Apr 16, 2023

Can EVs Energize India’s 15 Year Old Ridehailing?

Aggregator

Series H+

B2C

Transportation

Last fortnight, Delhi HC imposed GST on auto rides, hot on the heels of reversing a ban on bike taxis in an interesting year for ridehailing

Hail Meru

During World War 2, an uncontrolled increase in production resulted in shortages of raw materials, particularly rubber.

The US government decided to source extra rubber from an unlikely source - car tires. The premise was simple, each car had four tires and could serve five people per ride.

At that point, less than two people on average were served.

If people would share their rides and donate the extra unused tires to the government, sharing would solve the rubber supply issue.

This led to the emergence of ridesharing as a concept in the 1950s. Car taxis started in Europe in the 1900s and picked up worldwide.

The ridesharing industry was born.

In India of the 1990s, taxis emerged to take people who did not own a car to places they could not travel to by bus or other public transport. A Mumbaikar could get into an iconic black and yellow(Kaali-peeli) taxi, and the genteel ‘taxiwala’ would put the meter down, and off they would go.

One such Mumbaikar, Neeraj Gupta, regularly picked up and dropped off his wife at the airport for her job at Jet Airways. He wanted to make this easier by setting up a shuttle service to the airport.

In 2001, he established a shuttle service for corporates to shuttle their employees to and from airports in high-quality buses. His services captured major demand from companies looking to transport their employees to the airport, such as Tata, Sony, and Blue Dart.

As the demand for Neeraj's transportation services grew, he expanded his fleet to include cars, ultimately growing to 1,300 vehicles in just four years.

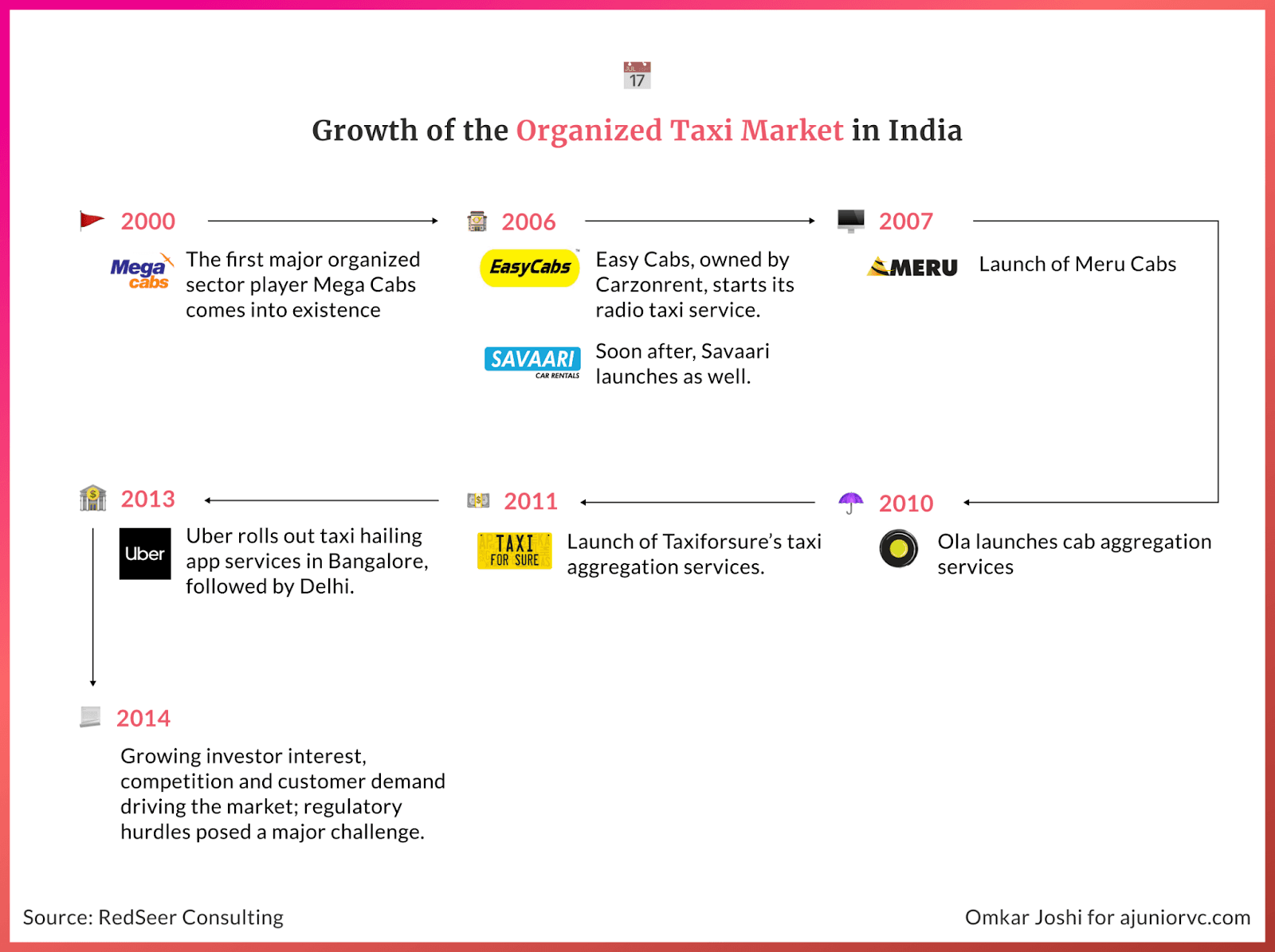

In 2006, he won a major tender from the Maharashtra government to supply 10,000 air-conditioned, electronic-metered taxis in Mumbai, leading to the birth of Meru Cabs.

Meru set out to create a world-class radio-taxi service across all major Indian metros.

Customers could pre-arrange a Meru cab over the phone. The vehicle would come equipped with an electronic meter that couldn't be tampered with, air conditioning, printed receipts with payment details, and GPS/GPRS systems to track the distance travelled accurately.

Meru educated their drivers in traffic rules, hygiene, geography, and the latest technologies to ensure a high level of service.

Meru's smart back-end technology allowed for automating service processes and standardization of the customer experience, making it an instant hit.

In 2009, Meru disrupted itself with a subscription-based business model. Under this model, the driver was no longer an employee of the company, but rather an entrepreneur who paid a deposit of Rs 10,000 to be assigned a cab.

Meru owned the customer acquisition process, car inventory, and maintenance, while the drivers offered their services through Meru.

This business model worked well, as drivers took more ownership of their work and responsibilities, earning anywhere from Rs 1,000-1,500 a day, depending on the number of trips.

Meru was now operating 3,000 vehicles daily across four metros, employing more than 700 people, and netting in ~Rs 100 crore in revenues. They also secured exclusive relationships with the four major airports in Mumbai, Bangalore, Hyderabad, and Delhi, becoming their official taxi-hailing service.

Meru became the largest radio-taxi company in India, pioneering a new ridehailing industry.

However, with the massive potential of the industry, tech-savvy competitors were beginning to make inroads.

Say Ola

A 1000 pound gorilla called Uber was quietly expanding its services internationally.

Uber focused on convenience, allowing users to hail luxury cabs from their phones within minutes, without owning any cars.

This caught the attention of two IIT Bombay graduates, Bhavish and Ankit, who pivoted their car-rental startup to a tech-first ridehailing service, giving birth to Ola Cabs in 2010.

Ola, which means "hello" in Spanish, focused on building a friendly yet simple ridehailing brand operating on a model similar to Uber. It did not own or operate its fleet but aggregated small fleet operators and single vehicle owners, making money by charging the cab driver a commission on each ride booked.

Ola launched an easy-to-use mobile app that allowed customers to order a cab at the tip of their fingers. The app offered an in-built feature to identify the driver's location through GPS, allowing customers to track their booked cab on a map on their cellphone until it reached their location.

In 2013, Uber entered the Indian market, heating up competition in the ridehailing space for Ola and Meru. While Uber was a competitor to be feared, Ola made some changes to adapt to the Indian consumer.

Ola focused on small hatchbacks to offer affordable rides while Uber focused on tapping the luxury segment. Ola also allowed users to pay for rides using cash, a popular payment method in India. In contrast, Uber primarily used cashless payment methods such as credit cards and digital wallets, which Indian customers did not widely adopt then.

Both Ola and Uber offered mobile apps that allowed users to book rides, but there were some differences in the features they offered. For example, Ola's app had a feature called "Ride Later," which allowed users to schedule rides in advance, while Uber did not offer this feature until later.

The success of mobile-first Ola and Uber was aided by an exponential increase in India's mobile penetration, from about 35% in 2009 to over 75% in 2012, meaning there were over 900 million mobile phone subscribers.

With Ola and Uber entering the fray, it became difficult for Meru to change its business model, which worked well for high ticket sizes in the range of ₹500-600. Ola and Uber were designed for high frequency, multiple short rides, and small ticket sizes, making it hard for Meru to compete.

On the sidelines, an unlikely Bangalore-based competitor named TaxiForSure was quietly building a more budget-friendly competitor to Ola and Uber.

TaxiForSure differentiated itself by offering lower prices, a diverse range of vehicle options, and a wider fleet.

Meru suddenly surrounded with serious competition, completely upending its model and almost decade long dominance.

Duopoly Driving Away

In 2014, as Indians warmed up to the convenience of calling cabs on their phone, the taxi market was expanding rapidly.

The radio taxi market was estimated to be worth $9 billion and growing at 17-20%. The number of organized taxis was set to reach 30,000 in 3 years, as nearly 10 fairly large companies were pushing for growth.

However, the market was expected to consolidate to two players - homegrown Ola and global giant Uber. Both companies relied heavily on technology to provide reliable and timely service, a concept new to Indian consumers then.

The consolidation to two players was driven by largely by network effects.

Acquiring user demand would onboard driver supply which would further acquire user demand. This cycle was virtuous and helped the 2 companies scale rapidly.

But economics is one thing, execution is another

While Uber had already operated for four years in the US and other countries, India presented unique challenges. Price-sensitive customers, a limited supply of good quality cars, and poor public infrastructure were critical.

To overcome these challenges, Uber adopted a different strategy in India. The company attracted customers by offering high-end cars at prices that seemed too good to be true - customers could get an Audi for the price of an auto-rickshaw ride.

Over the next few years, Uber implemented growth-hacking strategies that would later become business school case studies. The company introduced referral codes that allowed users to get free rides when their friends signed up, and users eagerly shared codes on social media, becoming the company's biggest promoters.

As more customers joined the platform, more drivers were willing to sign up, thanks to network effects.

To increase supply, Uber quickly expanded its product offerings from premium cars to smaller sedans and hatchbacks. The company was fueled by venture capital and quickly gained market share, making cab-hailing second nature to urban Indians.

From mid-2014 to the end of 2015, Ola's weekly active users grew from approximately 1% of overall mobile device users to 9%, while Uber grew to 5.7%. These numbers show that both companies were becoming important components of many mobile users' lives in India.

Ola raised $700 million to fend off local competition and used the cash to drop fares even further and expand into smaller cities. Ola introduced "Ola Mini" to match "auto fares" for cabs, dropping prices to as low as Rs. 10 per km for mini cabs and Rs. 13 per km for sedans.

TaxiForSure, which did not have the resources to survive a price war, had to pay taxi drivers the deficit and splurge on acquiring new customers.

By March 2015, TaxiForSure was acquired by Ola for about $200 million. The company could not raise more funding due to increasing regulatory scrutiny and uncertain investor sentiment.

Ola and Uber rode on, but were about to be hit with another storm.

Regulatory Roadblocks

The fast-paced growth hit a roadblock when a safety incident occurred with a woman passenger in an Uber cab in Delhi.

Uber offices were shut and banned from the city.

Indian regulators started to understand better the cab aggregator business model and the detriments of rapid expansion. They began to look closer into driver screening, licenses and passenger safety.

While the authorities began forming regulations, Uber’s tenacity and the value proposition cab hailing provided allowed it to wriggle back into action.

Ola continued to play the discounting game. Ola slashed prices for the Mini to Rs. 8 per km and Rs. 11 for the sedan to undercut Uber.

Even Meru joined the discounting race with cashback offers of up to 30% . They even tried running promotions on the radio, urging people to download the app. They focused on 14 to 15 km trips, with Rs. 20 per km pricing and higher payout to drivers.

There needed to be more to combat the rapid customer acquisition from the duopoly. They started to operate categories other than cars.

In March 2016, Uber started bike taxis, and Ola followed suit in 24 hours. The bike taxis supported short-distance commutes in cities with almost a Rs. 3 per km price point.

Ola allowed users to pay using its wallet, Ola Money, and supported cards and cash. Unlike its operations anywhere else, Uber allowed cash in addition to cards for their rides.

By the third quarter of 2016, Ola clocked about 6 million weekly rides across offerings. Uber wasn’t far behind with 5.5 million, which had risen from 1.6 million the same year.

In addition to bike taxis, auto rickshaws, and alternate payments, the platforms introduced another important lever that facilitated growth - ride-sharing.

Multiple people moving in the same direction could hop on and off the same cab. Costs reduced even further and brought in more people who could not afford a cab.

Both companies also aggressively marketed outside their top Bengaluru, Delhi and Bombay markets. Ola doubled down on smaller cities and launched the ‘Micro’ segment of cars, with fares as low as Rs. 6 per km.

Ola expanded to about 120 cities, spreading itself far, while Uber focused on going deep in 40 cities.

Uber kept up the price war, with UberGO offering prices in the same range.

After Uber sold its China business to Didi Chuxing, India was a market it couldn’t afford to lose. No other geography provided as many internet and mobile users making it worth the fight.

By 2017, regulation started to catch up stronger. Both companies had accumulated many complaints about driver misbehaviour. Some would lead to sexual assault.

Both firms started to put in place measures such as displaying a photo of the driver along with vehicle registration and model details. They also added features that allowed riders to share trip details with friends and family and a panic button to alert authorities.

They set up safety response teams on standby to be available in case of ride deviations or unplanned stops. Ola launched the one-time authentication to start rides.

While these features helped improve trust somewhat, they increased operating costs.

Both companies needed to look for alternate channels to soften the bruising price war and retain customers sustainably.

The SuperApp Crash

While the slugfest for Indian customers continued, Ola aimed to take the fight abroad.

In early 2018, Ola entered Australia and eventually New Zealand and the UK by the end of the year. The company also raised $400 million to fund expansion on multiple fronts.

Back home, the battle for cab rides expanded to include a struggle for food deliveries.

Uber Eats launched in India around May 2017. Soon after, Ola acquired Foodpanda’s India business. Ola briefly dabbled in the space with Ola Cafe in 2015, but shut it down due to poor performance.

Expanding to the food business sounded logical.

Ola and Uber already had a presence among 100 million Indian customers, built logistics capabilities and mobile technology in search, experience and payments.

However, on ground, the strategy needed to be more sustainable.

To take market share away from segment leaders Swiggy and Zomato, the companies had to burn cash on three fronts - deep customer discounts, higher pay for restaurants and generous driver partner incentives.

Given the mounting losses in the cab-hailing businesses, this proved an expensive game for both players.

The Foodpanda buzz soon fizzled out and Uber sold UberEats India to Zomato in an all-stock deal valued at $206 million.

While Ola pivoted away from food delivery, it continued to build a portfolio of food brands under Ola Foods, a network of cloud kitchens spread across the metro cities.

It turned into a brand-based offering, with some restaurants also listed on Swiggy and Zomato, in an attempt to collaborate and not compete.

Back in the mobility space, too, the competition was heating up. Not for cabs - no players had noticeable scale yet - but in the bike segment. Bengaluru-based Rapido was gaining traction in the smaller towns and cities.

Starting in 2015, Rapido realised that adding more cars would only add to the traffic woes of the metro cities. Instead, they saw two-wheelers as a faster and more affordable alternative.

In their home ground of Bangalore, Uber and Ola had already added bikes to their platforms. Rapido didn’t have the resources to play the discounting game and sought new ways to stay alive.

Post an investment from the Munjals of Hero Motor Corporation, Rapido focused on Tier 2 and 3 cities - a territory still thinly populated by the more giant aggregators. The proposition provides rides to daily commuters without vehicles and allows bike owners to earn a side income.

The investment allowed Rapido to define a turf away from the price wars. The company increased revenue by 13 times, crossing the rupee 50 crore mark in 2019.

On the theme of affordability, Rapido started adding autos to capture a broader market and use case.

In the metros, the big boys had already expanded services available on the app to autos, bikes, premium cars, rentals and shuttles. From cab-hailing disruptors, they sought to become all-in-one mobility solutions.

By 2019, Uber clocked 14 million weekly rides across 58 cites, and Ola did 28 million rides from the 250 cities it operated in across two, three and four-wheelers.

By providing ways for Indians to move, Indian mobility companies were in high gear and moving fast.

They were about to be hit with a body blow much harder than regulations

COVID Carwreck

After the first COVID-19 outbreak, Ola and Uber had to suspend their cab-sharing service.

In the days leading up to complete lockdown, the fear of COVID-19 caused demand for Ola and Uber to decrease by 50%.

They tried reducing fares and implementing basic safety protocols to tackle this unfamiliar situation. Then, when the lockdown occurred, cabs were completely suspended from roads, causing business to plummet to zero.

Ola's revenue fell by 95% in April and May, prompting the company to announce a mass layoff of 1,400 employees to preserve cash during the time of uncertainty.

With the unpredictable nature of recovery, Uber followed suit by laying off 6,700 employees globally, including 600 in India, and closing its Mumbai office.

Even before the pandemic, Uber tried improving profitability and focusing on its core operations and markets. In early 2020, the company sold UberEats to Zomato. After the pandemic, Uber closed its operations in several countries in North Africa and the Middle East to cut its loss-making endeavors and focus on long-term profitability.

To survive, these ridehailing companies started using their huge fleets for other purposes. Both partnered with grocery delivery companies like BigBasket and Grofers to meet their huge demand.

They also started providing services to transport patients safely to hospitals and coordinated with local authorities and hospitals to transport frontline workers and essential medical supplies.

Although both giants had invested in 2-wheeler taxis, most of their fleet was 4-wheeler, making bike-focused aggregators like Rapido and Vogo better placed to pivot to assist the grocery delivery space. Rapido and Vogo also launched their service for hyperlocal logistics.

Ola and Uber were poised to revolutionize sustainable transportation, provide affordable rides for customers, and increase profits for cab companies. However, due to the pandemic, the temporary suspension of ride-sharing became permanent.

As lockdown norms eased, Uber and Ola had to innovate to survive.

They returned to the "new normal" in India with safety precautions such as temperature checks, car sanitization after each ride, and plastic screens between drivers and riders.

However, with offices and schools still operating remotely, business for ridehailing firms remained subdued.

Turning the Wheel Around

From being a low-cost service provider to the safest service provider, ridehailing companies had to pivot their approach in the wake of the pandemic.

Customers' priorities shifted from saving money on commutes to ensuring health and safety. Ola adopted the "My Safest Ride" protocol and shifted its positioning from the lowest-cost provider to the safest provider.

However, the work-from-home trend had been a significant obstacle for ridehailing companies as IT employees accounted for a significant percentage of rides. Trips to airports, tech parks, and big office zones were not happening.

The pandemic also saw many drivers defaulting on car loans due to decreased income, active drivers for Uber and Ola went to less than 50%, resulting in fewer vehicles as demand gradually increased. The drivers that are abe to survive were faced with higher fuel prices, high maintenance cost and fewer rides

By 2021, both Uber and Ola experienced a surge in demand as the economy recovered from the pandemic. Uber reported a 105% year-over-year increase in gross bookings in the second quarter of 2021, and Ola's ridehailing business grew by over 110% in July 2021 compared to the same month in the previous year.

People have been avoiding public transport and opting for "safe" infrequent cab rides, leading to a surge in auto-rickshaw rides. Bike taxi players had also revamped their infrastructure, replacing petrol vehicles with electric ones.

As commuters seeked safer and more affordable options, they increasingly turned to bike and auto-rickshaw services.

Daily rental cab bookings have risen as people want to avoid making multiple bookings. Demand for outstation travel has risen as Indians have started "revenge travelling" and commuting to their hometowns.

During the second wave, monthly active users (MAUs) of Ola and Uber fell 25.2% over March to May 2021, compared to a 44% drop from March to April 2020.

However, both companies were better prepared for the pandemic this time, and commuters have adapted to the new normal.

By March-end Ola’s volume recovery had bounced back to 69% of pre Covid levels and by August 21 their volume was at par with the pre-covid levels.

Ola even reported their first ever profit for FY 2022, profitability was driven by sharp fall in expenses, even though the revenue dropped by 65% to 690 crores, they were able to post a profit of 90 crores as compared to a loss of 610 crores.

During the pandemics uncertainty Ola had taken bold steps to cut expenses, and with the recovery in demand, they could still function at low operational cost.

The situation dramatically flip-flopped with Uber and Ola choosing an opportunistic approach to recover business through higher fares, lower driver incentives, and reduced staff.

Auto Rickshaws, the dusty, hot and uncomfortable alternatives to cabs made the biggest comeback post lockdown, no one wanted to ride in a closed AC car in a pandemic. With aggregators coming in play there was no need to exchange cash with the driver during the pandemic.

All ridehailing companies were rushing in to capture the auto market.

By the end of 2021, Auto industry was doing 1.5x volume compared to Jan '20 while Moto and Car taxis just reached the pre pandemic level. After the second wave autos saw sharp growth.

Rapido, known for bike taxis, was generating near half of its revenue from Auto Rickshaws. It also announced it would double its business compared to pre-Covid levels by the end of 2022, and Vogo raised $11.5 million in funding. These bike taxi companies were having a gala time along.

With simpler times kicking in, and 100% recovery in GMV of ridehailing companies, things were starting to look better.

But a new variant was coming in, looking almost like the first variant of ride hailing cabs.

Electric Disruption

In 2022, EVs became popular due to the carbon footprint narrative, but the cost of ownership remained higher than a combustion vehicle.

Buying an EV for taxi purposes was 12L versus a combustion vehicle that cost 8L. Although the fuel and charging costs differed, with the former being an expense of nearly 24K versus the latter just 5K.

EVs could save money in the short run.

EV usage at scale was relatively new, and the aging of the cars had yet to hit. Still, as time progressed, EV maintenance and servicing became one of the most expensive headaches. This was due to the lack-of-knowledge syndrome and inexperience to work with batteries and EV engines.

In 2019, BluSmart entered the Indian ridehailing market with a fleet of electric sedans, offering a premium experience and environmentally friendly service. Its business model was similar to Meru's, prioritizing quality and price.

BluSmart owned and operated the vehicles. Owning EV fleets, but they did not scale as much as Ola or Uber did in the same timeline.

BluSmart owned 1800 cars from Tats Motors, but aimed to increase to 13.5k. It had other partnerships with Mahindra and Mahindra, and its charging stations had partnerships with Jio-BP.

Due to the limited car availability, it served only a set number of premium routes, which worked in their favor as the unit economics were better than the other ridehailing cars and their model.

Unlike other ridehailing companies, they contracted their drivers and paid them a fixed 20-30K salary plus incentives based on rides, which was the right way to do it.

This increased BluSmart’s costs but owning the cars and running the show proved to be a winner.

With frustration on Ola and Uber’s drivers cancelling and being unpredictable, BluSmart wowed users with clean cabs and no cancellation. In many ways, BluSmart was channeling MeruCabs to try and disrupt Uber/Ola like they had done to Meru.

Ola/Uber disrupted Meru with price, BluSmart took its cost advantage to disrupt Ola/Uber with quality.

But regarding business metrics, the high capital incentive business was a concern compared to the existing asset-light business models.

Purchasing each vehicle from another vendor, having the charging stations, maintaining the drivers, and technology required attention. If one wanted to do it all and keep the quality premium, then scale became a significant issue, especially with EVs.

The moving parts in EV ridehailing were many

Ownership or decentralization of cars, the scale of charging stations, technological improvement concerning charging stations, government subsidies, different per-unit costs of electricity in different cities, and the mega challenge in today’s environment.

While the current EV ridehailing was winning in the short run with the narrative and the service it provided with the cash burn, it too could lead a path like Uber and Ola over time.

As the old saying goes, time is money, and this cannot be more apt for the ridehailing industry.

The existing players were fighting it out with driver’s payout, contractual agreements, waiting periods, service quality, threats of unions, surcharge price wars, and more. The new EVs were fighting it out with own-operate model, high capital intensive agreements, EVs narrative, scalability issues, and availability issues.

With all the existing issues, the network effects the existing players built were the strong moat.

Electrifying their vehicles could be the solution to their economic woes.

Riding into an EV Future

Ridehailing presents numerous growth opportunities, but it also requires significant effort. Rather than reinventing the wheel, the industry should build upon existing successes.

In India, the ridehailing market is poised to expand over the coming years. Uber and Ola are investing in electric vehicles to reduce their carbon footprint and appeal to eco-conscious customers. However, competition will intensify as new players enter the market and existing companies continue to innovate and expand their services.

To achieve sustainable expansion, companies must use growth metrics that work for all aspects of their business.

Ola and Uber have experimented with various models and structures, such as ridehailing, post-paid services, used car purchases, and quick commerce businesses.

However, some of these ventures, particularly those related to driver financing, have backfired due to high interest rates. Despite these challenges, ridehailing companies have successfully addressed a significant pain point for customers, and their vast distribution networks reflect this success.

The key to success in India is to adopt the best practices from other geographies while accounting for Indian per capita income and consumer travel preferences.

Although ridehailing has been present in India for over a decade, it only accounts for 0.5% penetration compared to the US (over 10%) and China (over 30%). More growth does not necessarily translate to more business; rather, it depends on the usability and preference of the ride-sharing facility.

Most Indians prefer to own vehicles, even though owning a vehicle is more expensive in India than in countries like the US and China. For those who prefer ridehailing services, two-wheelers are the preferred mode of transportation due to their affordability.

India's government invests in electrified public transportation, such as buses and metros, in Tier-1 and Tier-2 cities. However, ridehailing will still succeed and thrive as India's per capita income and consumer preferences continue to evolve.

Currently, office-goers account for nearly 25% of ridehailing business. which is expected to increase as more people enter the workforce and companies pledge to reduce their carbon footprint.

The airport services segment is one of the most profitable areas for ridehailing, and it is expected to grow alongside the airline industry.

ridehailing services today use algorithms to increase revenue by prioritizing certain routes, such as affluent neighborhoods and multiple short rides within a given time frame.

Last-mile connectivity is still a significant challenge for users, and few companies have successfully addressed this issue. Some companies have tried to offer bike-sharing services, but these have not proven successful.

Electric vehicle ride-sharing services could provide a viable solution for last-mile connectivity, particularly when integrated with metro services.

India is a price-sensitive country, so any service offering lower prices with good quality will likely win the market, even among the wealthy. Autos and two-wheelers have been successful in India due to their affordability.

With Uber and Ola focusing on profitability, EVs will be top of mind. Uber’s electric mobility focus is a sign that they will double down on that strategy in India.

The two companies now have a full stack of logistics services, with cars, bikes, autos in place. Ola has even backward integrated to create 2 wheelers, perhaps an even more lucrative business than ridesharing.

But ridesharing has created a new way of life for Indians, especially those in urban areas. They need to fix quality and economics. Electric vehicles will likely be the way to go.

For an industry that has seen massive ups and downs in the last 15 years, this is the latest turn in a story that chronicles India’s rise.

EVs could be the ones to energize the industry as it recovers from the pandemic’s blow.

Writing: Chetan, Rajiv, Shreyans, Tanish and Aviral Design: Omkar and Chandra