since demonetisation and UPI, fintech have been forced to change for good.

This included giants like BillDesk.

Newer competitors that were emerging in the space were entering through the e-commerce segment, by offering payment solutions and making themselves attractive to the upcoming startup ecosystem.

Billdesk didn’t compete there just yet, it instead started partnering with some of these newcomers.

It still continued to be the market leader processing 60% of the online bill payments in India. For any player to beat this lead organically would have meant an easy 5-7 years of sheer evolution and constant innovation.

The player eventually joining hands with Billdesk didn’t only create a consolidated leadership in B2B plus B2C play. It bought 5 years of experience; 5 long years that would have to be spent building trust.

This translated into growth for Billdesk, marking an 80% growth over the last two years as the country’s digital payments infrastructure grew exponentially. The same is reflected in BillDesk’s valuation as well, which in FY 18-19 was pegged at around $2bn.

However, with passing time and growing scale, BillDesk began showing some signs of being a traditional incumbent.

The company reached a steady-state, with the management keen to keep the cash flows from existing products at levels that would ensure profitability over everything else.

This opened up an opportunity for upstarts to challenge their dominance. Several competitors emerged riding on the back of venture dollars and investors who encouraged them to chase growth at all costs.

The champion was being challenged.

You’ve Got Another Thing Comin’

By 2020, while BillDesk was razor-focused on sustainable profitable growth, their competition was ready to operate at negative gross margins.

This was in order to grow and catch up. Challengers to BillDesk began offering merchants super attractive rates to win their business.

This was evident when the Life Insurance Corporation (LIC) was renewing the deal to manage its payment gateway provider. LIC wanted someone who would offer cheaper take rates than its existing provider, BillDesk.

Paytm won the tender with an aggressive bid as it had other avenues to make money. LIC had registered 80 million transactions worth over INR 60,000 crore in premium collections on its digital platforms.

The growth of some of the newer payment gateways is further proof of this reality. In FY17, Billdesk was 15x larger than Razorpay in terms of revenue. By FY20 Razorpay had clocked more than double the growth rate of Billdesk and half its revenue.

The gap is likely to have narrowed further. Even in terms of the transaction value for FY21, at $55 billion Razorpay is just half of BillDesk.

The upstarts have been able to steal a march on BillDesk by focusing on markets traditionally ignored by BillDesk and the broader traditional banking system. They target SMEs and innovate on new products that they bundle with their existing products.

The new payment gateways also didn’t just want to be gateways.

They successfully managed to bundle other services like a digital storefront, human resources management, and ledger facilities apart from lending to the customers to make them stick. RazorPay is in fact, working towards becoming a bank for SMBs.

India is regarded by many as the market with the world’s lowest payment gateway commissions.

BillDesk tackled this by chasing customers that were traditionally harder to onboard and work with (large enterprises and government bodies) thus ensuring better margins, the younger companies in their space have looked at lending as a primary source of revenue.

Taking note of how fierce the atmosphere was, BillDesk was already planning its next move as 2021 started.

Mergers For Whom The Bell Tolls

The founders have been on a 20-year journey of building BillDesk since January 1, 2000.

Since then, the company has managed to scale to $100BN in TPV, $253 Million in revenue and $42MM in EBITDA. In fact, the company has been profitable since 2007.

Recognizing their duties to their investors, the management had been exploring various liquidity options for their investors, some of whom had been on board for 15-16 years. To that end, BillDesk had been exploring various options in the past 3-4 years including an IPO and a strategic sale.

However, given the size and scale of BillDesk, the universe of strategic investors was limited.

Several of the larger global players have stayed away from the Indian market due to the thin margin structure of the industry and the fairly robust ecosystem of local players existing in India.

Given Visa’s investment in the company, they would have made a logical home for the company. But the two largest Payments rail providers globally Visa and Mastercard have been shy to make outright acquisitions, instead choosing to make opportunistic investments in various new-age fintech companies.

Earlier in 2021, as the founders of BillDesk began the process of evaluating an IPO given the favourable market condition Prosus reached out to BillDesk for the first time.

The rest, as we know now, is history.

From BillDesk’s perspective, Prosus acquisition offer represented the right mix of financial investment and business strategy while also providing them with the impetus to grow aggressively going forward given their ability to continue to invest in the business.

The BillDesk acquisition for Prosus makes sense on several levels. BillDesk is the largest player both in the bill payment space and the payment aggregation space, counting close to 5K large enterprises as customers.

It is deeply integrated with the banking ecosystem and with utility companies and is furthest along on enabling subscription payments. BillDesk’s Standing Instruction (SI) Hub is the only platform in the country that can process recurring payments with additional security as mandated by the RBI, giving it the monopoly power for such payments.

The company also manages mutual funds and systematic investment plans for many mutual funds too. Even within the Bharat Bill Payment System, most of the bank-end is run by BillDesk.

By bringing together the two complementary businesses, the acquisition can be expected to create a fintech ecosystem handling 4 Bn transactions annually. That is four times PayU India’s current level.

PayU has a robust presence within the SME e-commerce market, which complements BillDesk’s modus operandi perfectly.

India’s 2nd largest acquisition being in fintech was a signal of the times to come.

The Times of India Are A-Changin’

This massive acquisition takes place at a time when the Indian payments sector is gaining traction.

According to the Reserve Bank of India’s (RBI) FY21 annual report, the volume of digital retail payment transactions surged by more than 80% from 24 billion in 2018-19 to 44 billion in 2020-21.

The RBI estimates more than 200 million early adopters to use digital payments over the next three years, with estimated yearly transactions per capita jumping tenfold from 22 to 220.

Recognizing this opportunity, Prosus has been consolidating its foothold in the Indian payments space through PayU. BillDesk is PayU’s fourth acquisition in the past five years, following the $160 million takeover of payments technology startup CitrusPay in 2016.

Prosus acquired security firm Wibmo for $70MM in 2019, and in 2020, it spent $185 million acquiring digital credit company Paysense, which currently drives its consumer lending objectives in India.

PayU’s strategy is three-fold. It wants to build a large business in payments; be an innovator in digital credit and wants to have a full financial services ecosystem.

BillDesk helps fill a key gap in PayU’s offering in terms of the type of customers it currently has on its platform. The BillDesk team, which plans to stay on post the acquisition, will be another asset for the PayU platform which is not spoken of enough.

With capital at their disposal thanks to the parent Naspers and a combined business that generates plenty of free cash, one should expect some aggressive moves by these companies.

BillDesk scaled in a world when internet adoption was still low and trust was lower, which means they understand what it takes to build trust with the consumers and merchants. As the next billion users come online and India’s online transacting user base expands beyond the 150MM that it is today, it will be important for payment enablers to help inspire trust amongst this group of consumers.

Who better than BillDesk to be able to do that?

The Indian fintech sector, especially startups, has seen support from the government and progressive policy in this sector has helped grow this sector manifold. India’s leadership on a global scale in fintech is well documented, so much so that Google has approached the Fed in the US to build a payments stack like India’s.

It is only deserving of this leadership that we have a company that is able to represent this success on a global scale.

With the acquisition of BillDesk and its ever-expanding product portfolio, PayU seems in line to do so. As the consolidation gets underway to challenge the new challengers like Razorpay, Indian fintech has entered an exciting new phase.

As it enters a new home, a lot remains to be done. As it finishes its first innings with a merger, BillDesk is building for its Next Innings in an even larger form.

Writing: Bhoomika, Chetan, Saniya, Varun and Aviral Design: Mehak, Omkar and Saumya