Last fortnight, MX Player raised a $100MM, adding more firepower to fight in the fast-growing OTT market. On the other side of the world, Disney+ launched and reached 10MM users in 3 days, with a 2020 launch planned for India.

Starting with a Big Bang

‘Kabhi kabhi toh lagta hai ki apun hi bhagwan hai’

This godly feeling might well be true for Netflix’s strategy in India which pumped in its highest ever investment of INR 100cr (~$14MM) on the second season for Sacred Games, which premiered earlier this year. With a runtime of 400 mins that’s $35K per minute.

Yes, it was as expensive as a movie.

That competition in the OTT streaming market in India is heating up would now be an understatement. There are 40+ players competing in the cluttered OTT market vying for your attention. How did we reach this point where India now counts as one of the most attractive markets in Asia for OTT?

Let’s YouTube rewind a bit.

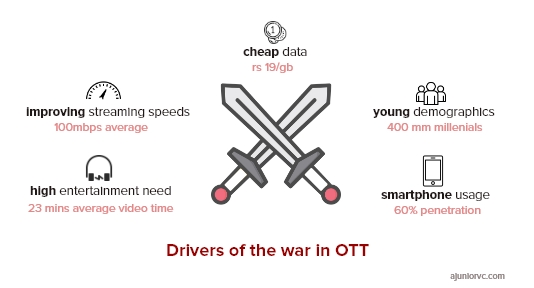

The transition of India moving from an economy led by bottom of pyramid to one led by the middle class by 2030 was happening through the surge in smartphone penetration in the country

Smartphone users were expected to touch 859 MM by 2022 from 468 MM users in 2017, growing at a CAGR of 12.9 percent. What this statistic said was that everyone had access to a screen.

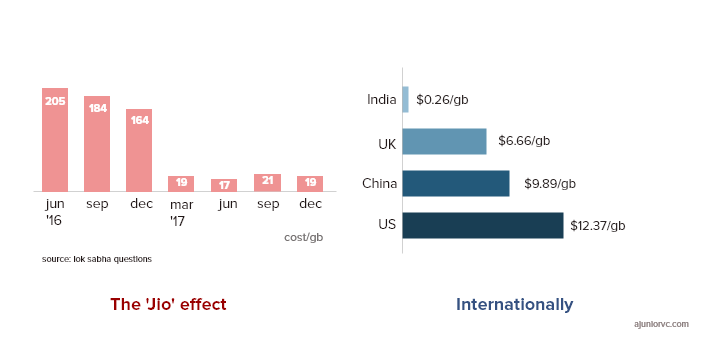

In 2016, Jio disrupted the telecom market by crashing internet data costs and free voice calls. Its effect has been amplified to an extent that no industry has been immune.

It has given birth to entire new industries (Agri Tech, B2B e-commerce) or disrupted existing ones (OTT)

The crashing of telecom prices is evident, and India is the cheapest market for data globally by a mile.

Jio’s data flood was soon about to alter customer behaviour.

The Godfather

If something is too good to be true, it almost always is.

But what if the other person made you an offer you can’t refuse. What if he gave you high-speed internet and rock bottom prices and you could call anybody for free?

This is what Mukesh Ambani did when he launched Jio. He changed the fortunes and behaviours of tens (hundreds?) of millions of people literally overnight.

That fateful day in 2016 democratised internet for India (actually, Bharat) and made the internet the fourth pillar of our existence in the 21st Century (Roti, Kapda, Makaan anyone?).

If data is the new oil, are telecom companies the new miners? Or are they the new suppliers? Well, that depends on how you choose to look at it.

When data prices are high, people are averse to consuming a lot on the go. However, when data prices plummet to a level where people don’t have to restrict their consumption anymore, their behaviour starts to change.

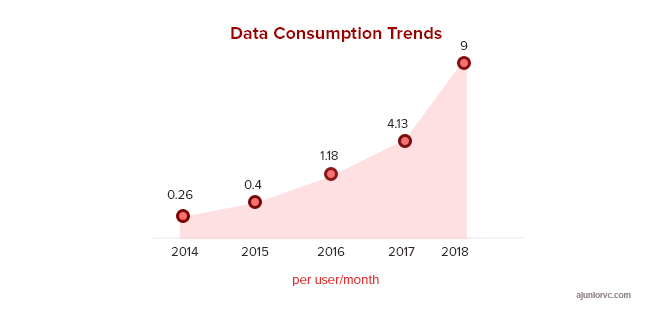

Before they know it, they’re hooked. We’re all hooked. We’re consuming all the time. Mobile data consumption has gone up from 0.26GB per user/month in 2014 to 9GB today, a 30x explosion in just 4 years.

Now, an important question is – what are people doing with all this data? How are they consuming it?

The one-word answer is video.

Consumers now regularly use the internet to enter a new world. This magical online world transports them to new places every time. From a dystopian future, to an ashram run by a baba who wants to reignite the world, to the hinterlands of India, to the upper echelons of Delhi and its big, fat weddings. They get it all.

Turns out, videos and some funny ‘white stuff’, that we will allude to later, have something else in common. Other than transporting people to a new world – it’s extremely difficult to get off it.

The captivated eyeballs that the internet would bring could not be left unattended.

Sher-locking Eyeballs

2016 marked the entry of Netflix and Amazon Prime.

The two global streaming giants, with their ‘capital’ moat were ready to woo the millennial class tired of Indian drama and soaps on television.

All this led to a heady mix of fresh, compelling content invigorating the content creation, production, distribution industry. Millennials started ditching TV for online content

India was also moving towards a young population using mobile to consume content for entertainment. By 2030 India will be one of the youngest nations on the planet with 1 Bn internet users. The rich and connected aspirants (26%) will spend 2-2.5x more on categories such as gadgets and 3-4x more on services, i.e. entertainment.

Sensing the opportunity, local home-grown brands such as SonyLIV, ALT Balaji, EROS Now, Zee5 among others emerged in 2017-18. Not to forget was YouTube and production houses such as TVF Play, which we had analyzed earlier.

All the players were out to ‘attract and retain’ eyeballs and wooed potential users with cashbacks, freebies and channel partnerships.

The market was up for grabs and the gold rush (or was it burn?) had begun.

Building a House of Cards

Against this backdrop, the replacement of “linear” TV by OTT was underway.

The concept of linear TV is explained in detail by Netflix in their Long Term View. But, if you’re too busy to read, linear TV is essentially set programming for set hours for everyone to consume.

Linear TV was fixed time, fixed shows and fixed screen. Non-linear TV, or OTT, was anytime, personalized show and any screen. The concept of binge-watching is alien to a linear TV world but is a symptom of a non-linear world.

Non-linear TV built on the personalization – the ‘hook factor’ to understand one’s tastes, consumption habits and offer the most compelling content. Again, the erstwhile DVD rental company Netflix brought this concept home.

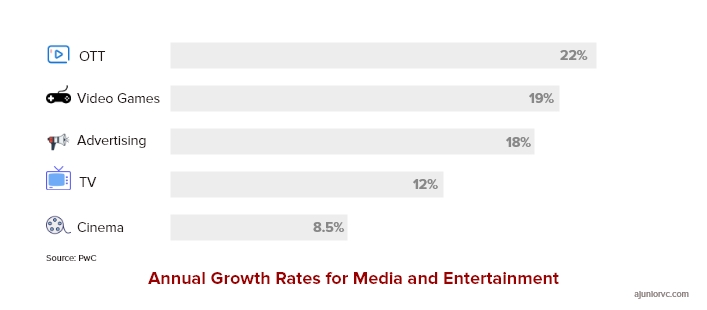

It is little wonder that OTT was driving the growth of the Media and Entertainment sector.

The Media & Entertainment industry was valued at INR 2.64 Lakh Cr in 2018 ($36.5B) with OTT industry recording the highest segment growth at 22% to reach INR 12k cr ($1.6B) by 2023.

The OTT market has transitioned from a nascent stage in India (2016-18) and currently moving to a phase of growth. India is expected to be among the Top 10 markets globally in video OTT by 2020. By 2023 India will have >500MM online video subscribers, second only to the biggest online video market in the world – China.

That is a massive 8-spot jump in 3 years.

Contrary to popular perception, the traditional forms of entertainment such as the television will continue to enjoy good growth rates in India.

TV might slow but will not be completely knocked down by the rise of OTT as seen in other markets. The TV industry will witness a CAGR of ~11% from 2017-22 while the global growth average will stagnate to 1.4% in the same period.

India has a massive number of TVs, with penetration in more than 170MM households, or 850MM+ people. Driven by a craze for entertainment, or doles of political largesse, TVs will remain a mainstay of the Indian viewing experience.

The OTT players would view this as a window, or a screen, into people’s souls.

Hotstar Starts OTT’s Battle for Iron Throne

In 2018, there were over 40 OTT players in the Indian market, from close to zero in 2010.

The war for eyeballs across the country was on, spurred by an explosion of internet users with quick and easy access to any content on the internet.

Companies like BIGFlix and nexGTV tried to make an impression on Indian audiences in the early ‘10s. But like many companies you’ve probably never heard about that, they were good ideas before their target market was ready for them.

The leader and first mover of the Indian OTT industry was Hotstar, launched by Star in 2014. Coincidentally this was right about when IPL 2015 was kicking off, which brought to Indian subscribers live cricket, shows and movies. By 2018, Hotstar had over 150MM active users and 350MM downloads

According to Hotstar’s India Watch Report 2018, 96% of watch time on Hotstar comes from videos longer than 20 minutes, while one-third of Hotstar subscribers watch television shows. In 2019, Hotstar began investing ₹120 crores in generating original content such as “Hotstar Specials”. 80% of the viewership on Hotstar comes from drama, movies and sports programs.

The sell to consumers was clear – Hotstar is a one-stop-shop to watch live sports, movies and everything else you can ‘consume’ on the internet.

Despite customer acquisition being driven by large sporting events, the goal for Hotstar is to keep users on the platform by the rich offering of content available to subscribers on a monthly basis.

But Hotstar specialized in “ephemeral” content, like live sports, where the value of timing i.e. watching live was immense. Other OTTs could focus on “eternal” content, which could be watched anytime unless someone spoiled it for you.

A huge whitespace of users existed that Hotstar did not target, and others saw an opportunity.

Everyone Is Playing Sacred Games

On the surface, one might think that the majority of these users would come from metro cities.

But the Watch Report shows that Kerala, UP and Bihar are the hotspots of user concentration. Further, cities with 1-10 lakh people showed the highest growth of sign-ups on the app. Finally, women were coming on to the platform 2-3x more than men were.

Hotstar was democratizing access to digital content around the country. But whenever an upstart begins to dominate an industry, the vultures start circling.

Hotstar’s incredible success, with additional proof of a viable industry solution given by SonyLiv and DittoTV, only further encouraged the two global giants, Netflix and Amazon, to double down on the Indian OTT space.

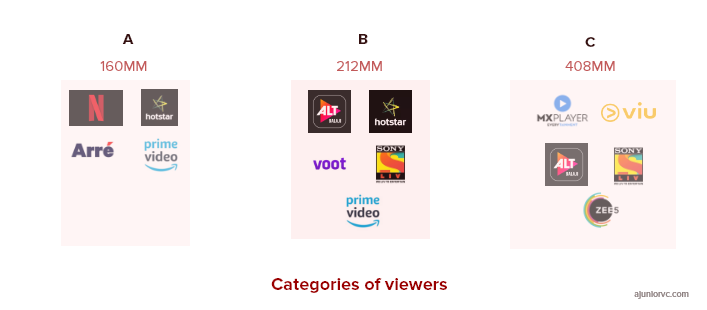

Spread across three categories, that loosely split across urban/rural and income groups, each OTT targeted categories of India’s 700MM+ TV watchers. Category A is the urban, tier 1 city viewer. Category B is the small town, tier 2 city viewer. Category C is the rural, tier 3 city viewer.

For a level set on the spending patterns of these players recall: Netflix spent Rs. 100 CR into the latest season of Sacred Games.

The average Indian competitors spends around 30-40Cr into their shows, at the higher end. Netflix’s strategy to come in as the premium content provider at a higher price might work in the West. But as we’ll see when exploring business models, it has had to make some tweaks to appeal to the masses in the Indian market.

In order to compete, Netflix recently began testing a lower-cost, mobile-only plan in India, at 250 INR ($3.6) a month, but still comes in more expensive than its rivals. Hotstar subscriptions start at a monthly rate of about 199 INR (about $2.87), while Amazon charges 129 INR ($1.86) for a Prime subscription that includes streaming video.

Amazon, never far behind from a growing trend anywhere in the world, previously committed to investing $5Bn in India. It has expanded its selection of movies and TV shows on Prime Video which comes with a typical Prime membership. Despite hotly debating unbundling video from the overall package, it continues to be a feature of Prime even today.

Amazon, Netflix and Hotstar were becoming the holy trinity of Indian OTT.

Looking in A Black Mirror

When it comes to monetizing, there are some key differences to Western markets that must be noticed.

Foresmost, the Indian consumer is very familiar with advertising and accepts it as a reality with most digital consumption, from radio to on-demand video.

Today, over 80% of revenue in the industry comes from advertising, expected to grow at a CAGR of 45% for the next five years. For the Netflix and Amazon Primes of the landscape, they would have to provide a far superior service in terms of personalization and integration to create large volumes of subscription revenue.

However, if a service is able to convert a one-time viewer into a subscriber, there is significant lifetime value that makes each of those users a very valuable and profitable customer.

Hotstar, widely recognized as the current leader in the space, has made significant strides in this aspect. Using algorithms to better understand their large user base and learn to more accurately predict the customer lifecycle and funnel, Hotstar has built a series of ‘nudges’ to drive people to subscriptions.

A less ‘sexy’ player in the space is the content-first Eros Now.

Eros has the largest OTT library in the Indian market and drives user acquisition through telecom partnerships with Jio, Vodafone and Airtel, among others.

A similar story to Disney’s latest Disney+ streaming service, Eros brought a wealth of previously owned content into a digital format and grew their subscriber base to 13MM paid subscribers by the end of 2018.

But the real dark horse of India’s OTT could be Netflix.

Looking at paid subscribers, only Hotstar, Prime and Netflix have those. According to estimates, Hotstar would have ~4M, Prime is 1.2MM and Netflix is ~1MM.

Prime Video is rightly a % of the overall Prime subscriber base. Hotstar and Prime cost $14, and Netflix costs $87 annually. Multiplying, back of the envelope estimates put Hotstar would be $60M, Amazon Prime would be $16M and Netflix would be $90M.

This is corroborated by Netflix’s marketing blitz and local content. This appears to have worked as revenue surged 8x to INR 470Cr ($80MM) and net profits 25x to Rs. 5.15Cr ($1MM) in FY19

Written off as the vanquished Ashwatthama, Netflix would be the fierce Rudra in India video. But there were bigger structural considerations that the three will have to consider.

The very foundations that these players built on are looking shaky.

Breaking Industries is Not Bad

Along with adding millions of subscribers, Jio’s entry also pushed its own industry in a tailspin.

A lot of ‘incumbents’ struggled and eventually gave declared bankruptcy and gave way for liquidation. One of those incumbents was RCom.

Some 30 months hence, the industry consolidated and a 3-player oligopoly emerged. Vodafone-Idea, Reliance Jio and Bharti Airtel, in decreasing order of subscribers. The dust seems to have been settled.

Well, not quite.

Contentions had been on about the settlement amount for something called Adjusted Gross Revenue (AGR) for years. The Supreme Court recently settled this AGR debate. Again, almost.

The now defunct (RCom) posted the biggest yet loss in the history of corporate India; Vodafone-Idea and Bharti Airtel followed suit and also posted really huge losses on top of bleeding balance sheets.

This has left 2 of the existing 3 players, particularly one of the players, between a rock and a hard place. Between marginally improving ARPUs and massive debt and regulatory obligations, our top player Vodafone is contending throwing in the towel.

The first domino fell. If regulatory pressure is not eased and in the unlikely and unfortunate event of a player calling it quits at this stage, telecoms will be forced to increase prices across the board.

Suddenly, people might start rationalising their consumption again.

Maybe they will keep consuming content but they will move to cheaper alternatives or resume watching TV? One subscription to engage them all?

If viewership and/or subscribers fall, the OTT industry will be in trouble. Its two biggest revenues are ads (through viewership) and subscription (through subscribers).

To understand the implication, we need to look at OTTs are part of an ecosystem of 4 key stakeholders. If the ecosystem breaks or slows down anywhere, it can whiplash.

Notice that in the ecosystem, telecom is 3 players, OTTs are 40+, content creators are in the 1000s and subscribers in the millions.

As you can imagine, power and influence are concentrated in those that are fewer in number. That is undoubtedly telecom.

If telecom hurts, it will hurt OTTs. In an era of data rationalization, the competitors to attention will not only be the numerous OTTs.

It will be Whatsapp, TikTok and Instagram.

Understanding Stranger Things in The Future

India’s OTT is heading for a complicated future.

On one side is growing demand, fuelled by increased internet penetration and rock bottom data prices. People are consuming more content than ever before, and all this happening on their phones.

On the other side is exploding supply, not least in OTT itself. With close to 40 OTT players, and assuming each has a library of 10K hours each, we are looking at 400K hours of content. But attention is getting divided even more, and it’s not limited to OTTs.

Whatsapp, TikTok and Instagram are all competing for the same currency – attention.

As Star India’s Sports Business Head Anirudh Kalia puts its succinctly “money is a commodity, attention is scarce”. If we go by the 20 minutes spent on OTTs daily in a market report, 200 million users have a total of 66MM hours of attention daily, or 24 Bn hours a year.

Dividing this volume of “attention hours” by the amount of content, we get an average of 60K viewers per unit of content. As we know that some hit shows have 10MM+ viewers, you can realize that a lot of content being produced is long tail.

This content is likely going to be seen by no-one, while it will cost money to produce. The big hit shows will take away attention from a lot of smaller players.

The looming threat of the data pipes being shut down is ever-growing. Strategically, OTT is a feature for a telecom player, and in the long run – a telecom player will start its own service. Without these data pipes, the OTT party is on weak foundations.

When the turbulent tides wash way, those without clothes will be caught naked.

The slicing of attention will cap demand, which will in-turn cap supply. Content production will become higher quality, but will flow through fewer OTTs. The market is already exhibiting winner takes most behaviour, like e-commerce.

Network effects are quite literally true here.

We expect OTT to evolve into a few dominant horizontals (e.g. Hotstar, Netflix) and multiple niche verticals (e.g. regional/theme focused OTTs). If the data pipes keep flowing, good content creators will flock to the larger OTTs. But in the end, who is winning in the OTT war?

The consumer, of course.

Written by: Aviral, Keshav, Rohan, Shiraz

Brilliant coverage and though full analysis!

Article helps me to understand how closely telecoms companies, OTT, content creator etc are connected with each other.

Thanks so much, Ankur! Please keep reading 🙂

Pretty good Bird’s Eye View..!

Thanks a lot Rohit! Please keep reading 🙂

A new angle and analysis!

Absolutely top notch analysis with a perfect blend of popular OTT show titles. Kudos!

Thanks so much for your comments Ravi! Please keep reading.

Loved the coverage of the topic! Worth every minute spent reading.

Thanks so much Eric!

Brilliant analysis man!

Thanks so much Rishabh!

[…] mirror local taste. Try ordering a McAloo Tikki anywhere else in the world!. Hotstar dominates the Indian OTT market through ad-supporting and live TV viewing and has beaten out competitors like Netflix, who tried to […]

As always, nice analysis. Just wanted to highlight a couple of things. There would be quite a few subscribers with all three major OTT subscription who are not dependent on mobile data for broadband internet (myself included). This might be low in volume right now but with mobile data getting costlier, I can see rise in demand for this dedicated non-mobile data providers with unlimited plans. Also, though I don’t have data to support the hypothesis, I would presume that the actual paying customers (at least for Netflix and Amazon Prime) would be quite price insensitive to the mobile data… Read more »

Brilliant piece of analysis. Just one question what is the unit of measure for content when you say 60k users per unit of content?

Hey Aviral, I have the same question. Could you please throw some light on this?

Hey nice article but two contention points -:

1. Are you sure that 80% of the revenue of these ott firms come from advertisements. I haven’t yet seen an ad on the platform of the content providers.

2. Another thing to note worthwhile would be prices will be competitive going forward so for survival they have to offer diverse content to increase subscribers.

Hey Pranshu, thanks for this. For the first point – the reference is linked. The reason why revenues are such a high percentage is Hotstar’s revenue from cricket ads + Hotstar is one of the largest rev % in OTT. Agree on 2.

This is quite comprehensive, without being dense it gives you all the details needed. Great job, Aviral.

Thanks Nikhil, credit to the entire team for working on putting this together.

How are you?

[…] viral. Shopkeepers and roadside vendors had already been using internet-enabled smartphones for OTT content consumption. All they needed was a simple-to-use app to use it for […]

Great Article,’

As per my opinion,<a href=”https://slidingmotion.com/why-ott-platform-better/”>OTT platform</a> will be the choice for Low Budget filmmaker because they are investing low money in OTT as compared to theatres.