A recent exchange on Twitter between Deepinder Goyal, co-founder of Zomato, and the company’s official Twitter account, generated some confusion regarding the correct pronunciation of the company’s name. While a poll with over 150,000 responses settled the matter in favour of ‘ZoMaato’, it was interesting to observe that almost 35 percent preferred ‘ZoMaito’.

In Zomato’s latest quarterly report (Q4 FY23), Deepinder addressed the question again by stating “It doesn’t matter. They both deliver on time (including profits)”. Deepinder may not face much debate for claiming that Zomato delivers on time. The second half of his claim, however, needs some looking into.

Fascinatingly, Zomato ended up delivering a consolidated profit of INR 20 Mn in its next quarter (Q1 FY24). Although this represents an infinitesimal 0.0008 per cent of its revenues, optimism around the company’s prospects led to a sharp uptick in its stock price.

It is worth acknowledging that this figure arose out of an accounting anomaly – a negative deferred tax entry of INR 170 Mn. Skeptics, therefore, dismissed the excitement around this development as unwarranted hype.

However, to do so would be to ignore the possible beginnings of a path towards profitability. Let’s dive in.

The Zomatoverse

Zomato’s beginnings can be traced back to 2008, when Deepinder, then working at Bain & Co., would have to regularly queue up with his colleagues at the office pantry to see food menus during lunchtime. This is where Deepinder first identified a problem that needs to be solved. Along with his cofounder Pankaj Chaddah, Deepinder started a website called FoodieBay, which had menus of around 1,400 restaurants in Delhi.

Over the next few years, Foodiebay, which eventually came to be called Zomato, developed an application and expanded its operations beyond the borders of Delhi. By 2012, Zomato had a presence in over 35 cities in India and 11 countries. Subsequently, in 2015 Zomato launched its last-mile food delivery vertical.

In 2018, it entered the B2B delivery space by launching Hyperpure, a farm-to-fork platform, and also achieved unicorn status. Adding on to its organic growth, Zomato has also acquired 16 companies, with the latest being the quick commerce platform Blinkit (erstwhile Grofers), in 2022.

In 2021, Zomato opted for an IPO, with the stock price initially listing at a premium of over 50 percent. The hype around the listing revolved around Zomato’s food delivery business operating in an effective duopoly. Multiple other startups in the space have failed and shut down in the past few years, leaving only Zomato and Swiggy in the fray.

However, the public markets work differently than private ones – growth at the cost of profits is not desirable. Zomato’s share price fell from a high of INR 154 in November 2021 to a low of INR 46.80 in July 2022. It has since recovered significantly to INR 89 as of mid-August 2023 on the back of topline growth, a recent declaration of quarterly profit, and a potential path to long-term profitability.

The numbers underlying the above narrative paint an intriguing picture.

Path to Profitability?

Deconstructing Zomato’s financials has some unique challenges, with the foremost amongst them being Zomato’s affinity towards using ‘Adjusted’ figures, specifically for its revenue and EBITDA numbers.

From FY 2019 to FY 2023, Zomato’s operational revenue has increased sixfold from INR 11.62 Bn to INR 70.75 Bn – representing a whopping CAGR of 44 percent. That’s impressive growth. The next step, ideally, would be to look at the Zomato’s EBITDA trend. However, Zomato’s EBITDA precludes the cost of share-based payment expenses to arrive at Adjusted EBITDA, something which has been the object of criticism, and even memes.

That being said, its Adjusted EBITDA has shown significant improvement, and has reduced from a negative INR 21.4 Bn to a negative INR 7.83 Bn. When compared against revenue, this represents an improvement in Adjusted EBITDA margin of -184 percent to -11 percent in these five years.

Net loss, however, has failed to show a significant positive trend. To better understand why, let us break down the revenue and cost headers for FY23.

As seen in the chart below, around 64 per cent of its revenue is attributed to food delivery, with Hyperpure, Quick Commerce, and Other Segments (residual) accounting for around 21 percent, 11 percent, and 3 percent respectively. Other Segments (residual) primarily consist of advertisement revenue and membership/ subscription-based revenue. The distribution of attributable losses, however, shows a very different story.

Despite the Quick Commerce segment’s contribution of only 11 per cent towards Zomato’s revenue, it accounts for an outsized ~50 percent of Zomato’s losses of ~INR 10 Bn. Meanwhile, the food delivery segment’s losses, standing at INR 44 Mn, account for a minuscule 0.43 per cent of the total. In FY22, food delivery’s losses stood at INR 7.65 Bn. The overall numbers thus hide a tale of a massive improvement.

It stands to reason that Zomato’s lacklustre performance in its overall path towards profitability for FY23 is primarily due to its acquisition of the heavily loss-making Blinkit, whose operations now constitute the Quick commerce segment. But, as we shall soon see, Zomato has already made significant strides to better the Quick Commerce segment’s unit economics in less than one year.

Now, let us get down to the source of the current excitement around Zomato – its latest quarterly numbers. Note that the Q1 FY24 report deals only in Adjusted Revenue figures, which include ‘customer delivery charges’. Zomato’s annual reports indicate that customer delivery charges are directly passed on to delivery partners, and are not included in the profit & loss statements in its annual report filings. As such, we arrived at actual revenue figures by netting the customer delivery charges for that quarter.

Operational quarterly revenue saw impressive year-on-year growth of ~71 percent in Q1 FY24.

Further, to discount the effect of deferred taxes, let us only consider losses before taxes – while the numbers did not show any improvement throughout FY23, losses reduced by a drastic ~92 per cent from INR 2.06 billion to INR 150 million.

There is a simple explanation for this. From Q4 FY23 to Q1 FY24, while operating revenues increased by 17.5 per cent, overall expenses grew only by 7 per cent. Simple, but not easy to execute. While further cost optimization is required for Zomato to start showing serious profits, the trajectory they seem to be on paints a hopeful picture.

Zomato fares quite well not only against its own past, but also its closest competitor, Swiggy. As the chart below shows, in FY23, Zomato earned slightly higher total revenues (including other income) than Swiggy, while limiting its losses to around one-fourth of the latter’s.

Let’s dive a little (actually, a lot) deeper by looking at each of Zomato’s business segments in isolation. Hang on.

Food Delivery

Online Food Delivery, Zomato’s biggest revenue generator, operates in a market currently pegged at USD 7 bn (INR 574 Bn) in gross merchandise value terms and is considered an effective duopoly, with Zomato & Swiggy constantly battling it out for marginal gains in market share. Here too, Zomato has gained a slight edge over the past couple of years.

This USD 7 Bn (INR 574 Bn) figure indicates a high level of under-penetration, given that the overall food industry (inclusive of food services & home cooked food) is valued at around USD 670 Bn (INR 54,940 Bn), of which food services constitute a paltry USD 65 Bn (INR 5,330 Bn). With rising incomes, growth in an aspirational middle class, and fast-paced urbanization, online food delivery as a proportion of food services, food services as a proportion of the food industry, and the food industry itself is expected to experience considerable expansion.

Indeed, Bain & Co. expects the online food delivery market to grow threefold to reach a market size of USD 22 Bn (INR 1,804 Bn) by 2027 itself. Underlying these numbers is the fact that annual online food delivery users (~55mn) currently account for only 8 percent of India’s total internet users (~750 Mn), with the latter expected to grow to ~900mn. A more precise benchmark would perhaps be the online shopper base in India, which currently stands at 190 Mn, and is expected to grow to 540 Mn by 2027. Whichever way you see it, the opportunity is huge.

Unfortunately, huge opportunities do not always translate to huge profits. The tombstones of Foodpanda, Amazon Food, Uber Eats (acquired by Zomato), and many more can attest to that.

So how did Zomato reduce this segment’s losses from a whopping INR 7.65 Bn to INR 44 Mn in FY23? Note that here, segment results are not inclusive of other income, share-based payment expenses, finance costs, depreciation, and amortization expenses – all of which are incorporated after combining all segment results, to finally arrive at overall profit/ losses.

Moreover, as seen in the chart below, the latest quarterly numbers paint an even better picture.

Note that as before, we have arrived at actual revenue figures to paint a more realistic picture of Zomato’s financials. Unfortunately, we will have to make do with Adjusted EBITDA numbers, as Zomato does not attribute share-based payment expenses to specific segments.

While operational revenues grew by ~18 percent year-on-year growth, Adjusted EBITDA turned positive in the previous four quarters. What’s key here is that Adjusted EBITDA is rising at a faster rate than revenue. In Q1 FY24, Adjusted EBITDA amounts to a healthy 10.6 per cent of Adjusted Revenue, and 13.2 per cent of actual revenues. One year ago, it stood at a negative 10.5 per cent of actual revenues.

The modus operandi behind this improvement was broken down quite effectively in Zomato’s Q4 FY23 report, which has been reproduced below. The chart details how the contribution per order has increased just shy of three-fold in the past one year, through improvements across all per unit revenue and cost components, except customer delivery charges and delivery costs.

This segment’s muted topline growth in FY23 seems to be a function of two levers – a focus on the bottom line, and muffled demand forces in the economy. Underlying Zomato’s shift of priorities towards profits is the fact that Zomato chose to shut down its operations in 225 cities. Parallelly, it also strategically churned out unprofitable customers by orienting marketing spends towards a higher quality of customer and limited support options for customers categorized as ‘abusive’.

There is considerable scope for further optimization in this regard – the top 8 cities in Zomato’s 1,000+ locations contribute more than half of its gross ordered value, and only 2.3 Mn customers, out of 50 Mn+ annual transacting customers, order more around 5 times a month.

The duopolistic nature of this market and the lack of any upstart disruptors could provide both Swiggy and Zomato a haven to shift plays towards profits rather than having to defend their respective market shares. Indeed, it is an interesting coincidence that Swiggy’s food delivery business also turned profitable in March of this year. Given its plans for an IPO next year in connection with the available precedent of Zomato’s listing experience, it is conceivable that Swiggy too will opt to prioritize profits over growth in the near future.

Prioritizing the bottom line does not implicate a complete negation of topline growth. Despite the focus on the bottom line, there is a noticeable uptick of ~17 per cent quarter-on-quarter in the topline numbers for Q1 FY24 – a sign of short-term recovery in demand. The simultaneous improvement in margins suggests that generating profits, coupled with sustainable (as opposed to breakneck) growth may not be exclusive goals for Zomato.

In the long term, a promising horizon could emerge. If the food delivery market does reach the expected market size of INR 1,806 Bn (in terms of gross order value) by 2027, assuming a continuation of the current duopolistic nature would peg the GOV passing through Zomato at around INR 900 Bn. As of Q1 FY24, Adjusted EBITDA for this segment is at 2.5 percent of its GOV, which means Adjusted EBITDA could increase to around INR 22.5 Bn in the next four years, if the margins are maintained. Zomato aims to bring these margins up around 4- 5 per cent of GOV as the business matures, which could double the expected EBITDA eventually (hopefully not Adjusted by then).

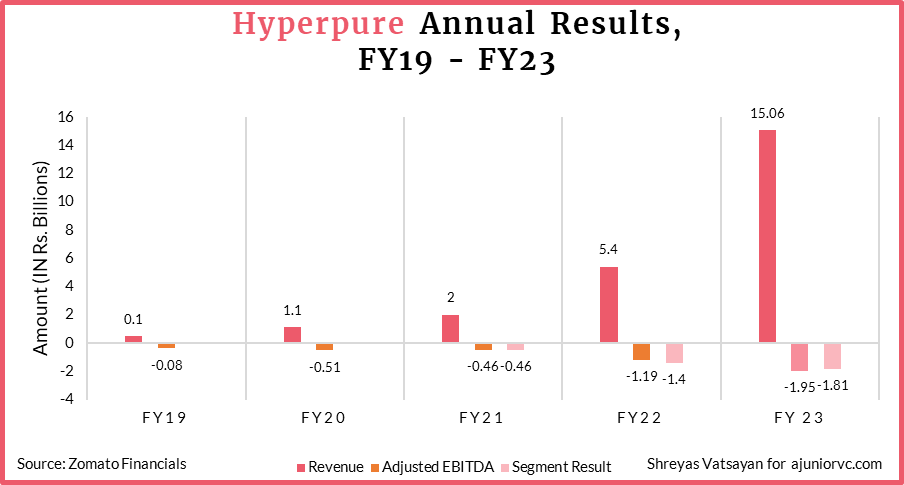

Hyperpure

Launched in 2018, Hyperpure is a purely B2B, farm-to-fork food service that also seeks to tap into the USD 65 Bn (INR 5,330 Bn) food service industry – from a different direction. Restaurants usually spend around ~40 percent of their revenues on grocery acquisition, resulting in a total addressable market of USD 26 Bn (INR 2,132 Bn).

In what could be considered a form of vertical integration, Zomato hopes to use its wide distribution of restaurant partners and developed expertise in food delivery logistics to gain an edge over the existing competition in this space.

The competition here is of a different nature than in the food delivery market. Historically, the supply of raw materials to restaurants was mostly dominated by unorganized, local players – which have accounted for over 91 percent of grocery procurement by restaurants. However, the space has seen an influx of agritech startups, with Tracxn categorizing 600+ companies as providing B2B farm produce e-commerce services, including the likes of WayCool and Ninjacart.

After spending three years developing infrastructure & supply chains in 10 cities across India, Hyperpure experienced explosive growth in its revenues over the past two financial years – from INR 2 Bn in FY21 to INR 15.06 Bn in FY23, representing a CAGR of 96 per cent. This has been on the back of the fast-paced onboarding of partner restaurants – which grew 40 per cent in FY23 to reach 72,000 – in what seems to be a demonstration of an effective cross-selling strategy adopted by Zomato.

Of note is the fact that over the past five quarters, Adjusted EBITDA margin as a percentage of revenue has reduced from a negative 16 per cent to a negative 6 per cent, while revenue has increased by an average of ~20 percent quarter on quarter. While profitability seems to be a distant goal for Hyperpure, continued efforts toward maintaining the current trajectory of heavy growth with improving margins would make it an accessible one.

Over 75 percent of Hyperpure’s revenue is sourced from medium-sized restaurant chains and retailers, with the remaining 25 percent being sourced from larger chains, indicating a heavy reliance on the organized portion of the food service space.

Rakesh Ranjan, Hyperpure’s CEO, considers their current inroads to have accounted for only 1-3 percent of the total opportunities available in the 10 cities where Hyperpure is currently operational. Given the massive, expected room for growth in existing geographies, Zomato is unlikely to expand its offerings to other smaller cities in the near future.

Another factor that plays into this decision is the exceedingly low-margin nature of an essentially trading-based business. As such, recovering fixed costs in smaller cities would be highly challenging. Demand density would play a big role in turning Hyperpure’s operations EBITDA positive. Continuing to focus on profitability, Zomato shut down its Hyperpure operations in Chandigarh, at the end of FY23 due to lower-than-expected demand density.

Exploring its options in the future, Zomato may build different operational models for smaller cities – routing products directly without warehouses, or hub-and-spoke models with large warehouses in major cities servicing smaller satellite cities around it. Further, integrating some parts of its infrastructure and operations with the quick commerce vertical, if feasible, could lead to a further reduction in costs across the board in the future.

Quick Commerce

Zomato’s acquisition of Blinkit in FY23 was a controversial one. For one, Albinder Dhindsa, the co-founder of Blinkit, previously held the position of Zomato’s head of international operations from 2011 till 2014. Second, he is married to Akriti Chopra, the current chief people officer of Zomato.

As such, concerns were raised about whether the deal was conducted at an arm’s length. In response, Zomato asserted that an independent valuation of the transaction had been conducted by EY, which was further supported by an independent fairness opinion from Morgan Stanley. It also noted that an independent opinion was taken by Saraf & Partners to ascertain that Albinder and Akriti’s relationship did not constitute any violation of related party transaction regulations.

The opportunity is a highly attractive one. Recall the USD 670 Bn (INR 54,940 Bn) food market size, of which around 10 percent, or USD 65 Bn (INR 5,330 Bn) was part of the food services industry. It stands to reason that the remaining 90 percent, around ~ USD 600 Bn (INR 49,200 Bn), consists mostly of groceries purchased by households for home-cooked meals. Of this, 95 percent is part of the unorganized sector. Of the remaining ~USD 30 Bn (INR 2,460 Bn) in the organized sector, only around USD 5 Bn (INR 410 Bn) is attributable to ‘delivered groceries’, of which quick commerce currently forms a minuscule share.

A large market is up for grabs, waiting for the right business model. And the companies in the fray to do so are many, disruptors (Zepto, Big Basket, Swiggy) and behemoths (JioMart) alike.

Regardless of said criticisms, Blinkit’s operations have seen considerable improvement under the aegis of Zomato’s management, in a limited span of three quarters. Blinkit’s application will continue to operate independently, while the delivery fleet at the back end is being integrated across Zomato’s other verticals as well for cost efficiency.

While considerable topline growth was seen throughout FY23, Q1 FY24 saw a muted increase, combined with a decrease in number of orders. One of the primary reasons behind this dip was a strike called by the erstwhile delivery partners of Blinkit, who were protesting against new payout structures rolled by Zomato’s management post the former’s acquisition. The disruptions ended after a period of about 45 days, albeit on unclear terms.

In yet another sign of Zomato’s focus on profitability, Adjusted EBITDA margins as a percentage of revenue declined from a negative 200 per cent to just a negative 35 per cent.

The below chart, replicated from Zomato’s Q4 FY23 report, breaks down the drivers behind the massive improvement in per unit contribution, representing growth of ~84 percent in less than one year. One of the key drivers behind this growth was the increase in per dark store throughput, with the average gross order value per store per day doubling from INR 309,000 to INR 625,000 between Q1-Q4 FY23. This was achieved by focusing on fast-moving SKUs, optimization of store design, and replenishment cycles for products.

Zomato has made decent strides towards improving its unit profitability without taking off the pressure on growth. The huge untapped opportunity at play has attracted serious competition, some with deep pockets.

However, since 2022, the industry has shown signs of trouble, similar to the consolidation phase of the food delivery industry. In 2022, Ola Dash shut down its operations. In early 2023, JioMart closed its express grocery delivery service, while retaining its normal online delivery service. More recently, Dunzo has laid off over 30 percent of its workforce over the last few months.

Zomato will have to carefully balance revenue and market share capture while defending its margins to survive this wave of consolidation, to come out at the top.

Dining Out & Others

After reaching a peak of INR 6.6 Bn in revenue in FY20, dining-out and membership-based revenues have fallen each year to reach a low of INR 2.34 Bn in FY23. The fall was on the back of shutting down of related international operations, COVID-related lockdowns, and multiple closures and re-launches of its membership programs. Erstwhile Zomato Pro members remained flat at 1.5 million from FY21 to FY22 and scaled to 1.8 million in Q4 FY23 under the newly launched Zomato Gold program, which replaced the Zomato Pro program as the fourth iteration of Zomato’s membership program.

But the real financial benefit of Zomato Gold, may not be the subscription revenue, but the high order frequency availed from such members. After purchasing a Gold subscription, users increase their order frequency by 60 percent on average. In March 2023, Gold subscribers accounted for 30 percent of Zomato’s total gross order value.

Despite this segment’s rather underwhelming performance, Zomato believes that its time has come. So much so, that income attributable to dining-out will no longer be reported under ‘Other’ income sources. Rather, it will be combined with its young events and ticketing vertical named ‘Zomato Live’, to form a new business segment called ‘Going out’, and will be reported as such in the next quarterly report.

This should be an interesting space to watch – a sudden uptick in the number of Gold members in the future could result in outsized positive impacts on Zomato’s top and bottom lines.

The Way Ahead

By now, a clear and common theme has emerged across all of Zomato’s main verticals – an increasing level of importance laid on unit economics. Zomato is slowly changing its identity from being a venture capital-funded disruptor chasing breakneck growth, to a publicly listed company trying to deliver profits to its shareholders.

While choosing profits over growth may be rewarded in the short term, given the low-margin nature of all three of Zomato’s business verticals, it will have to carefully balance scale and unit economics to make its shareholders happy in the long term.

Zomato is counting on strong macroeconomic growth, a large and growing aspirational middle class, and rising internet penetration levels to help achieve its growth. On the other hand, input inflation, the dominance of the unorganized sector in the food market, and deep-pocketed competitors will act as heavy headwinds.

But Zomato remains optimistic. Rumours strife about Zomato’s experiments to launch new verticals, including offering B2B logistics services for other e-commerce players, and offering home care services, similar to Urban Company. These plays could indicate a shift away from the past, wherein Zomato has focused solely on adding to its food services stack. However, these opportunities are unlikely to be converted in the near future, as Zomato’s current emphasis remains on improving unit economics.

Zomato’s financial evolution underscores a significant shift from sustained losses to a promising pathway to profitability. It has finally achieved positive unit economics in its core business of food delivery. Renewed focus on its dining-out business, along with its fast growing Hyperpure segment has yielded a strong foothold in the food service market segment. Its inorganic expansion into grocery delivery, tapping into the home cooked meals market, completes its four-pronged foray into the USD 670 Bn food market in India, and unlocks what could be its biggest driver of growth in the future.

Writing and Design: Shreyas