Last fortnight, the ED began investigating crypto exchanges in connection with instant lending apps, soon after, the RBI banned PPI instruments from loading via credit lines

Centuries of Becoming Credit-worthy

Some people say money lending is as old as humans.

That is probably no surprise given the human race’s propensity for innovation and risk-taking. Money lending in India is no different, it is an ancient practice. Traces of a faint credit system can be found as early as the Vedic period in India.

The practice of lending at unreasonably high-interest rates was considered immoral early on.

However, in the late 2nd century BCE, lending became an acceptable wealth creation mode. The Manusmriti, one of the many legal texts and constitution among the many Dharmaśāstras of Hinduism, even recognises the practice of lending as ‘Kusidin’.

A systematic structure of money lending emerged during the Mauryan age – 185-321 CE.

Chanakya referred to different forms of loan deeds in his texts. Ancient Sanskrit treatises like the Arthashastra and the Dharmashastra have references to bills of exchange providers to traders to help them carry out foreign trade and extend business loans. They also made caste an essential factor for money lending.

Centuries later, another form of money lending emerged during the Mughal era.

The process was known as dastawez, which were of two types. One which was payable on demand that is the dastawez-e-indultalab, and the other payable after a period, was the datawez-e-miadi.

There were two other prominent money lending tools- barrettes, payment orders given by the royal treasuries, and Hundi, which was used during credit transactions, much like the modern-day credit card.

As the Mughals declined, the Industrial Revolution, 1733 to 1913 A.D., began sparking a transformation in society from an agrarian economy to manufacturing and industrial processes.

This, coupled with the emergence of the British Raaj in India, meant India’s entire credit infrastructure became more structured and took on an anglicised form of lending and banking.

Most aristocrats and merchants extended business loans to entrepreneurs to help them rapidly expand their workforce. Indentured loans were also popular where the borrower had to repay the debt by working on the lender’s estate.

During the early days of the East India Company, Seths and Shroffs carried out money-lending and extended small business loans to merchants to support their trade.

India also witnessed the birth of various banks during British rule. In 1770, the first European bank, the Bank of Hindoostan, started its operations in Calcutta to provide business loans for foreign trade.

However, it failed in 1832.

With the birth of three presidencies—Bombay, Bengal and Madras—banking activities started in full swing. The Bank of Calcutta was established in 1806 to fund the wars against the Marathas and Tipu Sultan. Then in 1865, the Allahabad Bank was established, which remains functional.

The first Indian bank to establish was the Oudh Commercial Bank, followed by Punjab National Bank in 1894, after its early demise.

The Swadeshi movement brought about the establishment of quite a few banks in the period between 1906 to 1911. Indians established several small banks which served particular ethnic and religious communities. Several established banks have survived to the present such as Catholic Syrian Bank, The South Indian Bank, Bank of India, Corporation Bank, Indian Bank, Bank of Baroda, Canara Bank and Central Bank of India.

While the small Indian banks cropped up, the exchange banks – which concentrated on financing foreign trade – mainly were European-owned.

Indian joint-stock banks struggled from being under-capitalised. They were not seasoned to compete with the presidency and exchange banks.

But the winds of change were flowing through the country, which would altogether transform lending.

Liberalising to Have Outstanding Balance

The pre-independence period was characterised mainly by private banks organised as joint stock companies.

Most banks were small and had concentrated private shareholding. They were primarily localised, and many failed, especially in competing with their European-owned counterparts.

These banks came under the purview of the Reserve Bank of India (RBI), established as a central bank for the country in 1935. The RBI was established to respond to the economic troubles India was facing after the First World War

With the creation of the RBI, India could now lend or borrow money from other countries. But the process of regulation and supervision was limited by the provisions of the Reserve Bank of India Act, 1934 and the Companies Act, 1913.

The indigenous bankers and moneylenders had remained mainly isolated from the institutional part of the system. The informal lending network was still rampant and exploitative. Co-operative credit was the only hope for credit, but the movement was successful only in a few regions.

Unfortunately, the partition of 1947 hit the banks adversely, especially the Punjab and West Bengal economies. With independence came the end of Laissez-faire banking in India.

In 1949, RBI was nationalised, and the RBI implemented the Banking Regulation Act to regulate and control the interest rates on bank loans by Indian banks.

The first 20 years of Independence posed several challenges, with an underdeveloped economy presenting the classic case of market failure in the rural sector, where information asymmetry limited banks’ foray. Further, the non-availability of adequate assets made it difficult for people to approach banks.

During this time, the State Bank of India (SBI) expanded massively in the under-banked and unbanked centres, spreading institutional credit into regions which were un-banked thus far. Proactive measures like credit guarantees and deposit insurance promoted the spread of credit and savings habits to rural areas.

There were, however, problems with connected lending as many banks were under business houses’ control.

Significant developments characterised the period from 1967 to 1991.

Social control on banks in 1967, nationalisation of 14 banks in 1969 and creation of six more in 1980. The nationalisation of banks was an attempt to use the banking system’s scarce resources for planned development.

The task of maintaining a large number of small accounts was not profitable. A result of this was they had limited lending in the rural sector.

The problem of lopsided distribution of banks and the lack of explicit articulation of the need to channel credit to specific priority sectors was sought to be achieved first by social control on banks and then by the nationalisation of banks in 1969 and 1980.

The Lead Bank Scheme provided the blueprint for further bank branch expansion.

The period post the first way of nationalisation was characterised by rapid branch expansion that helped open the lending channels far and wide across the country.

The share of unorganised credit fell sharply. However, the stipulations that made this possible and helped spread institutional credit and nurture the financial system also led to distortions.

The administered interest rates and the burden of directed lending constrained the banking sector significantly. There was very little operational flexibility for the commercial banks. Profitability occupied a back seat.

Banks also suffered from poor governance. The financial sector became the ‘Achilles heel’ of the economy.

Fortunately, for the Indian economy, quick action was taken to address these issues.

Rich Technology

The period beginning from the early 1990s witnessed the transformation of banking as the country was unlocked.

The reform process helped take the banking sector’s management to the level where the Reserve Bank ceased to micro-manage commercial banks. It began to focus largely on the macro goals.

The focus on deregulation and liberalisation coupled with enhanced responsibilities for banks made the banking sector resilient and capable of facing several global challenges.

Liberalisation also coincided with globalisation, India opened itself to the global economy.

This helped bring in what we today know as the new generation of tech-savvy banks. In 1994, banks that we know today and trust, such as ICICI, HDFC, and Induslnd, came about during this era.

With foreign direct investment pouring in, the new policy waves in the banking sector. This ushered in a state of the art methods of lending and borrowing and the introduction of new credit instruments.

1991 marked a new beginning for business loans due to the rise in technology. The internet revolution began, and the banking sector embraced it with open arms.

Technology automated a lot of core banking services. Modernisation of payment services and settlements through Electronic Clearing Services (ECS), Real-Time Gross Settlement System (RTGS) and National Electronic Funds Transfer (NEFT) also opened up new opportunities for businesses.

Customers could now avail business loans online. This sped up the lending process and encouraged more borrowers to apply for loans.

On the back of these advancements, credit growth took off. Domestic Credit to the private sector as a % of GDP increased from 23.8% in 1991 to 50.6% in 2010.

This coincided with staggering GDP growth as the economy grew from $270B to $1.7T in the same period. In comparison, Domestic Credit to the private sector as a % of GDP increased from 12.5% in 1971 to 24.9% in 1990.

The growth in formal lending was just staggering. The banks were riding on this growth and saw their business boom and valuations soar. HDFC Bank’s valuation increased 47 times from its listing in 1999 to the end of 2010.

The rapid growth in loan books can usually be harmful, but India’s growth wasn’t. It happened in the largest banks, with credit expanding to all parts of the country.

By 2008, Bank assets were 90% of the GDP. Credit was given to businesses and consumers, with loans at ~57% of GDP.

The banking system was also maturing, consolidating while the overall segment grew. Individuals formed 48% of the lending pool, while institutions got 52%.

India’s growth was impressive, so it resiliently managed to withstand the 2008 Global Financial Crisis.

But like all good tales must come to end, this one was about to take a hit.

A Fintech Opportunity Out of Ruin

In 2010, Indian credit penetration, even after all these reforms, was still at 48%.

As the world slowed down, India still kept the pedal on growth going. By 2011, India was growing but facing inflation and financial stability headwinds.

In 2012, India came to a sudden halt. Bank NPAs shot up, lending froze, and the rupee depreciated from $44 to almost $65.

We seemed to be on the brink of a crisis. By 2013, the call to replace the government was rampant due to scams and a crashing economy.

The financial system’s strain requires us to understand what makes lending tick.

If the borrowers return their loans on time, lending is a highly profitable business, perhaps the best in finance.

At first glance, it is an easy-to-understand business. A borrower comes to asking for money, you provide the money, and the borrower pays you back the amount over time along with interest due for the loan.

From the lender’s perspective, the difference in the interest paid by the borrower and the cost of funds is the profit from the activity for that year. The second appeal of lending lies because it seems infinitely scalable. A lender with a larger balance sheet can lend more and earn a higher volume of profits without many changes in the operations.

At first glance, this looks easy till you factor in two points.

The first is the default rate, and the second is the power of leverage. In good times, these two factors are in your favour, and the lending business looks spectacularly profitable. In bad times, several lenders see their business wiped out.

It is unthinkable that there can be a lending system with no probability of default. In addition, such a risk-free system is one where the interest would be lower and unsatisfactory to the lenders and their funders.

Interest essentially prices for the risk of default. Higher interest rates are priced in.

Practically speaking, it is almost certain that any lending system will see default. It is also well known that default rates are cyclical. Double-digit default rates skyrocket in all parts of the economy in a downturn like the global financial crisis.

Indian NPAs and interest rates both began to shoot up. A bad economy almost always results in a change of government. A new government was formed in 2014.

The new change was afoot in the startup ecosystem as well.

Fresh from a global recession, new upstarts had begun to innovate globally. As India hurtled into financial stress, fintech sprouted up to plug the gap as well.

The wave of fintech in India was broadly comprised of wallets like Paytm and payments like Billdesk. In 2015, PayTm raised a monster $900M round, the largest for an Indian fintech and one of the largest for an Indian startup.

Lending-focused startups like Lendingkart and CapitalFloat began to sprout up. The lending/credit story in Indian fintech was beginning to start.

For that to work, the lending upstarts had to learn how lending worked.

Making Money, Lending Wise

Over decades, banks have built systems and safeguards to ensure lending works as a business.

The capital reserves and the equity capital ensure that the lending institution can cover the loss due to default from its equity capital.

If the institution is not well capitalised, it would mean winding up. Since the lending institution borrows funds to lend to its customers, a slight change in the default rate may wipe out the entire firm. This is the inverse of the power of leverage.

The banking history is replete with several lenders who have been wiped out due to a downturn and inadequate capitalisation. Hence, ideally speaking, any lending institution which has become profitable must keep adequate buffers for the winter whenever it comes.

The critical point of focus in the lending operation is to figure out and identify a customer segment that needs capital and would have lesser chances of default.

Traditionally, 5Cs of credit form a heuristic to estimate the chance of default and the loss to the lender.

These are the applicant’s Character (measured by credit history), Capacity (measured by debt to income), Capital (existing capital of the borrower), Collateral and the Conditions of the loan as proxied by the purpose of the loan.

Different loan products are formed by mixing and matching the above five characteristics. For example, a home loan, which has a large ticket size, would require collateral (the home itself, for example). In addition, the bank would typically fund a max of 80% of the cost of the home.

This type of loan is secured, meaning that collateral backs it.

The other side of the spectrum is unsecured loans, which are not backed by collateral. These loans are riskier and are consequently of lower ticket size.

The extent of the personal loan sanctioned to anyone primarily depends on income. Personal loans and credit card loans are prominent examples of unsecured loans.

In 2015, the fintech wave in India saw the emergence of several companies that decided to operate in the unsecured space.

P2P lending was the hottest and most visible example of unsecured lending. There were a couple of reasons for this.

Since unsecured loans are riskier, they have a higher interest rate, improving profitability, even at lower volumes. For any individual who had collateral, it is evident that the existing banks would service them.

The loans would be secure, and the borrower would get a lower interest rate as the cost of funding for the banks is much lower.

The fintech also knew that the unsecured personal loan market was one where the traditional providers did not want to enter, so there was lower competition. In addition, since India was a credit-starved country, there was a large market here waiting to be tapped.

In this unsecured personal loan segment, there are a few other necessities in the business, making the field more suitable for fintech than banks.

The market for personal loans is geographically dispersed throughout the country. Any individual in any part of the country may need a personal loan at any point, especially for emergencies.

Often the need for a personal loan is quick and instant disbursement is a desired feature.

In 2016, Jio dropped, and it turbocharged the entire startup ecosystem. Lending would see a boost.

Downloading a mobile app would give the fintech access to alternative data sources such as location, spending history (via SMS), and phone. This could be used to estimate a person’s character better, especially if there is no credit history.

Digital-first operations kept a lid on operations costs and did not let them increase proportionately based on the number of loans disbursed.

Despite all this, P2P lending never took off due to issues with the model. Just having tech does not make a fintech.

Indian fintech needed to look for a better model.

Non-Banking Checks

In 2017, only 12% of India was credit served, with 67% still credit unserved, and the rest, 21%, were either newly acquired or underserved.

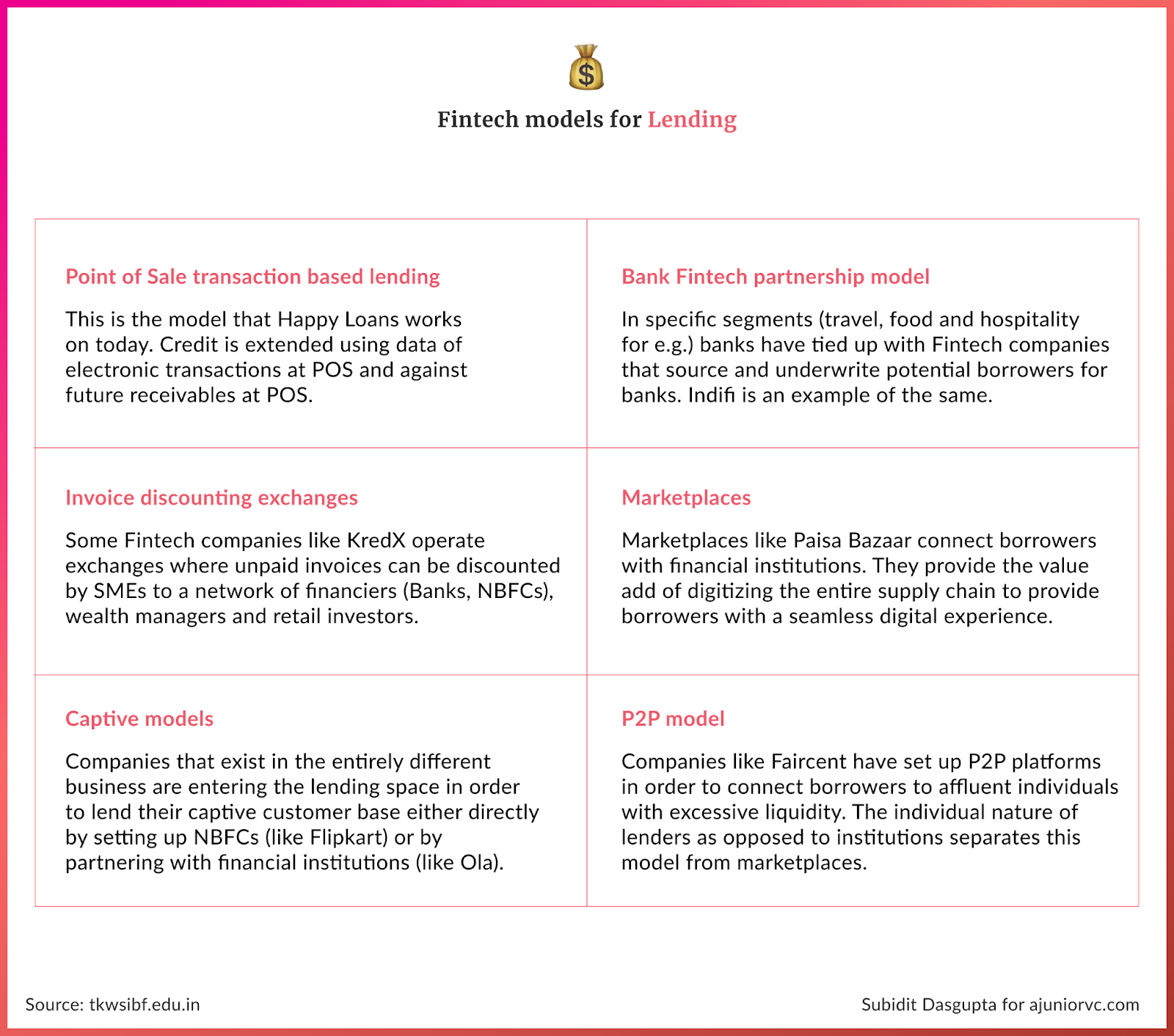

Most of the lending took place at the loan market places like Bank Bazaar and Paisabazzar that had tie-ups. NBFCs and Banks provided capital to them while the loan origination and the loan management were with the financial institution.

None of the risk policies was changed, and the newly credit served did not grow much.

India was at its nascence stage of credit lending in India. Pawn Brokers were still charging 36%+ per annum from MSMEs, and consumers still did not have access to credit.

It was clear that credit was not readily available to the masses, and every company had to be a Fintech company to reach the masses. But there was a problem; over 85% lacked credit scores.

We were still heavy on the informal loan market, with pawn brokers huge in the market.

Banks continued to serve their consumers, and their risk policies had not changed. Prominent NBFCs like Bajaj finance were growing their loan book rapidly with tech front capabilities. They were the initiators of the offline Buy Now Pay Later model in India.

By 2018, many peer focused NBFCs started erupting as digitisation to save grew. These P2P NBFCs could now lend to more audiences.

At almost the same time, established NBFCs like IIFL started to blow up, cratering the entire market. A major crisis was beginning to engulf the overall market. The smaller ones were not immune.

Many consumer digital applications like Kreditbee and Early Salary faced heavy NPAs in the early days due to the lack of collection mechanisms and eased underwriting policies.

Other B2C and B2B credit models were getting started as alternate data providers erupted and underwriting capabilities increased.

Traditionally, only credit bureaus were the core data providers; other data were mobile scrapping, email scrapping, cash flow-based lending, and alternate credit platforms.

But still, lending was restricted.

Startups had to find ways to lend on various forms of intangible Collateralization. Once a distribution is attained, they could offer a point of sale or purchase credit. But such purchases are limited to their ecosystem.

Ofbusiness that had already built a B2B marketplace started lending to the sellers to maximise their sales. As they made the escrow channels, they received the payments in a collateralised way.

Likewise, POS-based lending grew drastically with merchants that were accepting card payments were lent money, and the POS-system provider withheld the incoming transactions.

Companies like Pinelabs and BharatPe were born out of this need, coming on the scene in 2018.

E-commerce players thrived in this space by lending directly to consumers and merchants selling on their platforms. Amazon partnered with Capital Float, and Flipkart offered its capital.

Other startups with distribution in different segments also started their financial product. Ola had their Ola Money, Swiggy had their Swiggy money with its co-branded solutions, and Zomato ventured into the space. While the mantra is upselling and giving to the consumers’ various financial services products, success is yet to be proven.

By the end of 2019, there seemed to be many players, but they were still serving a small market.

The landscape was crowded as the new kids fought for a small consumer and business pie.

An Advancing Fintech Landscape

One could broadly categorise the upstarts into personal credit and business credit.

The personal credit landscape comprised of BNPL firms (e.g. OneCard, Unipay, Slice, Simpl), Personal loan firms (e.g. Navi, SmartCoin, ZestMoney), P2P Lenders (e.g. Faircent, i2i funding etc.) and digital channels of incumbent banks (e.g. YONO for SBI, iciciMobile Pay).

This fintech either lent on their books or partnered with other financial institutions. In the latter case, the fintech acted as a Direct Selling Agent and utilised their underwriting algorithms based on their digital data as their competitive differentiator.

The final lender often makes it mandatory for the fintech to have some skin in the game for the loans. This is operationalised through FLDG (First Loan Default Guarantee) agreement.

For existing financial institutions, a deal of this type allows them to expand their loan book without having to invest in spending on additional distribution.

The B2B lending space is the larger of the two is an equity capital-starved country.

Of the firms listed on the exchanges, approximately 70% of their total capital comes via debt.

The situation for MSMEs is likely to be a lot poorer. In this regard, the availability of debt funding in the MSME space is vital for their growth.

Lendingkart had already completed 4 years by 2019 in the space as new players began to sprout up a few years after it started. The disruptive moment in this space came up with the launch of the GST in 2017.

The GST system allowed any party to verify the invoices generated by the MSMEs on the GSTIN portal. This effortless verification system improved fraud detection and gave a better estimate of the ability of the MSME to repay.

Over time, other business models for lending have also come up.

For example, RupiFi offered embedded lending to shopkeepers and retailers when they buy goods on B2B marketplaces such as Walmart and Udaan. By late 2019, firms like Velocity offered Revenue Based Financing to online D2C merchants based on their sales on e-commerce platforms.

In early 2020, there was discussed on the advent of the Open Credit Enablement Framework (OCEN). This was likely to improve the availability of loans and the monetizability of transaction data.

For example, Swiggy and Zomato will be able to offer loan marketplaces in which their restaurant partners can share their order volumes data with banks/fintech to get short-ticket, short-tenure loans for their purchases. The GeM Sahay portal offered services such as Purchase Order Financing to individual MSMEs who sold to the Government.

But as 2020 progressed, the whole world was hit by a storm.

No Haircuts, Only Lending Growth

As 2020’s pandemic hit, startups and lenders had to brace for two winters – COVID 19 and The Reserve Bank of India

The credit grew, fintech startups and NBFCs curated the risk policies as the markets digitized, the transactions increased, and so did NPA.

The private banks were at 2.23 per cent and of NBFCs and HFCs at 3.77 per cent; public sector bank delinquencies stood at 5.03 percent, but the Fintech startups were at 6.6%.

Many of the new-age fintech applications had given out easy loans and had to write off the loans. Some did not even report to the Reserve Bank of India.

RBI is one of the most stringent regulators in the world and had not taken this to be easy.

It started with the multiple Chinese loan apps. RBI had found that over 600 lending applications were illegal with irregularities in the KYC format, and 27 have been banned. Some of which were allegedly bringing black money into the country money.

Before 2021, apart from the banks, only two NBFCs had the license to issue a credit card in India without co-branding.

This led to fintech applications finding a way to propel credit cards with a pre-paid Instrument card, cash loaded by an NBFC and a card provided by a PPI issuer. This moved the credit card issuance in India from 29 million in 2017 to 62 million in 2021.

But the RBI did not like the move of PPI in the market and banned the functioning of such practices as it had informed the startups to follow legal procedures, whether by co-branding with a bank or getting a credit card license on its own.

While the RBI was doing its part at a scale, the organisations building the account aggregators braced for India’s one-stop shop for data sharing with users’ consent.

No country had built such a system for sharing data in a decentralised way.

With multiple Financial information providers, Finacial information Users, sharing data and Technology service providers like Fego.ai acting as agents, India is now rushing to enable credit for all.

Just as UPI was for debit transactions, Open Credit Enablement Network will ensure that we scale credit transactions are enabled at scales for the masses.

At the same time, the RBI raised rates, and the interest rates increased for all the banks, NBFCs, consumers and businesses from 4% in May 2020 to 5.4%.

We returned to the drawing boards and listed the four most essential factors in Fintech to succeed: the cost of capital, collections mechanisms, low cost of customer acquisition and underwriting abilities.

Going for Broke

We entered 2022, and the credit story had improved.

Of the country’s 81.4 crore credit eligible population, 40.8 crores or nearly 50 per cent was credit unserved while 16.4 crore or 20 per cent was credit underserved, and almost 8% were new to credit.

This leaves only 22% credit served in the form of overdrafts, credit cards, secured and unsecured loans, Cash flow-based loans, POS lending and invoice discounting.

India still stands at one of the world’s lowest credit card penetration and household debt to GDP.

We are still awaiting our UPI moment in credit. It may just be UPI on credit that enables this.

The rate at which UPI has grown would allow the consumers to pick up credit on UPI at a faster rate, with merchants enabling high transaction value and volume.

The only issue is that the NPCI has currently only allowed RuPay credit cards on UPI, with only 1 Million cards RuPay credit cards in the ecosystem.

Therefore, other forms of credit on UPI needs to be enabled to enable credit to the 64 crore Indians of the 81 crores eligible for credit.

While credit platforms cannot build a distribution overnight to reach the masses, either it has to be an embedded form of finance or provide digital infrastructure for platforms that have the distribution.

Companies built for the future in lending look at two broader aspects, one with credit risk and another without credit risk.

Companies co-lending with the banks had acquired a low cost of capital.

Onecard is a credit card company that recently turned unicorn and has partnered with many banks.

Pure lending companies like Slice, Uni, Lazypay and Simpl have grown drastically and need to control the credit risk. With over 5% of NPAs, it might hurt in the long run to serve the market.

Other lending players like Refyne and Jify that offer earned wage access, give only the earned capacity of the individual with partnering with an NBFC.

Companies providing technology solutions are increasing due to less or no credit risk on their books. These enable large financial institutions to lend seamlessly.

India with a population of 153 crores and 110 crores of bank accounts. Banks hold the most extensive distribution in the country is with banks. Technology companies serve them directly.

The idea of creating a new credit company seems unviable.

Instead of enabling the mega institutions to lend at scale and to ensure the risk is controlled, underwriting capabilities increase and building robust collection mechanisms is what the next wave of Fintech should focus on.

M2P Fintech is a Fintech Infrastcutre company that predominantly enables credit for various financial institutions and Fintechs at scale. It has provided at least some function for almost all the PPI credit card players in the country.

Models to ensure that the assets teams can directly liaise with liabilities are critical to future intangible collateralisation.

Finsire is an infrastructure firm that operates overdrafts as the actual credit opportunity for the masses. They collateralise the loan and ensure that banks and NBFCs co-lend the earned capacity to individuals and businesses.

While being a supreme savings economy, we believe that credit is evil; on the contrary, it unlocks the potential for businesses and individuals to increase the total output.

Every fintech, though, is chasing lending as a monetisation tool. With the advent of UPI and the reduction of the cost of moving money, it is indeed the mechanism to make money.

A feature that could perhaps be added, but also the most significant money driver for fintech firms, just like banks.

We are still in the first innings of the credit journey compared to the world.

As companies are being built as credit providers and credit enablers grow, India will progress only if we maximise our potential and provide credit at scale.

Credit will play a crucial role for India to attain the 5 trillion dollar mark while being a true money spinner for the financial institutions.

Writing: Nilesh, Varun, Shreyans and Aviral Design: Blair and Subidit

What an amazing journey of lending through history AJVC team