Last fortnight, Open Financial Technologies became India’s 100th unicorn after raising $50M in its Series D funding round.

Founder Families are Gonna Make It

Striking gold in the fintech space was not something new to the Achuthan family.

Brothers Ajeesh and Anish Achuthan and Anish’s wife Mabel had started their first startup together, Zwitch Payments, in late 2012.

Anish and Mabel go back even further.

In 2007, they joined hands to build Cashnxt Technologies. Cashnxt soon stood apart as a contactless mobile payment solution pioneer, using sound encryption to allow contactless mobile payments that work on any mobile phone.

The husband-wife duo had tasted their first blood in entrepreneurship.

They moved on to co-create Neartivity Wireless in 2010. Its product, Simpaise, was a simple, secure and scalable NFC based mobile money platform that worked on any existing mobile phone. Simpaise offered a complete end to end mobile money solution to operators, financial institutions and service providers.

By 2012, e-commerce in India was starting to pick up.

Indian entrepreneurs, inspired by Flipkart and Amazon’s early success, wanted to set up their online storefront to reach their customers directly. However, the buying journey for budding online customers was arduous.

The Achuthan family wanted to streamline the process and started with Zwitch payments.

They realised massive customer drop-offs during the cart checkout phase when customers had to leave the merchant website to enter card details.

Zwitch solved this problem by having its natively web & mobile libraries – Zwitch.JS and Zwitch Mobile SDK seamlessly integrate payment processing into the merchant site, resulting in increased conversions and sales.

It operated almost like a Razorpay but was far ahead of its time.

Zwitch got acquired by Citrus Payment Solutions in 2015, and that’s when the trio picked up their roles in turbocharging Citrus’s growth.

Citrus got acquired by PayU in 2017, but the family had spent enough time in the ecosystem to understand the business banking problems faced by Indian SMEs.

The serial entrepreneurs were looking for the next big hunt again.

Bullish on Opening Banking

In 2017, businesses typically used many tools and platforms to manage their finances.

There was a portal to process and pay invoices, another to manage order and demand volumes, and a third to control the working capital. In most cases, all these tools would be disjointed from the traditional banking platform where all the money movement happens.

An enormous amount of time was spent managing company finances while running daily business operations. Often, companies had no other option but to rely on external finance professionals to help manage the company’s financial records.

There was a glaring need for someone to step in and help the SMEs run their finances effectively.

Open, Asia’s first neo-banking platform for SMEs, was born.

Open looked to solve this inherent problem by integrating traditional banking with all the tools used by small businesses to manage finances – tools for invoicing, payouts, reconciliation, accounting, expense management and payroll.

But Open was not a traditional bank.

Being a neo-bank, they would have to partner with a traditional bank and effectively build. Finding the right banking partner was of paramount importance.

Open v1.0, launched in December 2017, enabled businesses to open a digital-only account. Tools included collecting money and linking up a bank account to withdraw money. V1.0 went live with a select base of 500 businesses for three months.

That was when the steady stream of problems started to pour in.

The engineering team realised tech systems interact with banks a lot. Each of the 14 banks integrated would have its legacy tech that required different integrations. As more banks would get added, the process would be completely unscalable.

Time complexity was high, and creating a common framework for banking integration was the only way out. The framework helped in two ways.

Firstly, the time needed to go live with a bank nosedived. Secondly, developer productivity increased as standard services required to interact with a bank, such as authentication and session management, was in the framework.

With this, any new bank coming into the Open system took only a few days to go live.

Open was truly open for business.

Taking off To the Fintech Moon

Open v2.0 launched in April 2018.

It had an enhanced product that included payment collection and a bulk payout feature. This version lasted for six months. In that span, it had grown to 10,000 businesses using the platform.

In this journey, the team observed that the money collected would get withdrawn to a linked bank account within an hour or two.

The aha! moment then was to build a valid current account with card and cheque book and access to bank branches. Existing desktop accounting software and ERP systems had to be connected to the Open tech stack.

But how do you build for your customers when no such products already exist in the market?

Neobanks were not new to the world, but to Asia, it was.

The founders realised that the only way to innovate and be relevant was to have their ears on the ground. At scale, they realised that live chat support could be a huge channel to collect user feedback.

Coupled with social media listening tools, one-question surveys and pop-ups, the customers were always at the centre of Open’s product innovation. A superior user experience was essential for the team, especially when building the MVP.

Being the first neobank in Asia, there weren’t many investors in the system who understood the product. While the early mover advantage allowed them to capture the young market, they had to demonstrate an apparent product-market fit to raise a pre-Series A funding round of $2M.

The target back then was to accelerate growth and onboard 200K small businesses into the platform by 2020. The vision was that the core platform would launch new lending and wealth management products using AI and financial analytics.

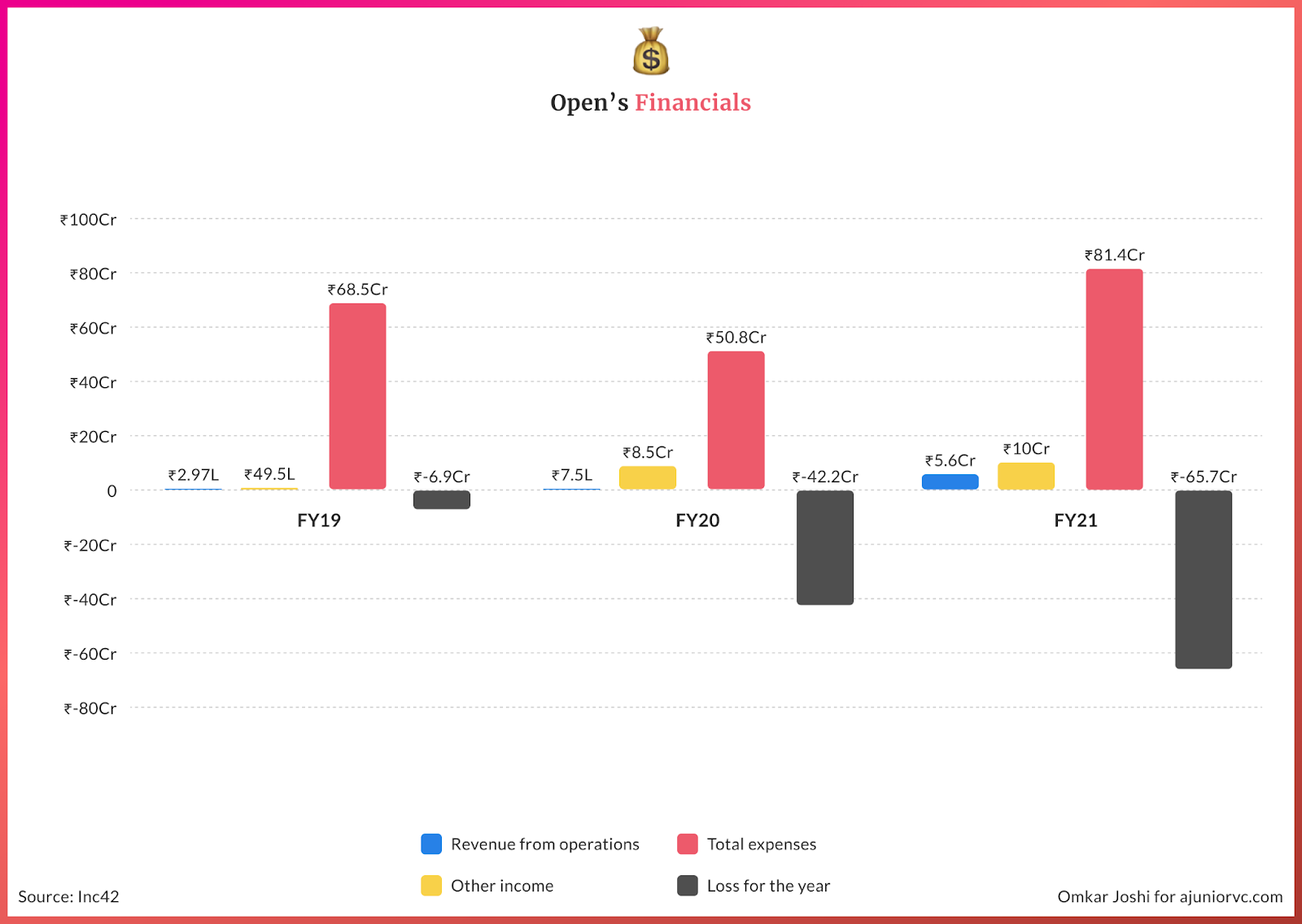

By Feb 2019, Open had grown to have 30K+ SMEs on their platform, processing $2Bn+ in transactions.

The growth rate was astonishing – 7.5K SMEs added every month. Open was well set on its path to reach 1M+ SMEs in the next two years.

On the back of these numbers, Open raised its Series A funding of $5M to trigger its next growth phase.

Tech was enabling the financial inclusion of small businesses everywhere in the world. Open seemed to be at the forefront of it.

It was staring at an enormous opportunity.

A Trillion Dollar Lending Market for Whales

Indian SMEs account for 6 -7% of the formal credit share and face a $ 1.1 trillion credit gap.

SMEs employ 40% of the workforce and account for 30% of GDP and 48% of all exports.

Some of the main challenges that drive this gap were difficulty in assessing the creditworthiness of companies and the requirement of collateral rather than cash flows. Lenders typically relied on past credit history for giving out loans, thus never allowing these SMEs to build a credit history in the first place.

Out of those who can apply for a loan, only 47% get fully funded, primarily due to cumbersome loan application processes. Small business owners are often left waiting for months to decide on their loans. The time was contrary to the bulk of their funding needs for shorter tenures especially working capital loans.

While microfinance lenders catered to the bottom of the pyramid needs, the traditional banks serve large corporations with significant assets and a credit record.

SMEs form untapped whitespace for formal banking services.

These businesses find themselves in dire straits on many fronts – working capital, business expansion, seed funding and property, plant and equipment upgrades.

They could use help in any form.

Emerging startups in the Fintech space began to offer solutions, such as creating alternate data sets for underwriting, co-lending with traditional banks (albeit at higher rates) and digitising the customer onboarding and distribution.

They used technology to make credit accessible, affordable and contextual for SMEs. One such innovation was Embedded Finance (EF).

Estimated to be a $ 7 trillion market today, EF was the integration of financial products for SMEs in non-financial ecosystems. Think of an equipment retailer’s payment and insurance plan just upon purchase. Buy Now Pay Later (BNPL), an example of EF that has taken retail Fintech by storm, is becoming a fast-growing option in B2B e-commerce setups.

The tantalising market size coupled with the bank’s lack of focus meant that the sector was up for grabs and would not be a winner-take-all market.

Each sub-segment could build a billion-dollar loan book, and the great Fintech Festival was about to begin in India.

It was already in process in the world.

Apeing the Global Neobanking Degens

Consumer-focused and technology-driven apps changed the way consumers shop online, order food and travel.

The hard-to-pivot legacy systems of traditional banks combined with lending gaps allowed Neobanks to redefine the consumer experience in money and finance.

Between 2016 and 2020, the global Neobank market clocked 50.6% CAGR.

These banks operate without any physical presence, rely on convenience, and use data to offer the right products to precisely defined customer segments. The approach was to start with a specific service, such as a millennial savings account, cheap forex, seamless international payment or fast SME loans and eventually offer the full suite of banking services.

Each was used as a hook to get into the market.

Europe was the global Neobanking hotspot. It was home to players such as Revolut, Monzo, Starling and N26. Fuelled by regulatory support for access to customer data and easier access to a banking license, the Neobank customer base has grown by 15 million since 2011. By 2023, it will reach an incredible 20% of the population over 14.

As many as 35 Neobanks cater to SMEs in Europe, with 13 offering lending services.

Tide and Starling emerged as the prominent ones, offering services such as a business toolkit, invoice assistance, free money transfers and on-call legal support. This non-banking value makes for a convincing value proposition beyond a mere digital bank.

In Latin America, Nubank saw exponential customer growth, allowing its valuation to reach $10 billion. With a large mobile-savvy but underbanked population, China saw e-commerce players Alibaba and Webank introduce the neo-banking platform ‘MyBank’, which pioneered the collateral-free 3-minute loan application with no human intervention.

Since 2015, the bank has disbursed ~870 billion RMB ($ 128 billion) to 20 million SMEs.

Back home in India, Open, similar to its European counterparts, relied on non-banking services such as automated bookkeeping and expense management to attract new customers.

At best, most of these services came for free or with a freemium model.

In India, there were no RBI licenses for Neobanks.

Neobanks needed to pay regulatory rent and outsource their core-banking responsibilities to a traditional banks. They generated revenue through commissions on customer acquisition, banking products, and transaction fees.

While they operated a low-Capex model that allows better deposit rates and lower fees, Neobanks can’t lend out customers’ money to earn revenue. They collaborate with other banks or NBFCs to offer loans (often small-sized and unsecured) at high-interest rates.

However, for the credit-starved businessman, the risk of lost business or long lead time outweighs the high borrowing cost. Applying and qualifying for a loan at a Neobank is as simple as signing up for any other online service such as food or travel.

Largely reliant on commission or fee-sharing, whether Neobank can monetise through core banking services remains open.

As Open and the world entered 2020, a storm was about to occur.

Growth On-Ramp via COVID Event Trigger

The COVID-19 pandemic proved to be a shot in the arm for Neobanks.

The health risk of visiting a bank branch or handling physical notes pushed customers to adopt digital means.

During this challenging time, Neobanks also proved to be the messiah for small businesses. SMEs looked for emergency working capital loans to keep their businesses alive or restart once lockdowns eased.

While various government and bank schemes tried providing financial assistance to the sector, only 53% of the SMEs out of those eligible for emergency credit line schemes were able to secure loans. In the traditional models underwriting SME customers in the absence of collateral leads to higher operating costs for banks, and many applications do not materialise.

Instead of relying on heavy collaterals or spotless credit history, Open used available business data such as tax payments and the frequency of paying out vendors.

Balance sheet information, often gathered from non-banking services, helps tailor credit services for SMEs.

The pandemic year also saw many traditional businesses and entrepreneurs shift online. Unlike the more evolved, tech-savvy company, these had more specific needs, such as regional language communication.

Open was quick to recognise the trend and built Openbook – a free financial app that comes with an in-built online bank account and tools to manage your business in one place.

Businesses could collect payments via a link sent over Whatsapp, automatically reconcile these payments, and create accounting reports and GST compliant invoices. It turned out to be, as Open calls it, ‘Dhandhe ka Naya sukh’ (newfound peace of doing business).

The embedded finance platform, Zwitch, also saw increased adoption with small businesses looking to integrate payments and lending to up their online revenue streams.

Before its funding round in October of 2021, Open witnessed a 10x growth over 18 months of the pandemic. A high transaction volume fed into the data pool required more customised offerings, which helped expand the customer base.

By the end of 2021, Open processed $ 24 billion in annual gross transaction volume (GTV) and served 2 million SMEs on its platform. The company also reported adding about 90,000 customers to its platform each month.

The pandemic had provided the perfect boost to Open, but it had also boosted competitors lurking.

Neo Bank Group Mining

Thanks to the COVID Pandemic, the Indian B2B and SME space rushed to digitise their processes and establish an online presence.

The neobanks spotted this as an opportunity to get a chunk of the enormous SME pie.

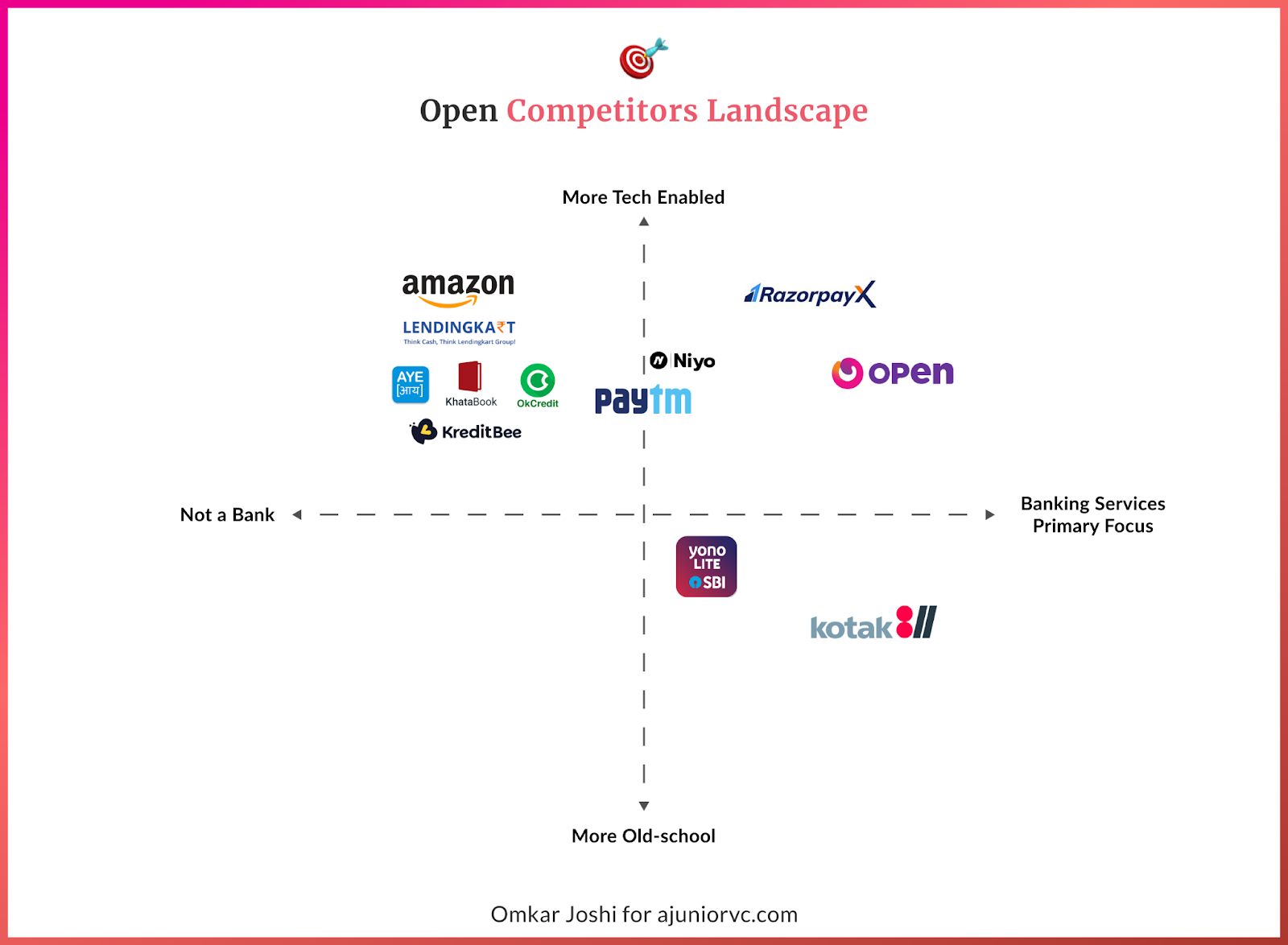

Bank Open was one of the most prominent neobanks in the B2B space.

But others were also rapidly scaling up to steal the limelight. One such was Niyo, which raised $100 million in a Series C round in February 2022.

Similar to other neobanks, it focused on consumers, providing digital savings accounts in partnership with banks, serving about 4 million customers. Niyo says it has processed $3 billion in transactions, making it India’s largest consumer neo banking platform.

Interestingly, Niyo’s payroll solution, Niyo Bharat, provides blue-collar workers with a salary account. In contrast, the payroll software makes it easier for companies to manage workers’ salary information.

More interestingly, the app is offered in over ten regional languages, marking a clear focus on Tier-2 and Tier-3 cities instead of other B2C neo-banks, which are more focused on the metros.

Given that most workers are under-banked in the blue-collar segment, this could be the wedge that Niyo needs to crack the SMB market. How Open competes with this remains to be seen.

InstantPay is another competitor with 1 million daily transactions processed and over 10 million monthly active consumers. Instant Pay has taken a full suite approach with solutions for retail consumers and SMEs and, interestingly, an API banking platform for developers.

RazorpayX’s neobank, which raised $375m in November 2021 and claimed to service 25,000 Indian businesses, is going after the same market. Its offerings include payroll management, current accounts, and corporate credit cards, and it is decidedly more upmarket, with a sleek futuristic design, with clients such as Upstox, Rupeek, and Sharechat.

Many more “neo banking” companies are trying to get a piece of the B2B pie. From public sector behemoth SBI’s “YONO” to other more consumer-focused companies testing the water, such as PayTM and Amazon.

The fight to become a giant won’t be easy for Open, but its strategy was seemingly in the right direction.

Hacking India’s Fintech Rails

Open’s business-focused approach is likely to better than the consumer-focused approach of other neobanks in India.

In markets such as Europe or Latin America, margins for banks are high, and the customer experience in banks is poor.

This creates an opportunity for a new player to come and disrupt the market.

On the other hand, India has a well regulated, thinner margin market. Surprisingly, large banks like SBI are exceptionally technologically savvy. The need for a “better” or “neo” bank for consumers in India may be a bigger challenge.

Banking, at its core is a trusted business. Moving consumers from a high trust large bank to an unproven neobank would require a substantial upgrade in feature sets. For Indian consumers, it is unclear whether this is a considerable upgrade.

Open’s model to provide financial rails to businesses is therefore a better entry strategy. Amid the searing competition, Open also wanted to diversify its offerings and target segments thus.

Open acquired the consumer neo banking startup Finin for $10 million in December 2021. Open aimed to use Finin’s infrastructure to help create an infrastructure for anyone to provide consumer-focused neo banking offerings under their brand names.

This infrastructure play is exciting in the light of how Open recently launched a fintech service platform called Zwitch for fintech and enterprises. Open claims that it is the first no-code embedded finance platform that offers brands and fintech a drag and drop interface to provide fintech services quickly.

Through this, it also targets a growing number of non-fintech businesses aiming to embed various fintech services such as bank accounts, card issuance, payments and lending products in their existing products through its DIY platforms.

Distribution first businesses looking for margin would use these.

Zwitch would take care of the banking partnerships, compliance, and technology through its network of over 15+ partner banks in India. But for more digitally savvy businesses who want customisation, Zwitch also offers full stack APIs that they can integrate.

By doing this, Zwitch competes directly with Instant Pay and a bunch of dev-infra focused startups such as YAP, Decentro, Setu, Hyperface, Card91 etc.

It will be interesting to see how Open will compete with these players. Setu, for instance, invested heavily in a developer community and outreach, similar to Stripe, with innovative open source initiatives such as “D91Labs” to bring research on user behaviours to the rest of the fintech community. Will Zwitch follow such an approach as well?

More importantly, as every company aims to become a pseudo fintech in the future, Open is trying to be a port of call to help them transition to this.

Making Indian SMEs Always In The Money

In May, Open raised $50m and became a unicorn making it the 100th entrant in the prestigious unicorn club.

The plan was to build three new products with the funds raised.

The most interesting is Open Flo, an innovative revenue-based financing product for e-commerce businesses. In essence, revenue-based financing is an alternative method in which companies receive funding based on future revenue.

Usually, under this approach, RBF platforms (which provide funding) will share a small percentage of the monthly revenue as repayment for the capital provided.

Usually, the repayment is capped at a predetermined amount, the capital plus a small flat fee. The developed markets such as the US are leading the way on this method with over $2bn being disbursed as of 2020 and leaders in this space such as ClearCo and Pipe becoming unicorns.

It will be interesting to see how this is customised for the very different realities of the Indian SMB market.

The other two products – Open Settl – an early settlement credit offering, and Open Capital – a working capital lending offering for SMEs, are tied in together to become a cohesive funding partner for SMBs in all cases.

Open has set itself a target to disburse $1 billion in lending through the new suite of products on the platform in the next 12 months, which is a very ambitious number.

One more interesting trend, which could prove a dark horse in this race, is dukaan-tech startups. OkCredit, Pagarbook, Khatabook, which primarily focused on book-keeping, inventory management etc, are all working on adding lending functionality on top of it, as can be seen in this job description of Khatabook.

Credit is the logical next step in helping MSMEs track their cash flow. While these startups have struggled to monetise just yet, they could be a serious challenger.

The SMBs, both large and small, are a significant target for these players.

But what is going to be the most interesting is the infrastructure play that they have planned with Zwitch, especially looking at global trends around the world.

Large global brands such as Walmart and Ikea have shown interest in incorporating banking services into their own portfolio of offerings. Walmart recently announced that it is building a financial-services offering with its financial technology investor Ribbit. Ikea also announced that it is purchasing 49 per cent of its banking partner.

Open is poised perfectly to take advantage of the “everybody wants to become a bank” gold rush if this trend holds. As Mark Twain is supposed to have said, “during a gold rush, sell shovels”.

As we enter a new decade amid turbulence, our 100th unicorn looks well poised to provide the shovels for businesses. In a still underbanked country, Open could Open up banking for Indian SMEs.

Writers: Chandra, Keshav, Raj, Rajiv and Aviral Design: Omkar, Shelley