Last fortnight, Zomato reported quarterly results, with Blinkit breaching 2,000 Cr revenue on the back of a staggering 97% growth.

Foodie Beginnings

Albinder Dhindsa grew up in Patiala with parents who were predominantly engaged in farming.

His mother viewed education as an escape from the “sarson da khet” and the village life in which her kids would grow up. She ingrained in her kids that they needed to excel at academics if they wanted to get somewhere in life. Both the brothers took this advice to heart.

Albi’s elder brother cracked the civil services exam to become a public servant. Albinder cracked JEE, and went to IIT Delhi in 2000.

That era was when smartphones were yet to be launched, but mobile networks were being set up.

Within a year of his admission, the dot-com crash happened. The Indian job market had not recovered from this shock when he graduated in 2004. He went to the US for a Master’s degree, after which he started his professional career as a Transportation Analyst at URS Corporation. He moved on in 2007 to join Cambridge Systematics.

That is where his path collided with that of Saurabh Kumar. Saurabh had just completed his Master’s in Transportation Engineering from The University of Texas at Austin after graduating from IIT Bombay in 2006. They worked together until 2010 when Albinder went to Columbia for his MBA, and Saurabh joined Opera Solutions.

Their paths were destined to cross.

Around the same time, another IIT Delhi graduate started FoodieBay, which aimed to digitize restaurant menus. FoodieBay’s founder, Deepinder Goyal, called his NTSE cohort mate and college batchmate, Albinder, to join the early team.

Albi left his comfortable investment banking job at UBS and returned to India, where he bumped into Saurabh again.

They got to know each other better over the next two years of building Zomato together. Both recognised the massive opportunity that Indian retail had to offer. Saurabh took the plunge in November 2013 to start Grofers. Albi followed him within a few months.

Grofers was an amalgamation of the words grocery and “gophers,” which meant someone who runs errands.

True to the word, Grofers was started as a logistics company in the express delivery category, delivering purchases from local shops (such as Kirana stores, pharmacies, and bakeries) to customers’ doorstep in Delhi NCR.

Remember, this was in 2013.

Keep Calm and Deliver

Albi and Saurabh identified many pain points that plagued the convenience of their primary target audience – the office-goers.

In India, going to a mall is considered a pleasurable outing experience, however, going to a supermarket for daily purchases is viewed as a chore.

This target group did not have time on weekdays to stock up on essentials and did not want to do these chores on the weekends. They valued their convenience so much that they would jump at the idea of their weekly purchases being delivered to their doorstep.

The duo stumbled upon the insight that demand in the grocery segment outstripped supply. Consumers did not spend more because they did not have adequate supply and enough variety. If one could create supply, people would open their wallets.

Grofers aimed to increase the assortment of essentials available to their customers and the discoverability of these selections.

Grofers needed to build an elaborate delivery network and add a layer of merchant networks before abstracting the entire experience to a phone app.

They went out and hired delivery personnel on the Grofers payroll. This would end up delighting all parties on the platform.

By 2014, they would report to a local hub, before being routed to merchants to collect orders and deliver them to doorsteps. Grofers then approached the local merchants to tie up with them, with the premise of opening up a new distribution channel for them.

Merchants were happy because they no longer needed to deal with their own delivery boys, and their order volumes increased. Delivery personnel were delighted, too—they earned more than they ever did before and could set their working hours.

Consumers won as well—for the first time, they could peer into the entire inventory of all the merchants and micro-sellers in their 4-5 km radius locality. Discoverability was no longer a problem, and neither was delivery. Consumer intent about shopping was rapidly changing, and Grofers was poised to capture a huge chunk of their convenience spending.

Grofers’ traction grabbed the attention of their ex-employer, Deepinder. He, along with an institutional investor, invested in Grofers’ $500K seed round.

In Search of Scale

2015 would be a game-changer.

Having successfully proven their model in the NCR and Mumbai, Grofers had onboarded 250 merchants boasting a catalogue of 500,000 SKUs. They processed over 30,000 deliveries monthly, with a fifth placed through its mobile app.

As they drew up plans to go national, Grofers would receive their biggest vote of confidence yet, in the form of a $10M Series A fundraise.

Most small merchants had never sold online, so Grofers employees would have to take photos of products in the store and upload them to the platform, a hugely time-consuming process.

Their plan was to make it easier for merchants to manage orders and track inventory independently. The funding would be key to improving this inventory management system.

The following month, Grofers would announce the acquisition of My Green Box, a Bengaluru-based grocery delivery app, as it aimed to enter a new city and scale its grocery business, which accounted for 60% of all transactions by then.

Two birds in one basket.

Two months on from their fundraise, Grofers had already scaled to 400 merchants and had tripled the number of orders placed through the app. Users could also order through Twitter through the #TweetnShop hashtag and would receive their orders in under 90 minutes. They had comfortably set up shop in Bengaluru and had Hyderabad and Pune on their radar.

Grofers would soon close another $35M funding round from the same group of investors. The company was on fire.

This would be used mainly to increase their SKUs as they aimed to introduce new categories, enabling consumers to access an unmatched selection and convenience via online shopping.

By November, Grofers would be live in 26 cities across the country, and the app would cross 1.5M downloads. They would also complete the acqui-hire of B2B logistics provider Townrush and food delivery app SpoonJoy. Both companies, with deep expertise in the sector, would add much value to the Grofers talent pool.

As 2015 ended and the race for on-demand delivery in India heated up, Grofers received a mammoth $120M Series C funding as it sought to become the leader. One little-known IIT Delhi graduate Ashneer Grover would join the company.

Grofers’ gophers were flying, but turbulence was coming.

Come One, Come All

By 2016, the overall grocery industry in India had grown to $383B and was pegged to touch $1T by 2020.

The online grocery segment, on the other hand, was valued at a mere $100M but was expected to cross $20B in the same timeframe.

Two major drivers would contribute to this potential growth.

The first is the huge uptick in the country’s total Internet users. This number had almost doubled to 213M from 120M a year ago, due to rising smartphone penetration and falling mobile handset prices.

The second was a change in the habits of consumers in India. As customers got comfortable shopping online, they moved to new categories. This, combined with their increasingly busy lifestyle, led them to opt for the convenience of ordering groceries online.

As the online grocery market began to take shape, a huge flurry of action would occur in the sector.

BigBasket would expand its operations, targeting $1B in revenue by the end of FY 2017. E-commerce giants Flipkart and Snapdeal would add gourmet and speciality food.

Having committed a $2B investment in the country a year ago, Amazon will follow through by introducing its gourmet food store on its platform. They will also launch Kirana Now, an express delivery platform in partnership with neighbourhood stores.

It would function similarly to startups in this space. The Kiranas would upload their catalogues online and list themselves as sellers, with Amazon providing the technology.

The competition heating up would lead to Grofers having to re-evaluate their strategy.

They would shut down operations in 9 cities across the country. The decision would result from these cities having seen minimal traction and the company’s decision to focus on regions where they had seen more significant growth.

They had expanded too fast, having raised too fast.

Grofers would hire Mumbai-based last-mile logistics provider Grab a Grub to optimise its fleet and improve its delivery times.

As the year would close, Grofers would do only half the monthly orders they did mid-year, but at an increased average order value (AOV) of INR 900, as opposed to INR 700 a few months ago.

Grofers seemed to have found its way.

Unit Economics, Stupid

Grofers believed that the marketplace model of owning no inventory and offering hyperlocal delivery would be successful in the low-margin grocery market.

However, the kiranas could not uphold consistent quality over time, and Grofers grappled with inventory woes. The absence of real-time inventory visibility hurts customer loyalty and repeat behaviour. Grofers’ fulfilment rate was close to 78%, with only 60% of orders delivered perfectly.

Considering Grofers’ AOV of ~INR 800, reliance on local Kirana stores for sourcing, offering deep discounts and order volumes coming heavily from staples, they were working on a very low margin of ~5%.

Given a shift of 12 hours a day and their 90-minute delivery promise, a single delivery boy would make around 8 orders a day and 240 orders a month.

Grofers’ cost would include the driver’s salary of INR 20K per month, plus the fuel cost of INR 4K per month.

(15 km per order * 8 orders a day * 30 days = 3600 km; 3600 km/ 60 kmpl [normal Splendor mileage] * 70 rupees per litre petrol ~ 4200 rupees)

With a fill rate of 60%, the actual AOV shrunk to INR 480 and a per-order margin of INR 24 (5%). The cost of delivery of each order was INR 100 (INR 24K cost of delivery/ 240 orders per month per driver).

They were working at a margin of -10%, not considering the cost of dark stores, inefficiencies and miscellaneous costs.

No doubt every player that tried a marketplace model in the grocery delivery segment had either shut down the business or pivoted completely. LocalBanya folded, while Grofers pivoted.

Grofers went the Bigbasket way, dealing with thousands of SKUs. The company became inventory-centric, stockpiling goods in warehouses. It opened large warehouses on the outskirts of cities, delivering via vans at slotted time slots.

With this model, they had real-time visibility of inventory, and the fulfilment rent went up to 98%.

In the inventory-led model, a delivery van shipped out a dozen-odd orders together in scheduled slots, ~100 orders a day.

Adding rental of the delivery van (INR 50K per month), the salary of the driver and a handler (INR 20K per month * 2) and a fuel cost of INR 30K per month for longer distances. The cost per delivered order now came down to INR 40.

In the first big act of the grocery market, the owned inventory BigBasket model was winning, the marketplace of Grofers was beginning to lose.

Crowded Carts

A bull run in the private markets is invariably punctuated by a hot grocery delivery market.

The US witnessed Webvan’s quick success and equally swift downfall as the dot-com bubble burst spectacularly.

A similar frenzy was kicking up in the mid-2010s as e-grocers became the rage again. American startups Instacart and Gopuff and China’s Xingsheng Youxuan were the new poster boys.

In India, the likes of PepperTap, Runnr, Scootsy, TinyOwl and Zopnow among others had been through the revolving doors of hyperlocal, powered by millions of dollars in venture funding. Flipkart was forced to close Nearby in 5 months, and Paytm’s ZIP failed to take off. Swiggy had an underwhelming experience with Swiggy Stores and Ola realised the hard way that it could not get its drivers to deliver groceries.

Internet grocery was anything but an accessible business. It needed deep pockets, large assortment, competitive pricing and astute inventory management.

However, despite rounds of consolidation, the allure of shorter delivery timelines, greater conveniences, and an irreversible, high-repeat habit failed to diminish – to practitioners and investors alike.

Grofers rolled the dice, shut down operations in over 10 cities, entered into ~140 brand partnerships, built cold chains for perishable items, and improved its fill rates. Tying up with the likes of Nestle, Patanjali, Kwality Walls, and Fortune helped develop its marketing credentials, as it offered banner ads for promotions.

Then, in a gutsy move, Grofers discontinued express delivery, as its mass users appeared content with slotted deliveries.

It then drastically cut down its assortment to 1,800 SKUs from the peak of 8K in 2015-16. Fewer items naturally led to higher throughput per SKU and better bargaining power with brands. Key members of the team like Ashneer would leave as the company looked set for disaster.

Its valuation fell from $360M in December 2015 to $66M in Mar 2018. But unlike many other hyperlocal companies that folded/collapsed, Grofers kept going.

Private labels were the next big bet as it invested $7M, engaged 200 manufacturing partners, reverse-engineered cost structures and launched 8 brands across multiple categories. The deep discount to third party listings led to these labels contributing to 40% of Grofers’ gross merchandise value (GMV).

By 2019, Grofers had hit an annual run rate of $700M, with more than a million monthly transacting users. It had broken even in Delhi NCR, which accounted for ~35% of its business. The North Indian belt, from Jaipur to Kolkata, was expected to take it beyond the psychological $1B mark.

Grofers’ valuation was now up to $600M, entering an almost lifelong rollercoaster of value.

Fail Seven Times, Pivot Eight

As Grofers’ user base stabilised, it revealed interesting insights.

For all its focus on “California users” in South Delhi-Gurgaon, its better customers came from East Delhi, Palam, and old Gurgaon.

Many users came from areas without supermarkets. For them, Grofers was an aspirational and utilitarian alternative to the local kirana shop. Many others adopted the platform because, unlike earlier, they could now get pulses and other commodities in a pack. The competition was indeed for losers!

The average annual household income of this core group was INR 6 lakhs. Grofers dubbed them “motorcycle families”, the kind that would typically shop at Sadar Bazaar, had to haggle in its DNA and a keen nose for value. They neither fussed much about speed nor cribbed about convenience.

While Instacart was every grocer’s role model 5 years earlier, Grofers’ new reference point was Aldi, a value retailer from Germany. Aldi’s philosophy was to drive volume through value. It operated low-frill stores, offered prices lower than other retailers and owned multiple private labels to command ~7% share in the UK grocery market.

Grofers’ strategic shift doubled its AOV to INR 1,500 by late 2019. A biweekly frequency for provisions and necessities translated into a monthly outlay of INR 4-5K.

Further, its move from express delivery and heavily rationalised inventory further accentuated its alignment with its new target set. Perishables and dairy products were eliminated from the platform. The intent was to become the platform of choice for household basics, not a genie that could fulfil any impulsive wish.

The platform’s purchasing budget was lowered due to supply chain efficiencies and ease of stocking. However, the narrow assortment and the 24-to-48-hour delivery lag curtailed the scope for premiumization in a hyper-competitive market.

Grofers heavily relied on its monthly subscription programme to boost GMV and on special offer periods to drive customer acquisition.

Low prices would keep customers coming, but maintaining low prices through discounting and cashback would balloon into an unsustainable burden. Although its business model had found a market fit, viable economics remained elusive.

Grofers and its many peers had spent nearly a decade trying to address a very clear need but for customers who neither knew nor articulated the minutiae of their mandate. The e-grocers proposed, over and over again, only for the laws of economics to dispose.

A virus would have to make an unwelcome visit for the hyperlocal delivery players to hit refresh.

Need for Speed

The COVID-19 pandemic opened substantial opportunities for grocery services.

In their newest avatar of hyperlocal grocery, they were called “quick commerce”. This trend, transcending local boundaries, attracted massive investments in grocery delivery across the US, Europe, and China.

Not to be left behind, India’s major retailers like Reliance Retail, Amazon, and BigBasket, along with newer players like Dunzo, Zepto, Ola, and Swiggy Instamart, all ventured into this space.

Grofers, rebranded as Blinkit, had to innovate to remain competitive.

By July 2021, the company was executing 15-minute deliveries in Gurgaon, expanding to 10-minute deliveries across the top 12 cities by August, handling over 20,000 rapid deliveries daily. Zomato would keep its ongoing relationship with Blinkit with a $120M investment.

Blinkit would become a unicorn, the latest in India’s funding frenzy.

A significant shift from its 2015 model, which suffered from poor unit economics and was ahead of its time, marked Blinkit’s strategic evolution.

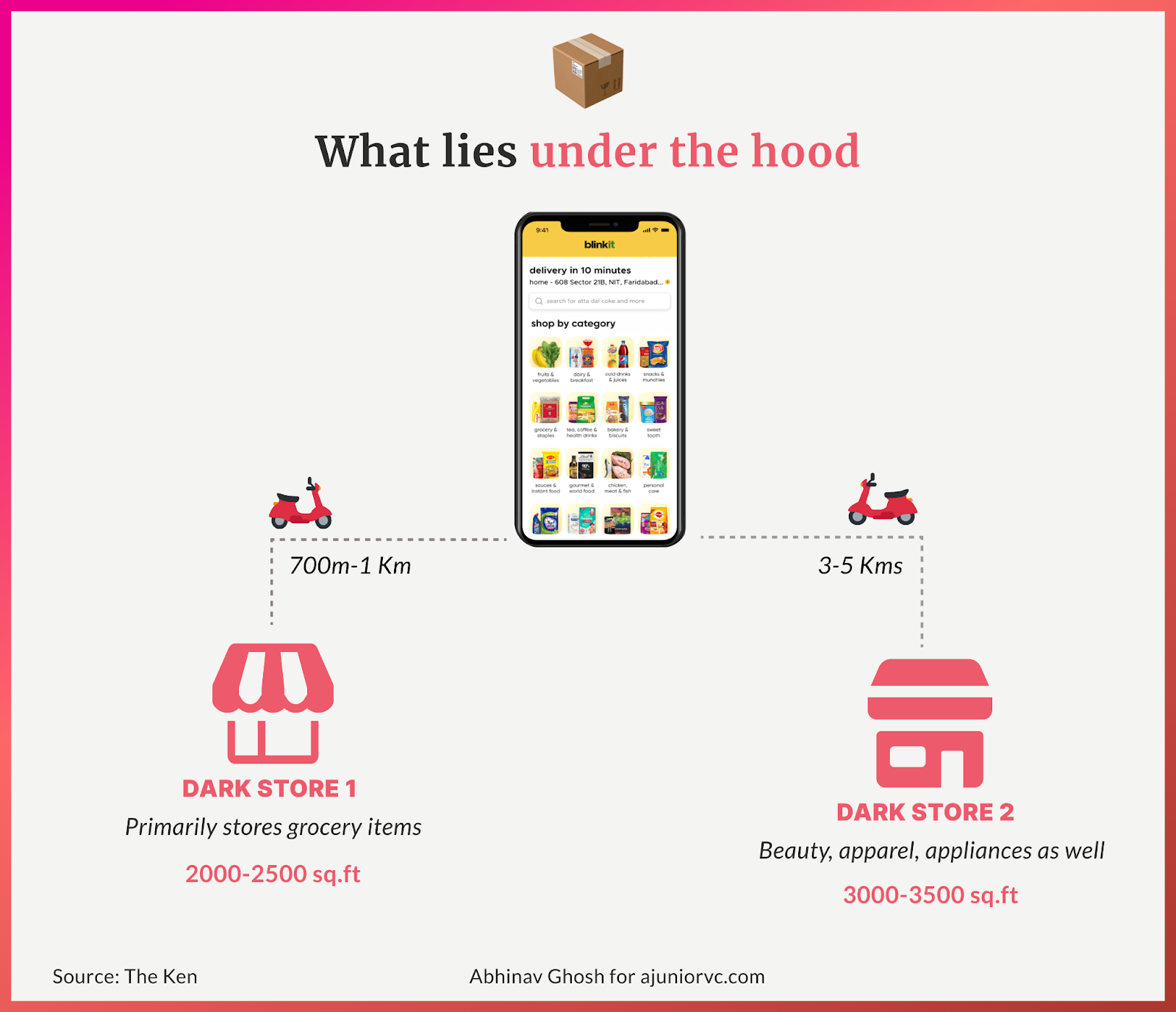

The company transitioned from a dependency on local retailers to a much more robust dark-store model, enhancing operational efficiency and re-engaging many former Grofers customers. This strategic pivot reduced customer acquisition costs and preserved AOVs despite lower order volumes, thanks to customers continuing their bulk-buying habits.

Despite these successes, Blinkit ceased operations in 18 of the nearly 30 cities where it could not sustain its quick-commerce model. However, it simultaneously pursued an aggressive expansion, growing its dark store network from 200 to almost 450 within 2 months.

At its peak, Blinkit was opening a new store every four hours.

Zomato recognised the potential for operational efficiencies by better utilising its existing infrastructure, including using Hyperpure warehouses for Zomato Instant’s hubs.

In 2022, Blinkit was acquired by Zomato in an all-stock deal for $568 million, a move that presented several strategic benefits. This would be yet another down round for Blinkit, in its many rollercoaster valuation ups and downs.

Zomato’s stock would crater by 4,000 Cr, effectively writing off the entire value of Blinkit’s acquisition. The public markets hated the acquisition and the potential bloat it would bring. But Zomato charged ahead.

The merger was expected to yield synergies between Blinkit and Zomato through shared warehouses, cross-procurement strategies, and integrated technology platforms.

Furthermore, potential efficiencies in delivery fleet management were identified, with Blinkit’s operations previously running independently from Zomato’s extensive 300,000-strong delivery fleet.

A new unit was taking shape.

Influencing Quick Commerce

In urban India, about two-thirds of grocery shopping is unplanned, involving small purchases that must be completed immediately.

This shopping pattern is largely due to limited disposable incomes, a preference for fresh food, and small storage spaces in urban households. Despite the presence of large, organised retail chains, traditional Kirana stores continue to thrive because they cater directly to these needs with speed and convenience.

As the pandemic receded, quick commerce began to fade away in Europe and the US. Giant unicorns like Gorillas would fold, being acquired by Getir. The model would fade in prominence in the US.

However, the landscape was shifting in India with the relentless rise of quick-commerce platforms like Blinkit, Swiggy Instamart, and Zepto.

These platforms are transforming India’s $620 billion grocery market by providing services that rival the speed of Kirana stores while offering broader selections, better prices, and over 18 hours of availability. The quick-commerce sector, valued at around $3 billion in 2023, is projected to expand to $30 billion by 2030.

While the jury is still out on the economics of these models, there are clear reasons why quick commerce is potentially working in India. High population density, avoidance of traffic, and availability of disposable income have all come together to see value in the fast delivery model. Customers are willing to pay to deliver an assortment fast while avoiding going out to pick things.

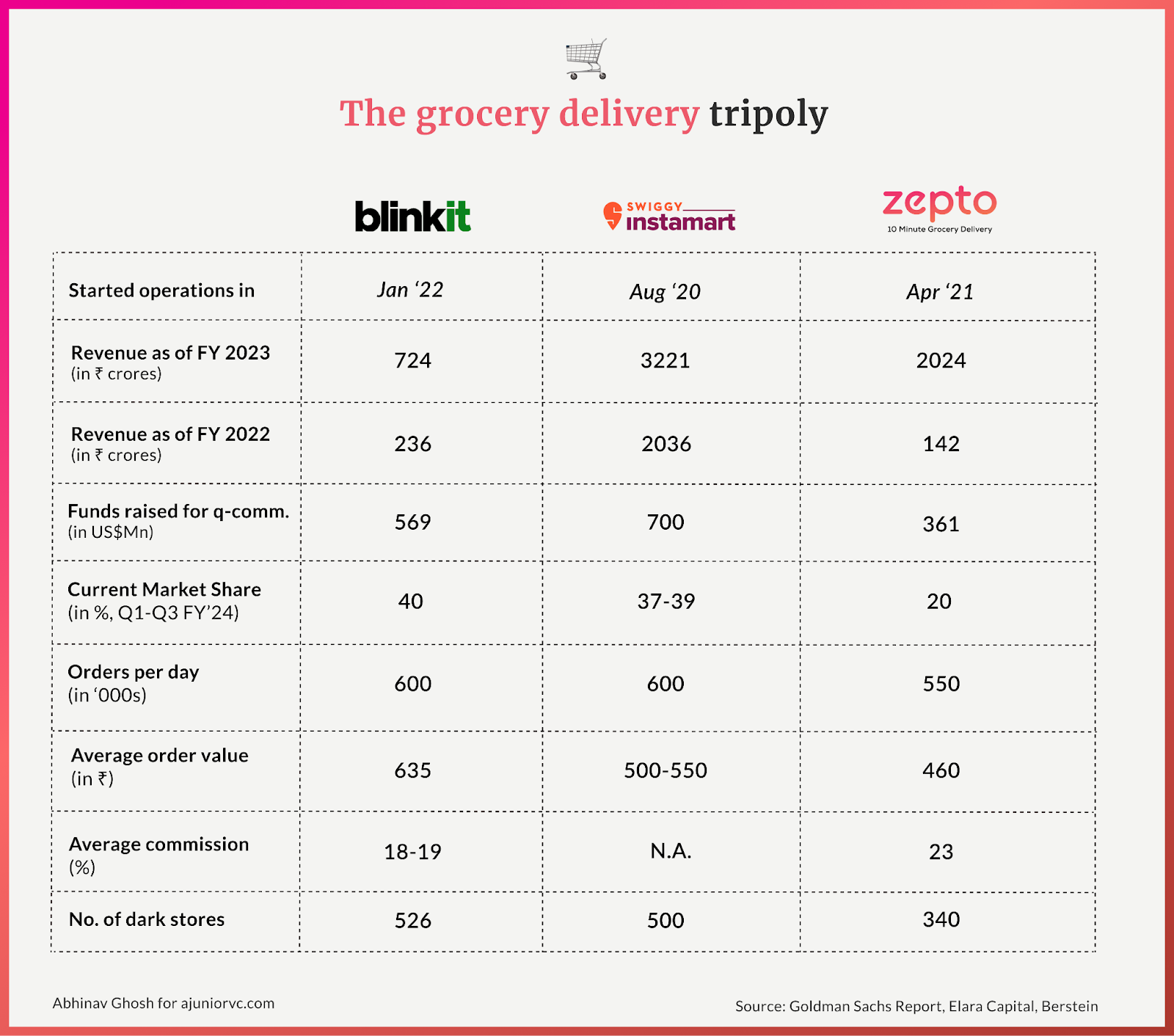

In many ways, these quick commerce companies have productised existing Kirana stores and added a service assurance. Leading this transformation, Blinkit commands a significant portion of the market with a 46% share.

It’s aggressively expanding in major urban centers, particularly Delhi-NCR, which is the main revenue driver for the company. This focus on major cities is strategic, as these areas offer higher transaction volumes and customer density, which are critical for the quick-commerce model.

Blinkit drives over 70% GOV from Delhi-NCR, in particular, saw the most new store openings, reflecting its importance to Blinkit’s overall strategy and revenue generation.

This is a key geography risk.

Blinkit’s future strategy includes opening new dark stores predominantly in key cities across India, with about 80% of its new store launches in Q4 FY24 targeted at the top eight cities.

Overall, Blinkit eyes to have close to 1000 dark stores. Blinkit also enhances its platform’s appeal by integrating established and emerging consumer brands.

This move not only diversifies the product offerings but also improves the average order value (AOV)—a crucial metric in retail that directly impacts profitability.

By the end of FY24, Blinkit’s gross order value surged by 97% year-over-year to INR 4,027 Cr. For Q4 FY24 alone, its revenue was INR 769 Cr, more than double the INR 363 Cr recorded in the same quarter the previous year.

Its value to be an astonishing $13Bn, a 20x multiple from Zomato’s “extremely expensive” $600M purchase in 2021. The company’s rollercoaster was looking up again.

These efforts culminated in Blinkit turning EBITDA positive in March 2024, a significant achievement indicating effective cost management and operational efficiency. This profitability milestone is particularly notable in the quick-commerce sector, characterised by high operational costs due to the need for rapid delivery logistics.

Blinkit’s surge puzzled countless people, happily to those who held Zomato stock, and unhappily to those who had written off the business multiple times.

It pioneered quick commerce in 2015, almost died 3 times along the way, got hammered on valuation, and acquired nearly distressed but has now emerged from the snakes and ladders as king. It’s a decade-long story of resilience, grit, and an unwillingness to stop. It is most definitely one of India’s biggest startup turnarounds.

Blinkit emerged from near death to become a leader in India’s hottest new grocery space, and it seems like its party is just getting started.

Writing: Nikhil, Parth, Raghav, Raj, Tanish and Aviral Design: Abhinav and Chandra

Well written story. It’s astonishing that it surpassed the valuation of its parent company (blinkit $13 Bn means it’s now 2/3rd of zomato $20 Bn) in 3 years. The concentration risk of 70% revenue from NCR alone present a risk as well as opportunity (if one region delivers so much of value then potential is massive across the country). One big risk with this business is there is not much product differentiation across platforms. Blinkit, zepto and other quick marts delivery roughly the same goods. Plus, there are so many big players already in this space, amazon, reliance etc. So,… Read more »

Agree with everything – well said. Thank you for sharing your thoughts

A very well written article indeed!

I would like to bring up that in the reason for shopping emerged, it has been mentioned limited disposable Income whereas why quick commerce is working has mentioned the exact opposite point that availability of disposable income. Just wanted a clarification on that

Last decade has seen a significant improvement in available income to the top 1%, which is the target segment of the quick commerce players

I think one thing Blinkit needs to look at is the concentration risk, i.e., 70% coming from Delhi NCR. It is very common for a company to have its major revenue from its base city, but i think the south market is still not fully captured by Blinkit. It is still dominated by Instamart (being its base location of Bengaluru). Other players tried to grow in this market, but unit economics let them close their shops. I think it can also now cater to new areas like, Delivery of Lab test report, tie-ups with local laboratories. I also have an… Read more »

Yes on the first one. Concentration is an issue. Important to note that such cos can be large businesses just focused on few cities.

On the second one, it is interesting. Why don’t you think Urban Company can do it? It is a small area and can be a nice niche business.