What do NH7 (an annual music and comedy festival), comic con (one of India’s biggest pop-culture conventions) and Kofluence (a matchmaking platform for brands and influencers) have in common?

They’re just a few of the many acquisitions and investments undertaken by Nazara Technologies during the past decade, in a play that transformed the company into a holding company of sorts, with offerings gaming and content spanning age groups and geographies.

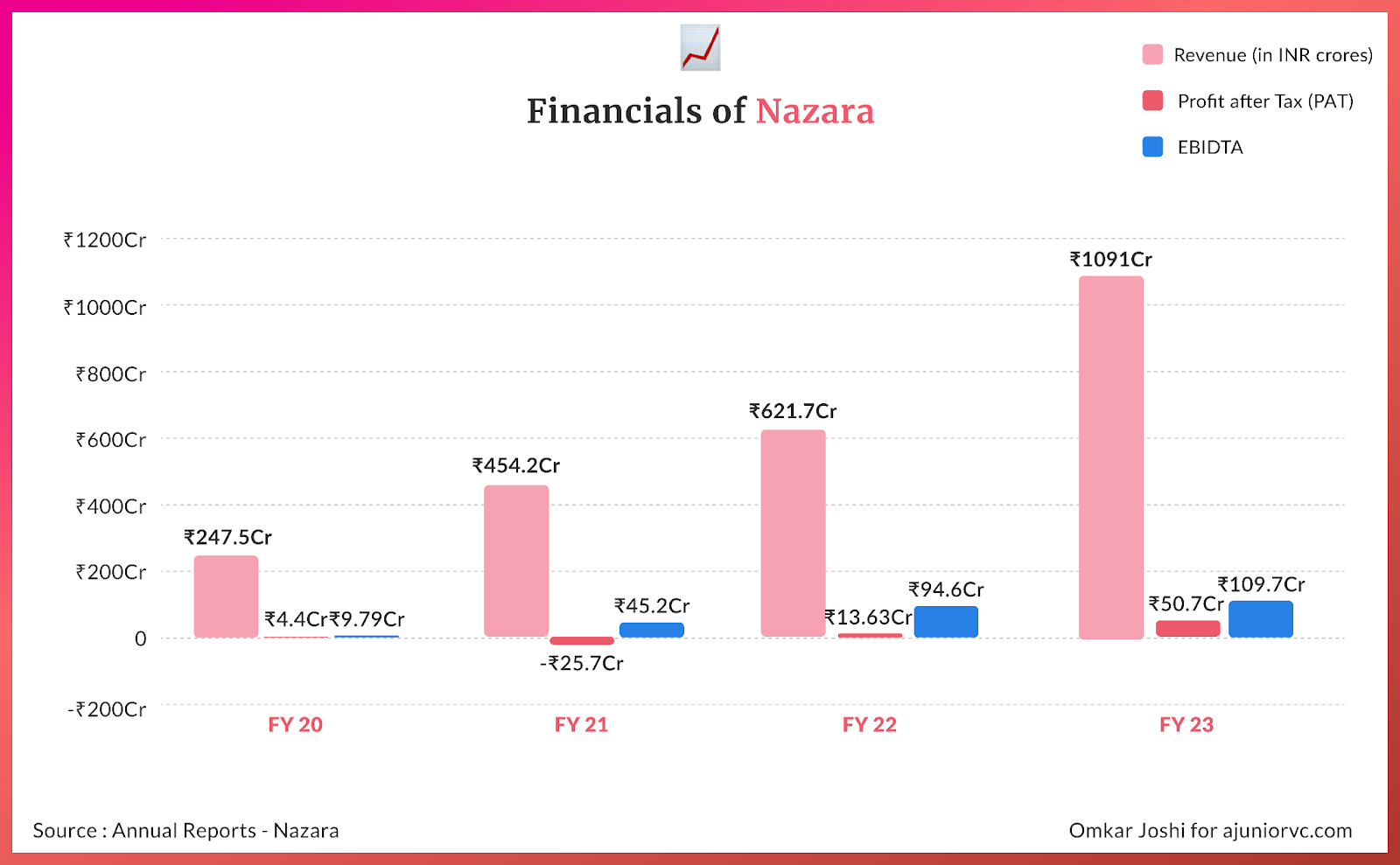

The upshot of this play? It took Nazara 20 years to reach annual revenues of ~INR 250 Cr, with a meagre EBIDTA margin of less than 4%. It took just three more years for Nazara’s revenue to grow ~5x, and EBITDA ~11x.

But Nazara wants to do more than just buy revenues. By identifying and unraveling the potential synergies that exists between its web of companies, it wants to transform itself into a full-fledged gaming platform. Let’s take a ride.

From Playing to Paying

Nazara Technologies’ story starts in 1999. Nitish Mittersain, then a commerce graduate from Mumbai’s Sydenham College, decided to turn his childhood passion for gaming into a business venture. ‘Nazara.com’, a gaming website, was born. And things scaled up fast; funds were raised from angel investors (including Nitish’s father), and a team of 60 was hired.

But the dotcom crash 2000 stopped Nazara.com’s monetisation potential form being realised. With debts of over INR 3 crore, Nazara sold its computers to pay its employees, and pivoted; it started dabbling in small ventures, like selling bulk SMS packs, to sustain its operations.

Four years would pass before the advent of feature phones in India would encourage Nazara to give gaming another shot. It pivoted again by launching a mobile cricket game, onboarding Sachine Tendulkar as its brand ambassador, and signing a deal with Airtel to sell its game as a value-added service (VAS). With VAS, Nazara hit paydirt – by 2013, it was earning INR 100 Cr in revenues.

But nothing lasts forever: the popularity of smartphones, exploding internet penetration rates, the multitude of free-to-play games on appstores was making VAS gaming a sunset industry by the middle of the previous decade. The launch of Jio in 2016, whose voice and data plans did not allow for VAS pay-per-use models, was the final blow.

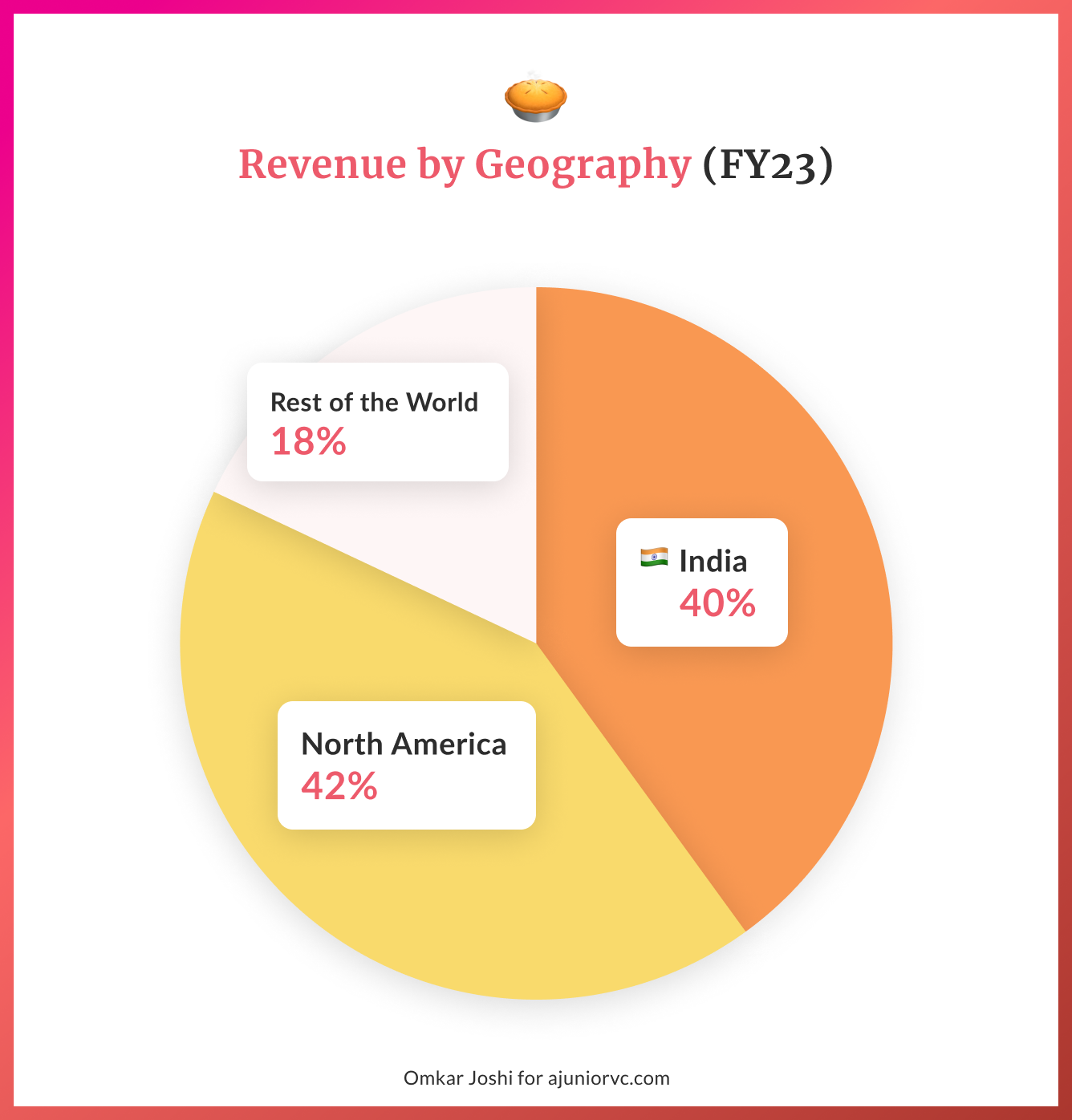

Nazara had to pivot yet again. So, it pivoted its DNA; it diversified and then diversified some more. A spate of 10+ acquisitions yielded a web of companies spanning three verticals – gaming, esports and ad tech, with 60% of its revenue base outside India.

Let’s take a look at how these verticals are faring.

Gaming: Healthy Margins Amidst Sluggish Growth Prospects

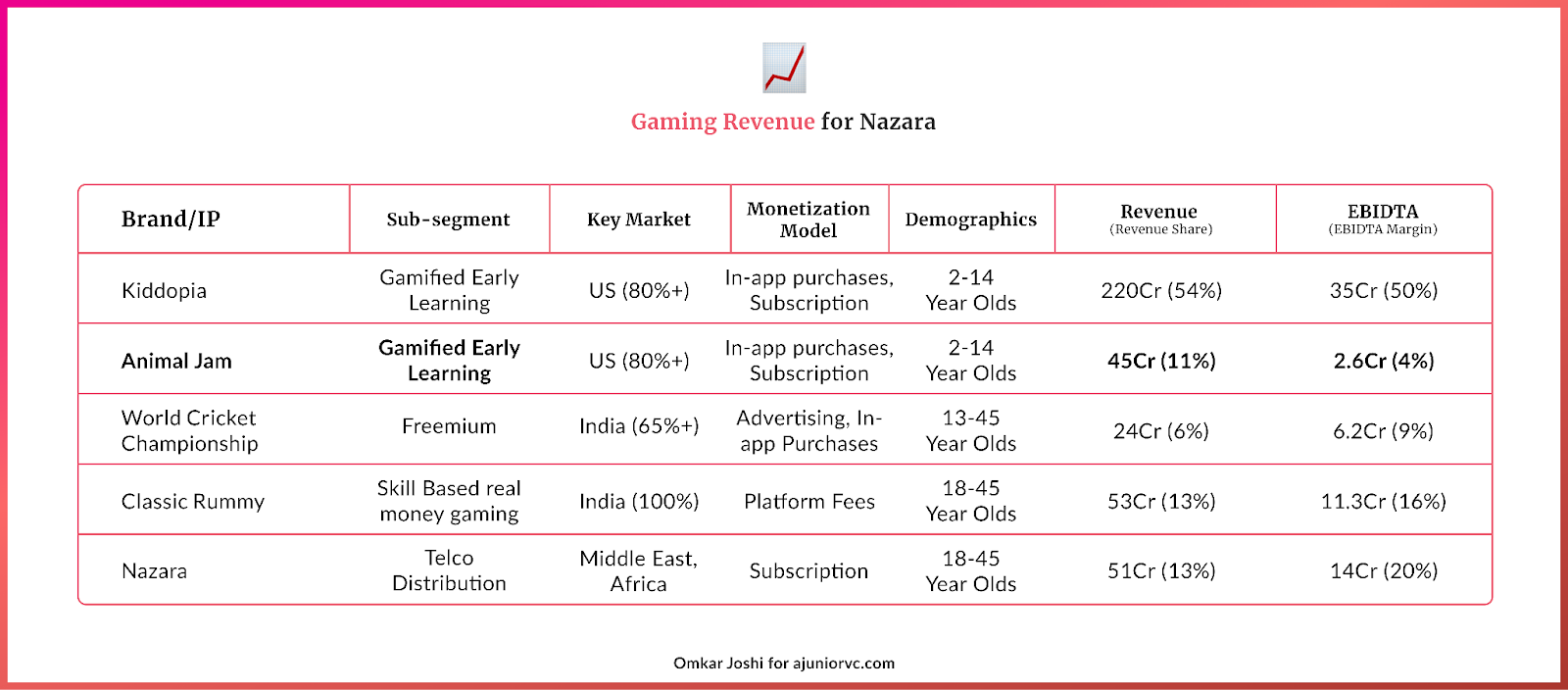

Over the years, Nazara has built a gaming portfolio that targets multiple age groups and spans multiple geographies. Accounting for 37 per cent of its revenue and an outsized 56 percent of its bottom line, gaming has long been Nazara’s cash cow.

And on the face of it, the vertical’s growth prospects look good. Gaming’s revenue grew by ~28 percent in FY 23.

But remove the revenue addition derived from Nazara’s latest acquisition – Animal Jam – and organic growth whittles down considerably to ~11 percent. Let’s disaggregate this further.

Of the ~INR 36 Cr added in organic gaming revenue in FY 23, the biggest contributor was Kiddopia (~INR 16 Cr), a subscription-based gamified-learning product targeted towards the US market. Kiddopia alone accounts for over half of the gaming vertical’s revenue and EBITDA and a whopping one-third of Nazara’s overall EBIDTA.

But a deeper look at Kiddopia’s numbers show that its revenue growth was a function of increased subscription price, rather than subscriber growth. Kiddopia’s subscribers have degrown, from a peak of ~340,000 in 2020, to ~310,000 in FY 2023.

Nazara’s next biggest driver of revenue growth, albeit unintentional, has been Classic Rummy – its only venture into the real money gaming (RMG) sector in India. In India, RMG is a ~USD 3 billion industry, and constitutes 60-80 percent of online gaming market.

But for Nazara, RMG constitutes barely ~5 percent of its overall revenue stream. And for good reason – given the regulatory flux surrounding RMG over the past few years, Nazara made a conscious call not to prioritize Classic Rummy in its portfolio.

However, the frenzy around RMG still fed into Nazara’s growth, with Classic Rummy adding ~INR 13 CR in incremental gaming revenues in FY 2023. Monetization became even more lucrative, with EBITDA growing 79 percent YoY.

But just when it looked like Nazara may have been over-cautious in its approach to RMG, the GST council imposed a 28 percent tax on the full value of bets placed on RMG platforms (note: not the winnings), throwing the industry into disarray and crippling it saga of breakneck growth. Dream11, the biggest RMG platform, has already faced an INR 55,000 Cr tax demand from the authorities.

Together, Kiddopia and Classic Rummy constituted 67% of Nazara’s gaming revenue, and an outsized ~80% of gaming’s incremental revenue in FY 23; today, both are facing considerable headwinds for future growth.

Even its other gaming ventures are not faring well. Telecom VAS, a legacy of its previous business avatar, is still the third largest contributor to gaming revenues, but has degrown by ~18 percent YoY.

Despite being the world’s largest cricket simulation game, World Cricket Championship (WCC) accounts for a meager ~6 percent of gaming revenue. It has grown by an average of just 10 percent over the last two years. WCC is stuck in a trap faced by the wider casual gaming industry (excluding RMG) in India – the country’s massive scale for user growth is undercut by an inability to effectively monetize said users.

In-app purchases, a function of disposable incomes, are usually inhibited. Advertising revenue, measured in cost-per-thousand impressions are significantly lower vis-à-vis other countries.

Nazara has a lot of work to do if it wants gaming to continue being its cash cow. But none of these challenges is unsurmountable – and Nazara is a business that has repeatedly shown a knack for pivoting and making the best out of bad situations. A lot of solutions are already in play.

For Kiddopia, Nazara is looking to tap institutional sales through school networks, enter new geographies, and unlocking additional monetization channels such as advertisement and merchandising.

For RMG, Nazara seems to have taken famed investor’s Warren Buffet’s maxim, “Be Fearful When Others Are Greedy and Greedy When Others Are Fearful” at heart. With cash reserves of over INR 13,000 Cr, Nazara perceives the industry downturn as an opportunity to hunt for dirt-cheap acquisition targets to strengthen its position in the segment.

And for WCC, that’s where Nazara hopes its efforts of building a gaming platform will pan out. Read on to find out how.

Esports: Nazara’s Next Engine of Growth

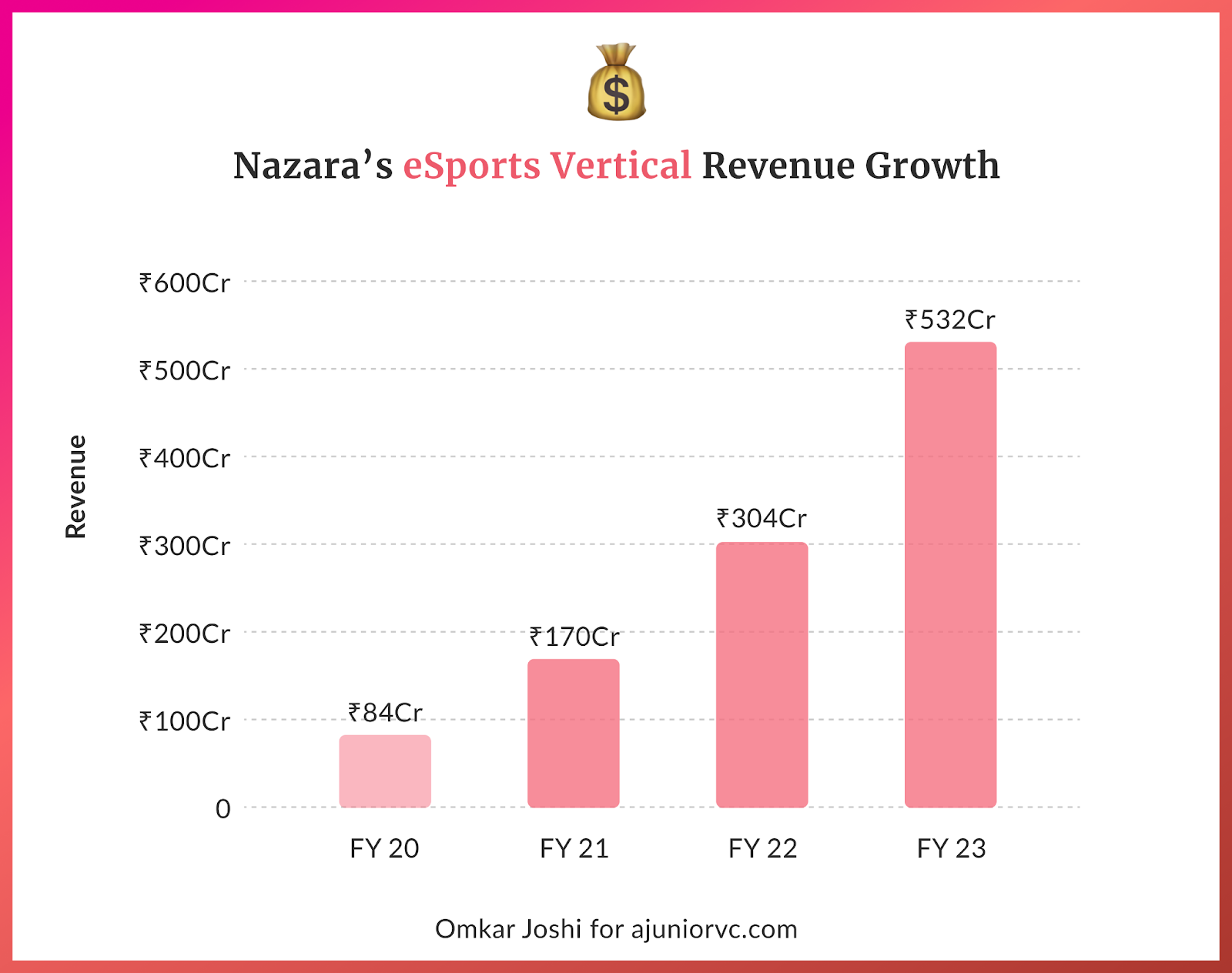

Over the past three years, Nazara’s esports vertical has enjoyed a spectacular 85 precent compounded annual growth, displacing gaming as Nazara’s largest vertical by revenue in 2023. But before we dive into decoding the key drivers behind this growth, let’s take a step back and understand what esports is all about.

Traditionally, esports are defined as video games played in organized competitive environments, often with a physical or virtual spectator base – not that different from actual sports. Nazara defines esports differently- as businesses built on top of games.

Which is why Nazara has two distinct segments driving its esports vertical.

The first is NODWIN gaming, which fits the traditional model of esports. NODWIN organizes gaming tournaments (120+ including popular games like PUBG/ Battlegrounds India), leverages them to produce content, and sells the media rights to various broadcasters (including Star Sports, Disney Hotstar, Jio TV etc.). In addition to media rights, its revenue drivers include sponsorships and advertisements and revenue from game publishers who partner with NODWIN to develop gaming tournaments.

With NODWIN having an 80 percent market share in esports in India, Nazara has established a undisputed market leadership position in this nascent, yet fast-growing industry. There are approximately 350 million gamers in India, but most of them are casual gamers – eports players and viewers account for less than 5 percent of the current market. This represents a high level of under-penetration vis-à-vis global levels (~ 25 percent), indicating a strong growth potential in the future. The esports market in India is expected to outpace global markets on the back of 25 percent annual growth over the next decade.

Further, roughly around 1/5th of gamers in India invest in gaming, with about 115 million gamers spending an average of US$ 13 annually. While this number is lower than the US$ 45 spent on real-money gaming (RMG), it’s important to recognise that it has doubled since the pandemic.

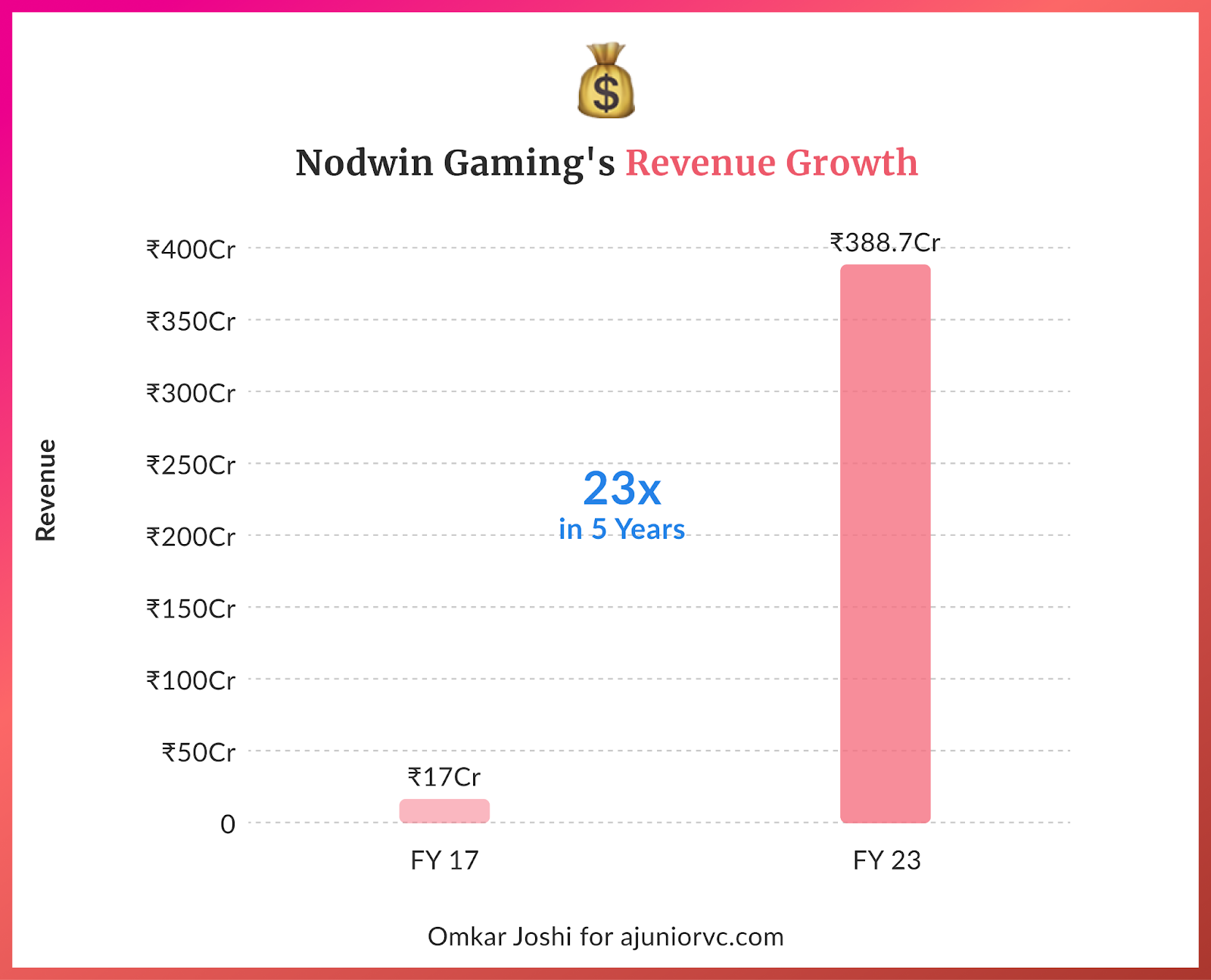

Consequently, NODWIN’s lucrative positioning in this high potential market has been leveraged by Nazara to drive a ~23x revenue growth in the last 5 years. While EBITDA margins remain miniscule (~2 percent), Nazara has defined NODWIN as a ‘strategic’ asset, focusing on consolidating their market leadership position and growing the nascent esports market in India rather than profitability. This explains the deviance between esports topline (~49 percent) and bottom-line (~33 percent) contribution to Nazara’s financials.

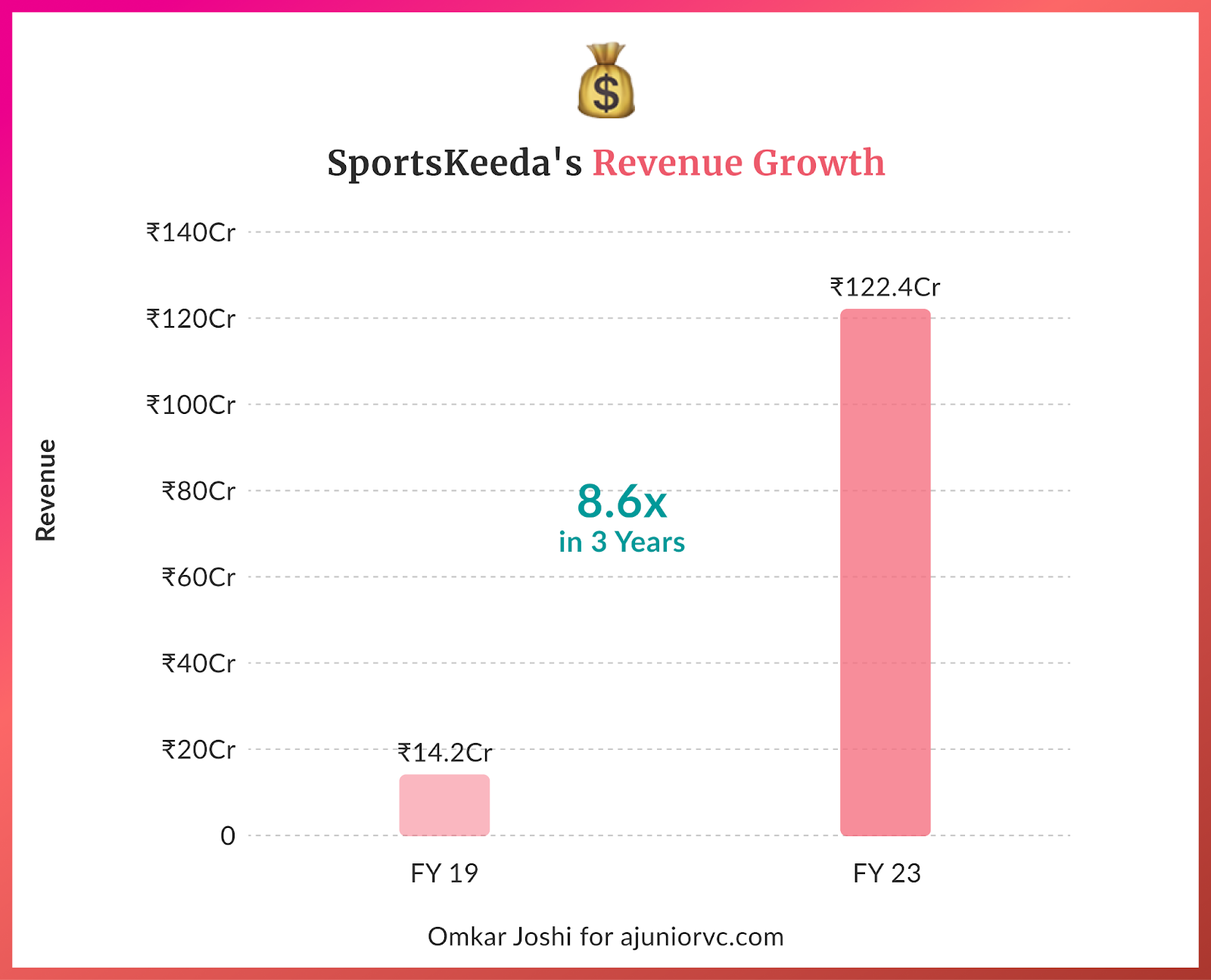

The second segment of its Nazara’s esports portfolio is SportsKeeda, a sport and esports news website that has clocked a ~9x increase in revenue in the past three years, driven by a large audience in the US (contributing ~50 percent revenue share, and reportage of events including WWE, soccer, cricket, basketball and various esports tournaments. Sportskeeda also enjoys an extremely healthy EBITDA margin of 32 percent.

Alright, lets stop here for a quick summary. Gaming is Nazara’s current cash cow, but is facing challenges – albeit not unsurmountable. On the other hand, esports is emerging as Nodwin’s crown jewel, on the back of its dominant positioning in a nascent, fast-growing market.

But till now, Nazara looks like an unassembled puzzle of disparate businesses struggling to fit together. Or does it?

Of Synergies and Platforms

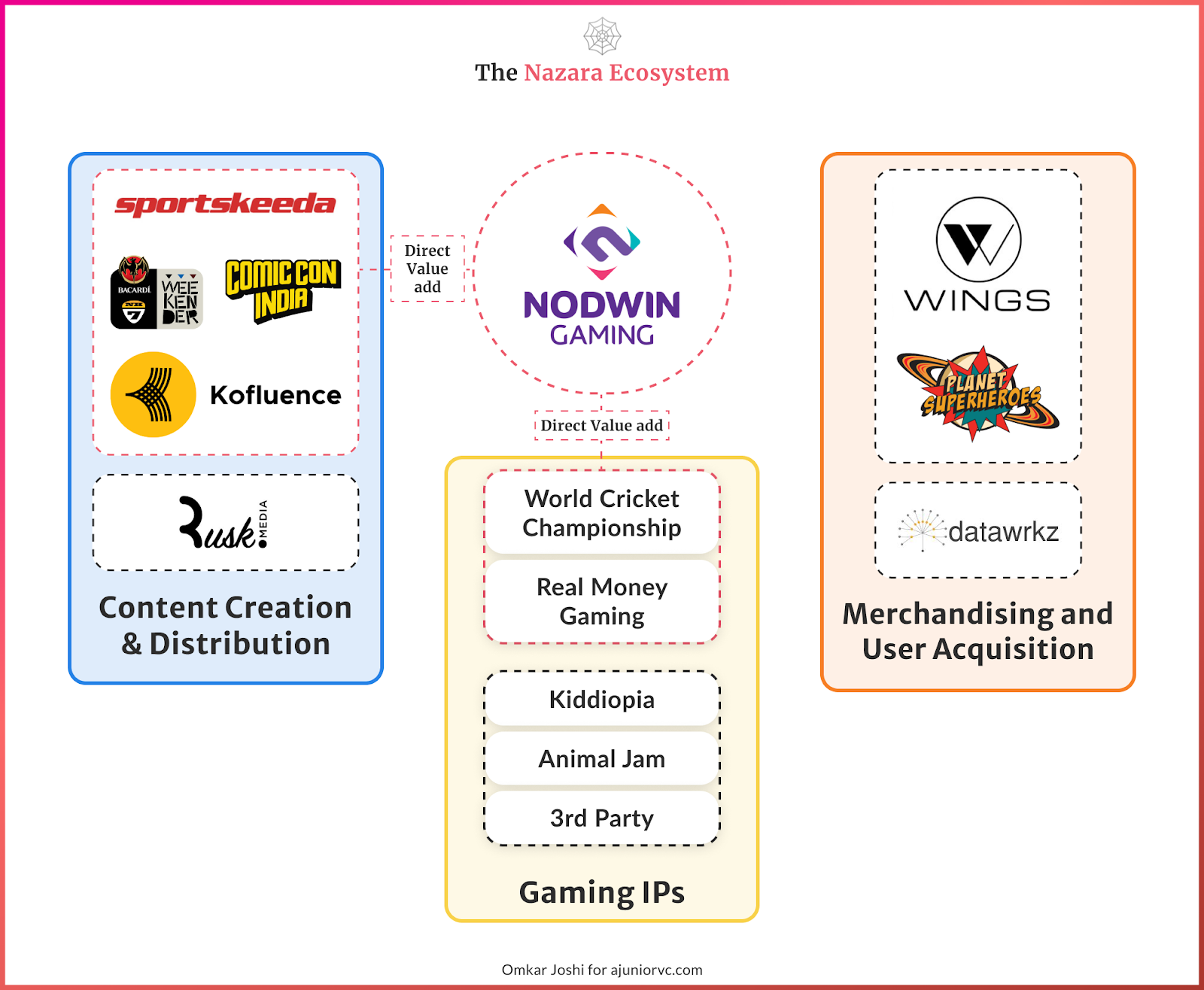

To understand how these pieces connect with each other, let’s take another look at question we asked at the very beginning – what do NH7 Weekender, Comic Con and Kofluence have to do with each other?

Simply put, content distribution. While NH7 gathers lovers of music and comedy, Comic Con brings together lovers of comics and pop culture. Kofluence is a platform for the masters of short-form content – social media influencers. And that’s not all. Nazara has also acquired a 10 percent stake in Rusk Distribution – a maker of youth-focused OTT shows.

Through Sportskeeda, NH7 Weekender, Comic Con, Kofluence and Rusk, Nazara gets access to mainstream consumers of sports, music, comedy, short-form and OTT content. Nazara is going to leverage them all to flood the market with yet another form of content, which till now has been restricted as a relatively niche subculture – you guessed it – gaming. To streamline its efforts, it even acquired a specialized games marketing agency – PublishMe.

Through this content powerhouse, Nazara hopes to drive user acquisition for its gaming labels as well as NODWIN tournaments, while simultaneously unlocking drivers of advertisement and sponsorship revenue. Once users of its gaming properties cross a required threshold, NODWIN can work on.

And its efforts will be supported by Datawrkz – yet another Nazara acquisition – that specialization in tech and data driven user acquisition and monetization growth.

Not only does it come with an established external client base that generated a revenue of cool ~150 Cr in FY 23, but its capabilities are also being turned inward to improve user and monetisation metrics across Nazara’s gaming properties.

And that’s not all. Nazara is already establishing footholds in allied services through the acquisition of Wings, a producer of gaming audio equipment, and Planet Superheroes – a retailer of pop-culture merchandising.

So on one hand, you have Nazara’s set of gaming properties – which is are set to expand considerably given its decision to launch up to 20 games across mobile, web3, virtual reality (VR) and personal computer (PC). On the other, mix of diverse content distribution channels, supported by acquired expertise in marketing and monetization.

And there you have it – a full-fledged ecosystem aimed at elevating the gaming subculture into the mainstream in India, with Nazara positioned to ride the wave till the very top.

Writing: Shreyas Vatsayan, Tanish Girotra ; Design: Omkar Joshi